Publications /

Policy Brief

The global energy system has entered a period of acute structural stress following the strikes by the United States and Israel on Iran in late February 2026, and the subsequent disruption of flows through the Strait of Hormuz. According to the International Energy Agency, the resulting shock marks the most severe disruption to global energy markets since the 1970s oil crises, with systemic characteristics comparable to the combined effects of those crises and the 2022 Russia-Ukraine energy shock.

This policy paper examines the mechanics of the oil-price shock, then assesses the structural importance of the Strait of Hormuz as a global energy chokepoint, through which an estimated 17.8 million barrels per day of crude oil and LNG transited before the Iran conflict. It highlights the limited substitutability of existing bypass infrastructure under conditions of sustained disruption. It also evaluates the fragmentation of the OPEC+ framework, including the United Arab Emirates’s announced withdrawal from the alliance on May 1, 2026, marking a critical point in the erosion of coordinated production management among major Gulf exporters. Finally, it analyses the role of renewable energy as a structural variable in the crisis, not as a short-term buffer, but as an accelerating force reshaping the geopolitical foundations of energy security.

The Hormuz disruption should therefore be understood not only as a price shock, but as a systemic stress test of global energy governance, exposing deep structural fragilities and accelerating realignments across markets, alliances, and the energy transition.

1. Introduction

The global energy system is being redefined less by gradual transition dynamics, than by abrupt geopolitical rupture. The escalation of military conflict between the United States, Israel, and Iran in late February 2026, culminating in the effective closure of the Strait of Hormuz, has triggered a significant shock affecting oil and liquified natural gas (LNG) supplies, plus related commodity markets. The International Energy Agency (IEA) has characterized the event as the most severe disruption to global energy flows since the 1970s, underscoring its systemic rather than cyclical nature.

At its core, the crisis has reactivated a long-recognized but often underappreciated vulnerability in the global energy architecture: extreme geographic concentration of hydrocarbon transit routes. The Strait of Hormuz, through which nearly one-fifth of global oil and LNG passes, is a critical bottleneck in the link between Middle Eastern supply and Asian and European demand centers. While alternative routes and strategic reserves exist, their capacity remains insufficient to fully offset sustained disruption at this scale. Consequently, the shock has propagated rapidly through both physical supply chains and financial pricing mechanisms, amplifying volatility across global energy markets.

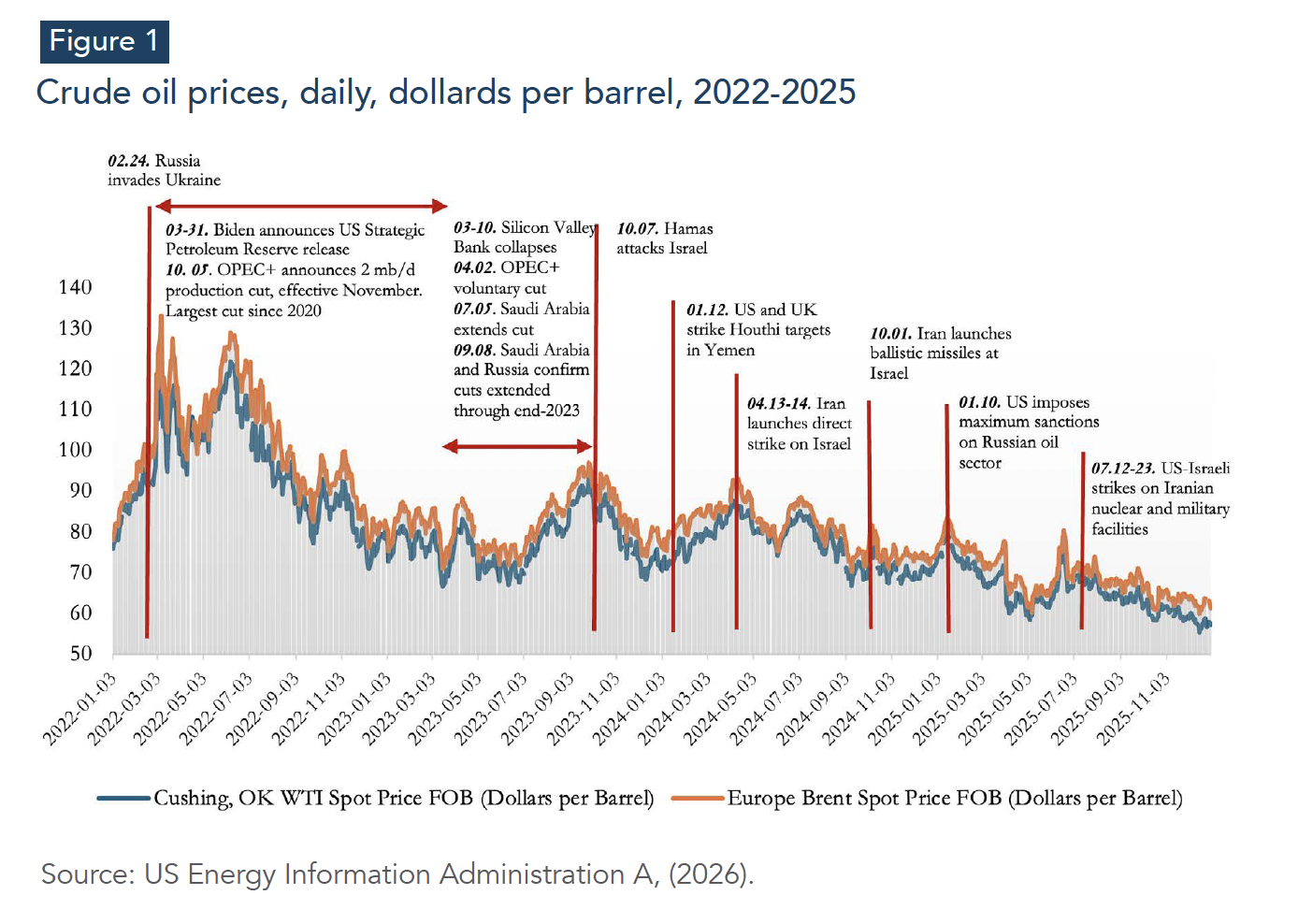

The immediate market response has been sharp. Brent crude prices surged from a pre-crisis environment characterized by structural surplus conditions to levels exceeding $119 per barrel within days of the U.S.-Israel attack on Iran. The price surge reflected both physical risk premiums and expectations of prolonged supply insecurity. However, the significance of the shock extends beyond short-term price dynamics. It has exposed deeper structural tensions in global energy governance, including the fragility of coordinated production regimes and the uneven distribution of energy security across importing and exporting states.

These tensions are at time of writing manifesting within the institutional architecture of OPEC+, which represents oil-producing nations. The announced withdrawal of the United Arab Emirates (UAE) from the alliance in May 2026 marked a critical inflection point in the erosion of collective supply management among major producers, raising fundamental questions about the future of cartel coordination in an increasingly fragmented geopolitical environment. Importing economies are responding through strategic stockpiling and demand-side adjustments, and also through accelerated investment in renewable energy and electrification as instruments of energy security.

This policy paper situates the Hormuz crisis within this broader structural context. It argues that the current disruption should be understood not as an isolated geopolitical shock, but as a stress test of the global energy order, which is simultaneously accelerating the reconfiguration of oil market governance, exposing the limits of chokepoint-dependent supply chains, and reinforcing the strategic importance of renewable energy systems in an era of heightened geopolitical uncertainty.

2. The Mechanics of the Oil Price Shock

The price shock that followed the U.S.-Israel strikes on Iran in late February 2026 did not emerge from a vacuum. To understand why it propagated so rapidly and at such scale, two prior conditions must be established: the structural state of the market at the moment of impact, and the specific financial and physical transmission mechanisms through which a geographic supply disruption becomes a global price event.

2.1. The Pre-Crisis Baseline: A Market Primed for Volatility

In the months preceding the escalation, the operation of global oil markets was deceptively calm. Brent crude settled into a range of approximately $62–$68 per barrel by December 2025, a price environment consistent with moderate structural surplus conditions. OPEC+ production restraint was holding, if imperfectly, while U.S. shale output reached record levels of approximately 13.4 million barrels per day (mb/d). Demand growth in China had decelerated markedly following a prolonged property-sector contraction, further suppressing the forward price signal.

Beneath this apparent equilibrium, however, several structural vulnerabilities accumulated. First, the OPEC+ coalition was sustaining price discipline at increasing political cost (see section 4): chronic non-compliance by Kazakhstan and Iraq eroded the credibility of quota enforcement even before the UAE’s departure. Second, global spare production capacity outside the Gulf was structurally limited: U.S. shale, though responsive to price signals, operates on a three- to six-month lag between investment decision and incremental output, not on the days-to-weeks timeline that an acute disruption requires. Third, the global insurance and tanker charter markets had no standing mechanism able to price and intermediate such a geographically concentrated disruption, a vulnerability that would prove decisive in the early phase of the shock (World Economic Forum, 2026).

The result was a market that appeared liquid and well-supplied, but lacked the institutional and logistical depth to absorb a sudden, large-volume disruption at its most critical transit node. The pre-crisis price level of $62–$68/bbl reflected this structural fragility only retrospectively: it contained essentially no risk premium for closure of the Strait of Hormuz, a pricing omission that the market corrected with exceptional speed once the shock materialized.

2.2. Two-Speed Transmission: Physical Supply and Financial Risk Premium

The price response to the Hormuz disruption was transmitted simultaneously through two distinct but mutually reinforcing channels. Conflating them obscures the mechanics of what occurred.

The physical channel was the more fundamental. The effective closure of the Strait removed from circulation an estimated 17.8 mb/d of crude oil and LNG, approximately one-fifth of globally traded supply. (Reuters A, 2026). No combination of strategic-reserve releases, bypass-pipeline activation, or spare-capacity deployment could substitute this volume on the timescale the market required (the structural constraints of bypass infrastructure are quantified in section 3). Refineries in Japan, South Korea, and India, operating on days-to-weeks of inventory buffer, faced genuine physical tightness. The spot premium for non-Gulf crude grades (North Sea Brent, US West Texas Intermediate (WTI), West African Bonny Light) widened immediately as buyers competed for physically available barrels outside the disrupted zone.

The financial channel amplified this physical signal through the expectations mechanism. Unlike prior Hormuz brinkmanship episodes, including the 2011–2012 Iranian nuclear standoff, and the 2019 Abqaiq strikes, the 2026 escalation had no clear near-term resolution pathway (EUISS, 2026). Forward curves, therefore, embedded not merely a spot disruption premium but a sustained supply insecurity premium across the six to 18-month horizon. Options markets skewed sharply upward as hedgers scrambled to purchase insurance against tail-risk price scenarios. The combination of physical tightness and open-ended duration expectations drove Brent from its pre-crisis range to above $119/bbl within days, a dislocation with few modern precedents in its speed, if not its absolute level.

2.3. The Insurance and Charter Market Seizure

A mechanism less commonly analyzed in oil-price shock discussions, but central to the 2026 episode, is the near-simultaneous seizing up of the tanker insurance and charter market. Within days of the escalation, Lloyd’s of London and the major P&I (protection and indemnity) clubs suspended or sharply restricted war-risk coverage for vessels transiting or operating within a broadly defined Persian Gulf exclusion zone (Osler, 2026). Without war-risk insurance, tankers cannot operate commercially: cargo buyers cannot obtain letters of credit, ports may refuse to berth uninsured vessels, and shipowners bear unlimited liability exposure.

This insurance mechanism created a secondary chokepoint that has been, in some respects, more immediately disabling than the physical disruption itself. Even Saudi crude that could theoretically exit via the Petroline bypass to Yanbu on the Red Sea has faced commercial impediments: the Red Sea has been subject to Houthi interdiction since 2024, and extended war-risk exclusion zones encompass portions of that routing as well. The practical effect has been to strand volumes that were physically accessible but commercially immovable, a distinction that purely volumetric assessments of the disruption systematically understate.

The charter rate spike that followed was extreme: VLCC (Very Large Crude Carrier) day rates for routes avoiding the Gulf of Oman reached levels last seen briefly in early 2020, at the onset of the COVID-19 pandemic storage trade (Washington et al, 2026). For longer Cape of Good Hope routings, the only fully Gulf-free alternative for crude destined for Asian buyers, the combination of elevated day rates, longer voyage times, and war-risk surcharges has added a logistical tariff that has priced some end-users out of the spot market entirely and forced refinery run-cuts as a demand response.

2.4. Grade Incompatibility and the Refinery Lock-In Problem

A structural feature of the Hormuz shock that distinguishes it from most historical supply disruptions is the degree to which available non-Gulf crude is commercially accessible but technically incompatible with the refinery configurations of the most-exposed importing economies.

The major refining centers of northeast Asia—China, Japan, South Korea, and Taiwan—were designed and built over decades with the explicit assumption of continued access to Persian Gulf crude. These are typically medium-to-heavy, high-sulfur grades, and their processing characteristics are embedded in the capital configuration of catalytic cracking units, desulphurization equipment, and hydrocracker specifications (Bakshi and Vij, 2026). The main non-Gulf alternatives available in volume during the disruption, namely US WTI, West African Bonny Light, and Norwegian grades, are mostly light sweet crudes. They, therefore, do not match these refinery configurations without blending adjustments or process-unit modifications, neither of which can be implemented within weeks.

The result is a bifurcated market, in which a global crude surplus by volume coexists with a shortage by grade and region. Some volumes of non-Gulf crude are commercially available, but cannot be refined efficiently at the sites of greatest demand. In Asia, some refineries, therefore, have been running below capacity, not for lack of crude by volume, but for lack of the right crude by specification. This grade lock-in problem reinforces the geographic concentration risk discussed in section 3, and underlines why the substitutability of Gulf supply cannot be assessed purely in volumetric terms.

3. The Strait of Hormuz: Anatomy of a Critical Chokepoint

Sections 4 and 5 of this paper examine the institutional and strategic responses to the Hormuz disruption, the fracturing of OPEC+, and the acceleration of the energy transition. Both analyses rest on a precise understanding of what the Strait of Hormuz actually is, what flows through it, what alternatives exist in practice, and why the 2026 closure constitutes a categorically different event from prior episodes of Hormuz brinkmanship. This section provides that foundation.

3.1. Physical Geography and Strategic Geometry

The Strait of Hormuz is a 21-nautical-mile-wide waterway at its narrowest point, connecting the Persian Gulf to the Gulf of Oman and from there to the Indian Ocean. Traffic management regulations channel commercial shipping through two designated lanes, inbound and outbound, each two nautical miles wide, separated by a two-mile buffer zone. The navigable corridor available to deep-draft tankers is, therefore, substantially narrower than the Strait’s overall width, creating a concentration of vessel movement that has no parallel in any other major energy transit route (Butler et al, 2026).

The Strait is flanked by Iran to the north and by Oman and the UAE to the south. The northern coastline, controlled by Iran, is within easy range of shore-based anti-ship missiles, mines, and fast-attack craft. This geographic asymmetry defines the strategic logic of the chokepoint: the cost to Iran of denying or degrading commercial transit through the Strait is structurally lower than the cost to naval and commercial actors of sustaining unimpeded passage under active threat conditions. Even if U.S. and allied naval forces retain the military capacity to transit the Strait, sustaining the conditions under which commercial insurers will cover tanker voyages—a separate and more demanding threshold—requires a security assurance that cannot be provided unilaterally.

This asymmetry is not new, but it had been systematically underpriced by energy markets and policy frameworks that conditioned expectations on decades of managed brinkmanship (Umud, 2026). The 2026 escalation has broken that conditioning in a way that the 2019 Abqaiq strikes, the 2011-2012 sanctions standoff, and the 1980s Tanker War did not: it removed the implicit assumption that the Strait would remain commercially navigable, regardless of the political temperature in the Persian Gulf.

3.2. Flow Composition: Crude, LNG, and the Compounding Effect

The 17.8 mb/d that transited the Strait of Hormuz prior to the crisis encompassed two distinct commodity streams whose simultaneous disruption has produced a compounding shock with serious implications.

The crude oil component flows predominantly to Asian markets. China, India, Japan, South Korea, and Taiwan collectively absorb most Hormuz-transiting crude (the geographic and technical dependency of Asian refining on Gulf crude is discussed in section 2.4). The economic cost of the disruption has thus fallen disproportionately on Asia, which unlike Europe has not developed diversified pipeline infrastructure or strategic reserve holdings sufficient to buffer a multi-month interruption.

The LNG component adds a qualitatively distinct dimension. Qatar, the world’s largest single LNG exporter prior to the conflict, supplying approximately 25%–30% of globally traded LNG, operates all of its liquefaction infrastructure from the North Field on the Qatari peninsula, with export terminals located entirely within the Persian Gulf (Calabrese, 2017). There is no pipeline export alternative for Qatari LNG: the commodity cannot leave Qatar without transiting the Strait.

The additional damage to Qatari liquefaction infrastructure, with two of fourteen trains destroyed with an estimated five-year reconstruction horizon, ensures that even a normalization of Hormuz transit conditions will not restore Qatari LNG exports to pre-crisis levels in the near term (El Dahan et al, 2026). This permanent reduction in global LNG supply capacity is a structural feature of the post-2026 energy landscape that section 5 returns to in the context of transition pathway risk.

3.3. Bypass Infrastructure: The Arithmetic of Inadequacy

In practice, only two pipeline systems offer meaningful alternatives to Strait transit for Gulf crude exporters.

Saudi Arabia’s East-West Pipeline (Petroline) connects Eastern Province oil fields to the Red Sea terminal at Yanbu, with a capacity of approximately 4.8 mb/d and an estimated sustained operational throughput of 3.5–4.0 mb/d. The UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP) connects Habshan to the Port of Fujairah on the Gulf of Oman, with a capacity of approximately 1.5 mb/d. Combined, these systems provide a theoretical maximum bypass capacity of roughly 5.3–5.5 mb/d, covering at most 31% of the normal Hormuz flow (Argus, 2026).

The practical ceiling is lower. Petroline’s Red Sea outlet was already subject to commercial constraints from residual Houthi maritime activity in the Red Sea, which have not fully ceased since the Iran escalation. War-risk insurance extensions into the Red Sea further limit the commercial attractiveness of this routing for cargo buyers. The ADCOP outlet at Fujairah is located in the Gulf of Oman, which while outside the Strait itself remains within the extended naval threat perimeter of the conflict zone. Neither route offers unconditional commercial access.

For LNG, the bypass calculus is simpler: it does not exist. Qatar’s liquefaction terminals are located on the Persian Gulf coast with no pipeline infrastructure connecting to any external market. The LNG disruption is, therefore, total under Hormuz closure conditions. This asymmetry, partial crude bypass and zero LNG bypass, is a structural design characteristic of Gulf energy export infrastructure, which was established over decades of investment and premised on Hormuz remaining open.

4. The OPEC+ Fracture: UAE Exit and the End of Cartel Coherence

Compared to previous crises, the Hormuz crisis differs in three main ways: dynamic escalation, absence of diplomatic resolution, and permanent infrastructure damage. The IEA characterizes the current crisis as one of the most severe disruptions to global energy markets since the 1970s. They also define the context within which OPEC+ fragmentation (section 4) and renewable energy reframing (section 5) must be understood: both are responses to a shock with a duration and structural consequences that are categorically different from anything the post-1973 energy governance system was designed to manage.

4.1. Strategic Rationale and Timing of the UAE’s Withdrawal

The UAE's formal withdrawal from OPEC on April 28, 2026, was not a sudden strategic pivot. Rather, it reflects the culmination of a long-standing structural grievance. As OPEC’s third-largest producer, behind Saudi Arabia and Iraq, the UAE had expanded its upstream capacity to approximately 4.85 mb/d through a sustained $150 billion investment program, while remaining subject to a production quota of roughly 3.2–3.5 mb/d (Patterson et al, 2026; Reuters B, 2026). The resulting idle capacity of 1.4–1.6 mb/d represents an estimated annual opportunity cost of $50 billion–$70 billion at prevailing prices, a sacrifice that became fiscally and politically untenable for a government facing elevated defense expenditures, capital outflows, and intensifying competition with Riyadh over regional economic primacy (Jing, 2026).

Exiting the cartel frees the Abu Dhabi National Oil Company (ADNOC) to pursue a produce-to-capacity strategy, operating as a normal non-OPEC independent, analogous to U.S. or Brazilian producers, with no obligation to subordinate output decisions to collective quota discipline. This pivot is underpinned by a deliberate long-term calculus: anticipating peak oil demand and the progressive devaluation of hydrocarbon reserves under the global energy transition, Abu Dhabi has chosen to monetize its resources aggressively while the demand window remains open, rather than to hold production in reserve to support cartel-managed price floors (Jing, 2026).

The timing of the announcement was strategically chosen to limit market and diplomatic fallout. With the Strait of Hormuz effectively closed to regular commercial traffic, UAE export volumes are already constrained by geography rather than by quota. The immediate price impact of the exit is, therefore, muted, as any material increase in supply cannot reach markets until shipping lanes normalize (Patterson et al, 2026). As the UAE Energy Minister stated publicly, the exit “at this time is the right time, because it will have minimum impact on the price and minimum impact on our friends at OPEC”.

Beneath the economic rationale lies a deterioration of the political compact that once bound the Gulf producers together. Relations between Abu Dhabi and Riyadh were strained well before the current conflict, most acutely over Yemen, where Saudi forces struck UAE-backed Southern Transitional Council positions, and over diverging postures on Somalia and the Horn of Africa (Hart, 2026). The Iran war has introduced a further rupture: while both capitals initially expressed solidarity under Iranian attack, the two governments have since diverged on war aims and the terms of any diplomatic settlement, eroding the trust that underpinned their coordination.

The decision to announce the withdrawal on April 28, the same day Crown Prince Mohammed bin Salman hosted a Gulf Cooperation Council unity summit, was not coincidental. It was a pointed signal that Abu Dhabi’s patience with Saudi-dominated institutional frameworks had run its course (ThinkChina, May 2026). For the UAE, continued formal membership of a cartel that includes Iran had become untenable.

4.2. Institutional Fragility and the Erosion of OPEC Cohesion

The UAE’s withdrawal does not merely reduce OPEC’s headcount. It removes one of the two load-bearing pillars of the cartel’s market-management architecture, with consequences that are likely to compound over time. The UAE’s significance to OPEC was never primarily a function of its production volumes, but of its spare capacity. Alongside Saudi Arabia, it was one of only two members able to mobilize idle output at scale within 30 days, the mechanism through which OPEC absorbs supply shocks and defends price floors. That buffer is now gone, leaving Saudi Arabia to conduct increasingly costly price-stabilization operations with a structurally thinner cushion (CNBC, 2026). S&P Global’s near-term price assessment remains neutral, reflecting the reality that UAE export volumes are still constrained by the Hormuz closure, regardless of quota status, but the medium-term structural damage to the cartel’s shock-absorption capacity is not in dispute.

The more consequential effect of the exit may prove to be normative rather than volumetric: it has demonstrably lowered the political cost of departure for remaining members. Kazakhstan is the most closely watched candidate. Astana has been a chronic non-complier, producing approximately 26% above its assigned quota of 1.468 mb/d as recently as early 2025, driven by the international-operator-led ramp-up of the Tengiz field, over which the government exercises limited production-side leverage (Pokidaev, 2025). Responding to the UAE announcement, Kazakhstan’s energy ministry confirmed it had no current plans to alter its participation format, but conspicuously declined to reaffirm quota discipline, a distinction that analysts were quick to note (Discovery Alert, April 2026). Iraq, similarly flagged as a potential departure risk given estimated overproduction of 250,000–300,000 b/d, moved promptly to deny any exit intention (Reuters C, April 2026). Neither departure is imminent. But the UAE’s decision has established that exit in pursuit of national production interests is both executable and survivable, a precedent that will complicate Riyadh’s ability to hold the coalition together through the next bout of pricing pressure.

That challenge points to a deeper problem for Saudi Arabia. Riyadh retains unquestioned primacy within what remains of OPEC; its spare capacity of approximately 2–3 mb/d dwarfs that of any other member. The difficulty is not Saudi market power in isolation, but its ability to enforce collective discipline across a membership characterized by endemic non-compliance. Iraq and Nigeria have both routinely exceeded their quotas without meaningful sanction. The UAE’s presence provided an institutional counterweight that lent Saudi quota enforcement a degree of legitimacy beyond naked self-interest. Without it, as former U.S. State Department Special Envoy David Goldwyn observed, Riyadh “will have a weaker hand” (CNBC, April 2026). The fiscal dimension sharpens the dilemma: the Kingdom requires approximately $90 per barrel to balance its budget, per International Monetary Fund estimates, yet its capacity to anchor prices through coordinated supply management has just been materially reduced.

These dynamics arrive on top of a decade-long structural retreat. OPEC’s share of global output had already declined to approximately 30%, less than half its historic peak, while the broader OPEC+ framework controlled around 40%–45% of global supply prior to the UAE’s exit (Reuters C, 2026). The shale revolution permanently reordered the supply-side equation: U.S. production now accounts for roughly 20% of global output, providing a structural ceiling on OPEC’s long-run pricing power. The UAE’s exit is seen as the biggest schism in the organization since it was founded in 1960, a judgement that reflects not the immediate market arithmetic but the signal it sends to an alliance whose cohesion has long rested more on political inertia than genuine convergence of interests (Flower et al, 2026).

4.3. Long-Term Price Dynamics: What a Post-OPEC World Looks Like

The immediate market consequences of the UAE’s withdrawal are paradoxically limited. In the short term, the exit is broadly price-neutral to mildly bearish, because the Strait of Hormuz remains partially disrupted by the Iran war, physically constraining the UAE’s ability to monetize any additional production capacity. The real structural implications will emerge only once maritime traffic normalizes.

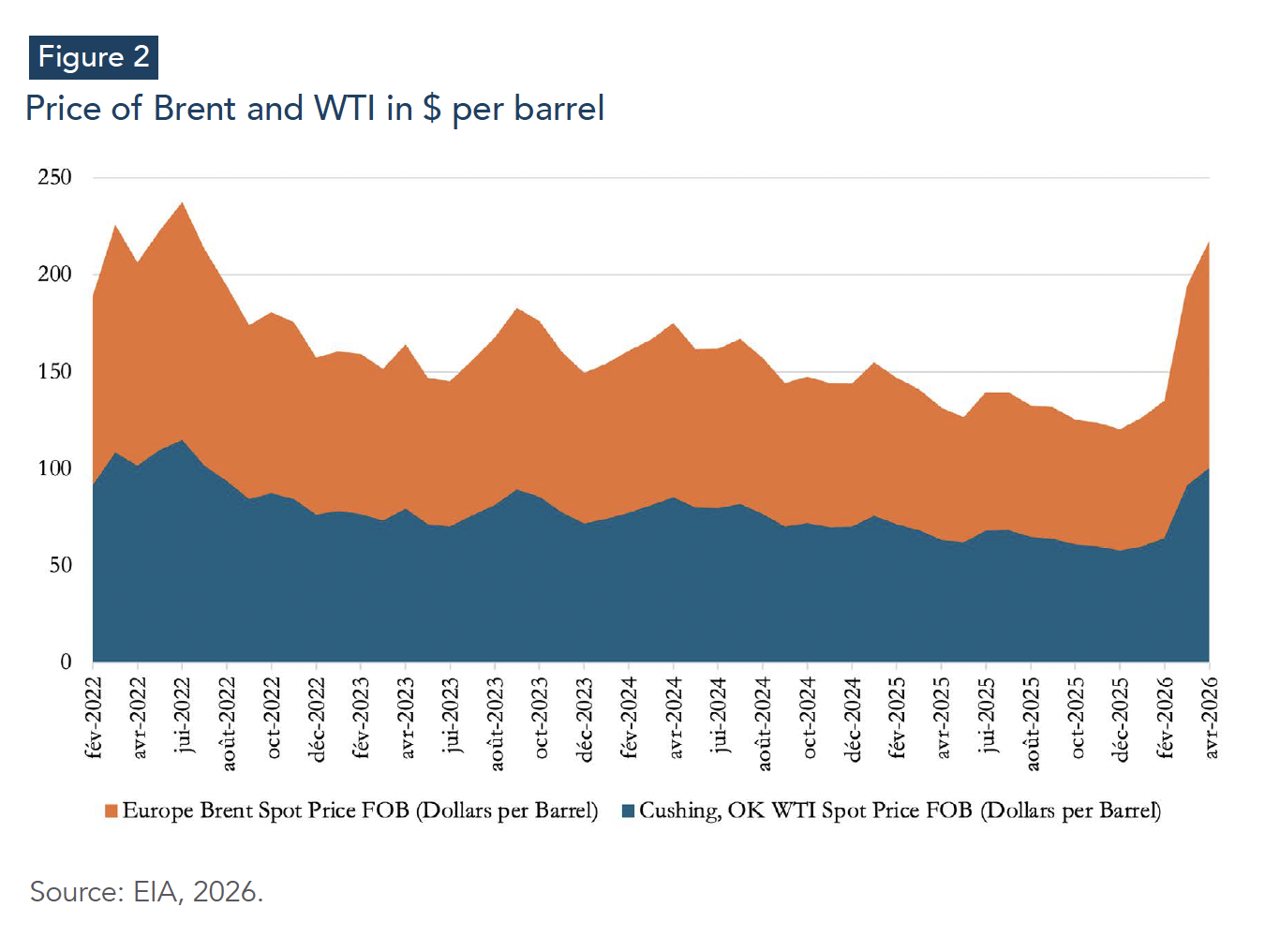

Over the medium term, however, the UAE’s departure introduces a significant new bearish force into global oil markets. Freed from OPEC production ceilings, Abu Dhabi can progressively deploy an estimated 1–1.5 mb/d of idle capacity accumulated through its long-term upstream expansion program. Combined with the continued responsiveness of U.S. shale producers to elevated prices, this creates a structurally more elastic supply environment than that which characterized the pre-shale OPEC era. Historical price trajectories since the Ukraine shock already point in this direction. After peaking above $120/bbl in mid-2022, Brent prices entered a prolonged downward adjustment, despite repeated geopolitical disruptions and sustained OPEC+ intervention efforts. Between June 2022 and December 2025, Brent prices declined from approximately $123/bbl to nearly $63/bbl, while WTI fell from roughly $115/bbl to below $58/bbl. Even during periods of heightened geopolitical stress, prices repeatedly reverted toward the $70–$80 range, suggesting the emergence of a softer structural ceiling on sustained price increases.

This dynamic reflects a deeper transformation in the political economy of oil markets. The post-2016 OPEC+ framework functioned not simply as a production alliance, but as an implicit volatility-suppression mechanism. Through coordinated quota discipline, led overwhelmingly by Saudi Arabia, the cartel provided markets with an informal price floor, dampening both oversupply collapses and speculative instability. The UAE’s exit weakens that mechanism materially. Without credible collective discipline, the burden of stabilization increasingly falls on Riyadh alone, raising the financial and political cost of future interventions. The result is likely to be a market characterized not necessarily by permanently low prices, but by structurally higher volatility.

Recent price movements already illustrate this shift. Between December 2025 and April 2026, Brent prices surged from roughly $62/bbl to over $117/bbl, while the Brent-WTI spread widened sharply as maritime risk premiums intensified around seaborne crude exposed to Hormuz-related disruptions. Such swings are consistent with a market losing part of its coordinating architecture: geopolitical shocks continue to trigger acute price spikes, but the capacity to sustain elevated prices over long periods is progressively eroding.

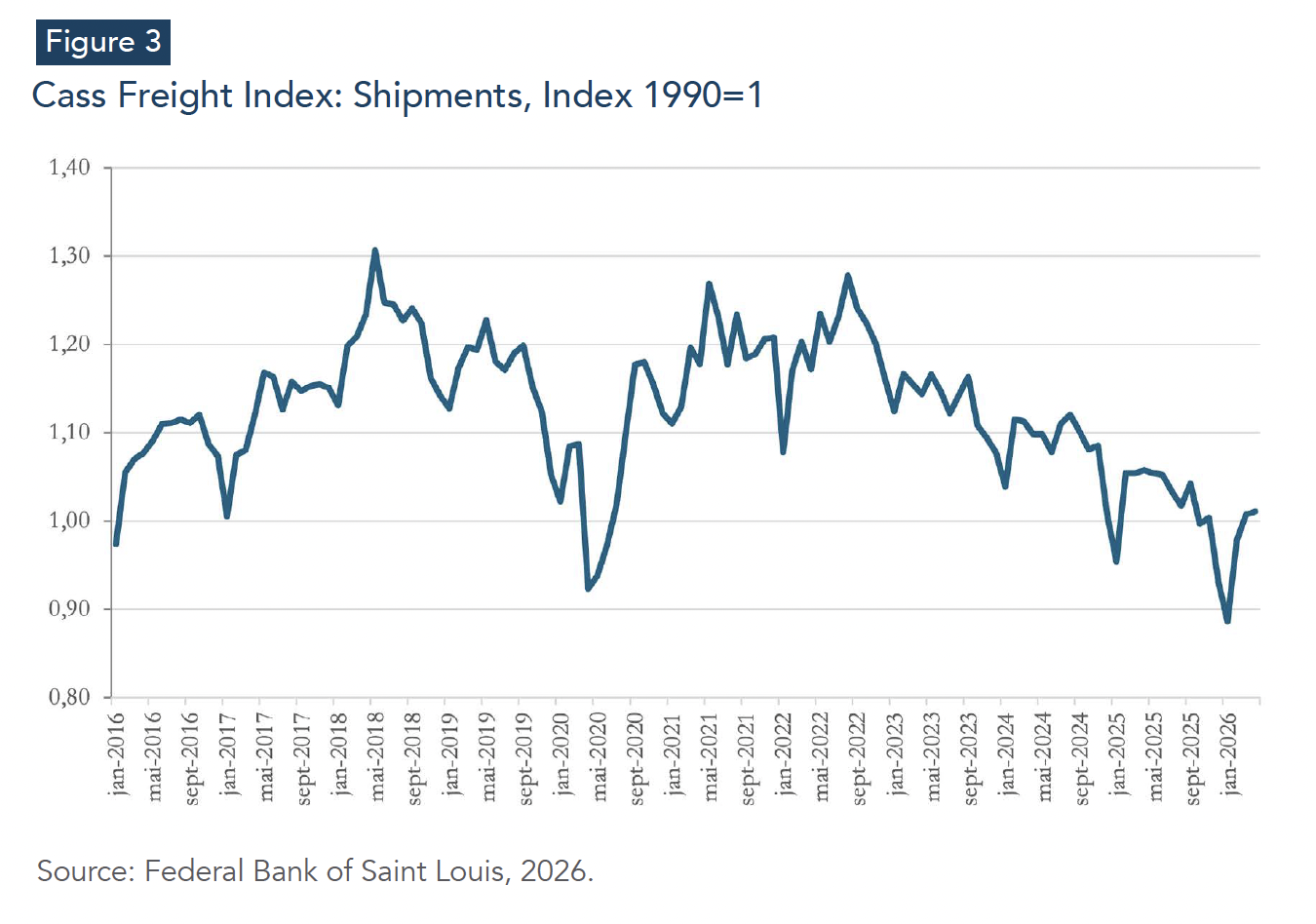

Figure 3 provides a complementary demand-side dimension to this structural diagnosis. Having recovered sharply from its pandemic low of 0.92 in mid-2020, and briefly surpassing 1.27 in early 2022, the Cass Freight index entered a sustained contractionary trend, falling below the 1.00 threshold by late 2025 and reaching approximately 0.89, its lowest reading since the COVID-19 shock. This deterioration in physical freight volumes is analytically significant: it indicates that demand-side weakness is compounding the supply-side pressures introduced by the UAE’s exit from OPEC production discipline. In a market simultaneously confronting structurally more elastic supply and decelerating demand, the stabilization mechanisms historically associated with coordinated quota management lose much of their operative leverage, reinforcing the broader contention that the post-2016 price floor is being eroded from both sides of the market equation.

For energy-importing economies, this creates a dual and somewhat contradictory reality. Lower expected long-term oil prices may reduce the immediate economic urgency of fossil-fuel substitution, particularly in developing countries facing industrialization pressures and fiscal constraints. Yet greater price instability simultaneously strengthens the strategic rationale for domestic renewable-energy deployment as a tool of energy sovereignty and macroeconomic resilience. In this sense, the fragmentation of OPEC may accelerate the energy transition, not through scarcity, but through insecurity.

5. The Hormuz Shock and the Strategic Reframing of Renewables

5.1. The Security Reframing: From Climate Imperative to Energy Sovereignty

The most consequential effect of the Hormuz crisis on the energy transition may not be economic but cognitive. The crisis has fundamentally reframed the political argument for renewables, shifting it from the language of environmental obligation to the language of national interest. This is not a messaging adjustment but a structural change in the political economy of the transition, one that broadens its coalition and accelerates its timeline in ways that years of climate advocacy could not.

The evidence is already visible in consumer behavior and policy responses. Across Europe, online searches for electric vehicles, heat pumps, and home solar systems surged to record highs in the weeks following the Hormuz closure (Ferreira, 2026). France unveiled its most sweeping electrification plan to date, doubling annual electrification funding to €10 billion, banning gas boilers in new buildings, and targeting two in three new cars to be electric by 2030. The Philippines, with 98% of its oil imported from the Middle East and only around 40 days of supply remaining at the height of the crisis, fast-tracked 22 major renewable energy projects targeting over 1.4 GW of new capacity within weeks of declaring a national energy emergency (Ferreira, 2026; Hart, 2026). Other examples from Asia highlight this shift of narrative: South Korea’s president called for the country to move “very quickly toward renewable energy”. Japan announced expanded offshore wind permits and Turkey pledged $80 billion in renewable investment by 2035 (Myllyvirta, CREA, April 2026).

The crisis has made viscerally clear what energy security analysts long argued in the abstract: dependence on fossil fuels transiting a single 29-nautical-mile chokepoint is not a manageable risk premium but a structural vulnerability (IEA, 2026). For net energy importers, the geopolitical mandate to accelerate domestic renewable capacity has now eclipsed the environmental one. The longer the disruption persists, the stronger the structural incentive for accelerated renewable deployment and electrification, particularly across transport and power generation systems. Sustained exposure to oil and gas price volatility reinforces the economic and strategic rationale for electric vehicles, renewable electricity generation, and reduced dependence on imported hydrocarbons, thereby accelerating the long-term shift toward domestically anchored energy systems. (Gross and Tomer, 2026).

Crucially, this reframing travels further than environmental framing precisely because it maps directly onto national interest, crosses ideological lines, and speaking to constituencies that have never engaged with climate policy, but who understand, viscerally, what it means to be exposed (Ferreira, 2026). The policy implication is clear: the security rationale should now be the primary institutional frame for renewable deployment, in policy chambers, investment mandates, and procurement strategies alike.

5.2. The Empirical Case: Renewables as a Demonstrable Shock Absorber

Beyond political framing, the crisis has generated real-time empirical evidence of the economic advantage conferred by prior clean-energy investment and the cost of its absence. The contrast is stark and quantifiable.

In Europe, the same crisis produced radically different outcomes depending on the energy mix in place before the shock. Italy, still heavily dependent on gas-fired generation, saw electricity prices peak at €142/MWh in the immediate aftermath of the Hormuz closure. Finland, with a renewables-heavy grid, held at approximately €35/MWh. Spain and Portugal, where solar, wind and hydro collectively generate 57% of electricity, remained closer to €60/MWh (Andreolli and Signorelli, 2026). The divergence is not incidental, it reflects the fundamental price-setting logic of electricity markets, in which the marginal generator, in this case gas-fired plants, determines the market clearing price for all generation. Countries that structurally reduced the frequency of gas as the marginal producer insulated their entire electricity system from the shock (Hanson and Isaacs, 2026).

The aggregate figures reinforce this. Without the wind and solar capacity added across the EU between 2022 and 2025, the bloc would have spent an additional €58 billion on fossil-fuel imports since the start of the Hormuz crisis. Solar generation alone saves the continent over €100 million per day (Ferreira, 2026). Italy’s reduction in gas demand of 16% between 2021 and 2025, achieved through electrification, efficiency improvements, and renewable deployment, translated into €4.3 billion retained within the domestic economy rather than transferred abroad (Andreolli and Signorelli, 2026). These are not projected savings from a future transition; they are realized, measurable outcomes of prior investment decisions.

Power generation data further undermines the prevailing ‘coal comeback’ narrative. In the first month following the Hormuz closure, global fossil-fuel power generation fell 1% year-on-year across countries with near-real-time data. Gas-fired generation dropped 4%. Coal-fired generation was broadly flat, not because of new capacity, but because coal plants in most markets were already running at near-maximum utilization before the crisis, meaning no headroom for substitution (Myllyvirta, 2026). Outside China, solar output grew 14% and wind 8% year-on-year in March 2026, absorbing demand that gas could no longer reliably meet. Seaborne coal transport volumes fell 3%, to their lowest levels since 2021, the opposite of what a genuine coal resurgence would produce (Myllyvirta, 2026).

Pakistan offers a particularly instructive case at the household and SME levels. A distributed solar boom, driven initially by unaffordable grid electricity and the availability of low-cost Chinese panels, had, by the time the crisis began, already avoided $12 billion in oil and gas imports. During the crisis, rooftop and plug-in solar installations buffered the power sector from the worst effects of gas supply disruption, particularly during daylight hours. This was not the result of a government mandate but of a market-driven substitution engineered not by energy policy but by the price signal (Hanson and Isaacs, 2026). The lesson for policymakers is that the most resilient energy transitions are those that embed distributed generation capacity ahead of the shock, not in response to it.

The record solar and wind capacity added globally in 2025 alone, approximately 510 GW solar and 160 GW wind, generates an estimated 1,100 TWh per year, or roughly twice the electricity that would have been produced from all the LNG that transited the Strait of Hormuz before the closure (Myllyvirta, 2026). The energy-security calculus embedded in that comparison is powerful and should inform infrastructure investment prioritization accordingly.

5.3. The Structural Counterargument: New Chokepoints, New Dependencies

The security rationale for renewables is compelling, but contains a structural vulnerability that policy analysis must not elide. The Hormuz shock has accelerated the global energy transition, but acceleration without supply-chain diversification risks substituting one form of strategic exposure for another. The clean energy transition does not eliminate chokepoints but relocates them, from maritime straits and hydrocarbon reserves, to mineral processing facilities and manufacturing supply chains (Project Syndicate, April 2026).

The concentration risk is significant. China currently holds an average 70% market share in the refining of 19 critical minerals tracked by the IEA, including lithium, cobalt, and rare earth elements, which are foundational inputs for solar panels, wind turbines, lithium-ion batteries, and electric vehicles (Hart, 2026). It manufactures the dominant global share of solar PV modules, battery cells, and EV drivetrains—what President Xi Jinping has called the “new trio”. China is also increasingly supplying the grid infrastructure, transformers, power electronics, and grid management software that a high-renewables electricity system requires. Chinese state-owned firms are already building and operating entire regional grid systems across parts of South America and southern Europe (Hart, CFR, April 2026). The clean-energy system that the world is now urgently building is, in large measure, a Chinese-manufactured system.

This creates a second-order geopolitical exposure that policymakers in Brussels, Washington, Tokyo, and Seoul cannot ignore. The Philippines provides an illustration: with 98% of its oil imported from the Middle East, it has every incentive to accelerate its renewable build-out, and it is doing so. But in moving rapidly toward solar and battery storage, it is deepening its dependence on China—with which it has an unresolved territorial dispute—for the equipment and supply chains that underpin its new energy security architecture (Tewari et al, 2026). The risk exchange is real: reduced exposure to Persian Gulf hydrocarbon disruption, increased exposure to potential Chinese supply-chain leverage.

The aluminum case illustrates the depth of interdependency. Aluminum is a critical input for the ‘new trio’ and for power transmission lines, drone systems, and a wide range of industrial applications. Gulf states, particularly Bahrain and the UAE, have been significant producers, but their aluminum exports have been shut down alongside their hydrocarbon exports by the Hormuz crisis. China, which accounts for approximately 60% of global aluminum production, is the residual supplier (Somwanshi, 2026). The crisis has, in effect, reinforced Chinese leverage across multiple critical material supply chains simultaneously.

Furthermore, the disruption to Qatari LNG, with two of fourteen liquefaction trains destroyed and an estimated five-year reconstruction timeline, has curtailed what was one of the more viable medium-term pathways for reducing coal dependence in Asia: a managed transition through gas (Gross and Tomer, 2026). The loss of 20% of the global LNG supply does not automatically accelerate the shift to renewables in every market; in some, particularly price-sensitive emerging economies facing near-term demand destruction, it creates conditions for reversion to coal or biomass, as seen in parts of Africa where households have returned to solid fuels for cooking. The transition is not a uniform curve.

The policy implication is not that the energy transition should be slowed. The security, economic and climate cases for it remain compelling and are now reinforced by real-time evidence. It is, rather, to pursue the transition with analytical clarity on where the new dependencies lie. Critical minerals must be treated as a strategic asset class, not a procurement afterthought. Investment in domestic and allied-nation processing and refining capacity must be pursued with the same urgency now applied to renewable deployment itself. Supply-chain due diligence must become a standard component of energy-security doctrine. And the transition strategy must explicitly account for the differential impact across economies at different stages of development, where the risk of crisis-driven regression is real and the margin for managed substitution is narrow.

The Hormuz crisis has not changed the destination of the global energy transition. It has, however, exposed the strategic complexity of the journey, and the cost of navigating it without a clear-eyed map of the dependencies being built along the way.

6. Conclusion

The global energy system is often misread as a system undergoing a linear transition from fossil fuels to renewables, when in reality it is being reorganized under the combined pressures of geopolitics, infrastructure fragility, and institutional fragmentation. The Hormuz crisis demonstrates that energy security is no longer determined primarily by resource availability, but by the resilience of highly-concentrated transit networks, the credibility of producer coordination mechanisms, and the capacity of markets to insure against systemic geopolitical risk. In this context, what appears as a price shock is in fact the manifestation of a deeper structural stress test of global energy governance.

We identify three reinforcing distortions that define the post-crisis energy order. First, the collapse of reliable chokepoint stability transforms maritime geography into a binding constraint on global supply, introducing discontinuities that cannot be offset by marginal increases in production or strategic reserves. Second, the fragmentation of OPEC+ undermines the last institutional mechanism able to smooth volatility on the supply side, replacing coordinated adjustment with asymmetric and increasingly unilateral production strategies. Third, the energy transition itself is accelerating not because of coordinated climate policy, but by crisis-driven security incentives that reallocate investment toward electrification while simultaneously embedding new dependencies in critical minerals, processing capacity, and industrial supply chains.

The concept of fragmented resilience captures this emerging configuration: states are no longer optimizing for efficiency or even energy independence in a traditional sense, but for differentiated exposure management across overlapping layers of risk. In this environment, the critical constraint is not technological feasibility, but the spatial and institutional organization of energy systems across production, transformation, and trade.

The central policy challenge is therefore no longer confined to accelerating the energy transition or stabilizing fossil-fuel markets in isolation. It is to design governance frameworks that can manage a multi-layered energy system in which security, industrial policy, and decarbonization objectives are simultaneously interacting and often conflicting. The future of global energy stability will depend less on the speed of technological substitution, and more on the capacity to rebuild coordination mechanisms that can operate in a structurally fragmented and geopolitically exposed energy geography.

References

Andreolli, Francesca, and Giulia Signorelli. "Crisis in the Strait of Hormuz: Gas, Energy Prices and European Strategic Autonomy." ECCO — Italian Climate Network, March 12, 2026. https://www.eccoclimate.org.

Araral, Dianne, and Eduardo Araral. "The Energy Transition Has Its Own Strait of Hormuz." Project Syndicate, April 3, 2026. https://www.project-syndicate.org/onpoint/clean-energy-transition-is-creating-new-strategic-vulnerabilities-by-dianne-araral-and-eduardo-araral-2026-04.

Bakshi, Parul, and Samriddhi Vij. “Why Asia Cannot Replace Gulf Crude Easily.” Observer Research Foundation (ORF) Middle East, May 1, 2026. Observer Research Foundation

Butler, Gavin, Toby Mann, and Patrick Jackson, with BBC Persian. “Why the Strait of Hormuz Matters So Much in the Iran War.” BBC News, April 8, 2026. BBC News

Calabrese, John. “Global LNG Markets in a State of Flux: Qatar in the Crosshairs?” Middle East Institute, December 12, 2017. Middle East Institute

CNBC. “Iran War Energy Facilities, Refinery, Pipeline, LNG.” CNBC, April 15, 2026. https://www.cnbc.com/2026/04/15/iran-war-energy-facilities-refinery-pipeline-lng.htm

European Union Institute for Security Studies. “War in the Middle East: What Implications for the EU and the World?” EUISS Commentary, March 2026. https://www.iss.europa.eu/publications/commentary/war-middle-east-what-implications-eu-and-world.

Federal Reserve Bank of St. Louis. “Cass Freight Index: Shipments (FRGSHPUSM649NCIS).” FRED Economic Data. Accessed May 18, 2026. https://fred.stlouisfed.org/series/FRGSHPUSM649NCIS

Ferreira, Filipe. "Hormuz Has Made the Case for Renewables." The Brussels Times, May 14, 2026. https://www.brusselstimes.com.

Flowers, Simon, Alan Gelder, Douglas Thyne, Hazel Seftor, Alexandre Araman, and Dalia Salem. “UAE’s Exit Rattles OPEC’s Grip on the Oil Market.” Wood Mackenzie, April 29, 2026. https://www.woodmac.com/blogs/the-edge/uaes-exit-rattles-opecs-grip-on-the-oil-market/

Funaiole, Matthew P., Harrison Prétat, Aidan Powers-Riggs, and Jasper Verschuur. "The Strait of Hormuz in 8 Charts." Center for Strategic and International Studies, April 22, 2026. https://www.csis.org.

Gross, Samantha, and Adie Tomer. "The Iran War Is Making Energy More Expensive for Everyone." The Brookings Current (podcast and transcript). Brookings Institution, May 13, 2026. https://www.brookings.edu/articles/the-iran-war-is-making-energy-more-expensive-for-everyone/.

Halabi, Bachar. “Saudi East-West Pipeline Maxed Out on Hormuz Closure.” Argus Media, March 29, 2026. Argus Media

Hanson, Craig, and Jessica Isaacs. "As Iran War Strains Fuel Supplies, Clean Energy Is Secure Energy." World Resources Institute, April 10, 2026. https://www.wri.org.

Hart, David M. "With Hormuz Closed, China Is Wiring the Globe's Clean Energy Future." Council on Foreign Relations, April 16, 2026. https://www.cfr.org.

International Energy Agency. "Strait of Hormuz Factsheet." Last updated February 2026. https://www.iea.org/topics/oil-security/strait-of-hormuz.

Lin, Jing. “China May Be the Biggest Winner from UAE’s OPEC Exit.” ThinkChina, May 13, 2026. https://www.thinkchina.sg/politics/china-may-be-biggest-winner-uaes-opec-exit

Myllyvirta, Lauri. "Global Fossil Power Generation Fell after the Hormuz Closure due to Solar and Wind Growth." Centre for Research on Energy and Clean Air, April 14, 2026. https://energyandcleanair.org.

Osler, David. “How a Prolonged Gulf Conflict Could Squeeze P&I Clubs.” Lloyd’s List, March 12, 2026. https://www.lloydslist.com/LL1156600/How-a-prolonged-Gulf-conflict-could-squeeze-PI-clubs

Patterson, Warren, and Ewa Manthey. “The Commodities Feed: UAE Exit from OPEC Marks a Big Shift in Oil Market.” ING THINK, April 29, 2026. https://think.ing.com/articles/the-commodities-feed-uae-exit-from-opec-marks-a-big-shift-in-the-oil-market290426/

Pokidaev, Dmitry. “Kazakhstan Sees No Major Risks From UAE Exit From OPEC+.” The Times of Central Asia, May 11, 2026. https://timesca.com/kazakhstan-sees-no-major-risks-from-uae-exit-from-opec/

Reuters A, 2026, “Exclusive: Iran attacks wipe out 17% of Qatar’s LNG capacity for up to five years, QatarEnergy CEO says.” El Dahan, Maha, Andrew Mills, and Yousef Saba, March 19, 2026 (updated March 20, 2026). Reuters A

Reuters B, 2026, “Iran Crisis: Oil & LNG Flows Through the Strait of Hormuz.” Reuters, 2026. https://www.reuters.com/graphics/IRAN-CRISIS/OIL-LNG/mopaokxlypa/

Reuters C, 2026, “How the Strait of Hormuz closure affects global oil supply”, https://www.reuters.com/graphics/IRAN-CRISIS/OIL-LNG/mopaokxlypa/

Shokri, Umud. “Global Markets and the Strait of Hormuz: The Economic Shockwaves of the Iran War.” Stimson Center, March 3, 2026. Stimson Center

Somwanshi, Rohan. 2026. “FACTBOX: Attacks in the Middle East Hit Gulf Aluminum, Steel Plants Amid War.” S&P Global Commodity Insights, March 30, 2026. https://www.spglobal.com.

Tewari, Suranjana, Joel Guinto, and Jessica Rawnsley. 2026. “Philippines Declares Energy Emergency over Iran Conflict.” BBC News. https://www.bbc.com/news/articles/c3ex8ez3717o

U.S. Energy Information Administration A, 2026, “Spot Prices for Crude Oil and Petroleum Products.” Petroleum & Other Liquids Data Browser. Accessed May 15, 2026. https://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm.

U.S. Energy Information Administration (EIA) B, 2026, “Today in Energy.” U.S. Energy Information Administration, May 2026. https://www.eia.gov/todayinenergy/detail.php?id=67064

Washington, Thomas, Alec Kubekov, and Catherine Rogers. “VLCC Rates Face Downward Pressure as Tankers Flee Gulf Crisis.” S&P Global Commodity Insights, March 17, 2026. S&P Global Commodity Insights

World Economic Forum, 2026, “How War in the Middle East Is Turning Governments into Insurers of Last Resort.” World Economic Forum, April 2026. https://www.weforum.org/stories/2026/04/how-middle-east-war-turning-governments-into-insurers-last-resort/.