Publications /

Policy Brief

On Friday, March 10 -2023, the US and the world discovered that the Federal Deposit Insurance Corporation (FDIC) had seized the Silicon Valley Bank after SVB’s customers had withdrawn an extraordinary $42 billion from their deposits on March 16. This $4.2 billion an hour, or more than $1 million per second for ten straight hours, an unprecedented event made possible by the use of Apps by many startup founders to access their accounts and advise their friends to do the same -what the Chairman of the House of Financial Services Committee called ‘the first Twitter -fueled bank run’.

-

To put that in perspective, the previous largest bank run in modern U.S. history took place at Washington Mutual bank in 2008 and totaled $16.7 billion over the course of 10 days. That’s small compared to what was seen at SVB within one day. A small fraction of SVB’s deposits were insured by the Federal Deposit Insurance Corporation as its customers were overwhelmingly corporations with much more than $250,000 in the bank ($250,000 being the upper bound of the deposits insured on a single account by the FDIC).

-

The S&P lost 4.6% over the week ending on March 10, after the suggestion by the Fed on Tuesday that a rapid rise of interest rates was necessary to rein in a resurgent inflation; the losses accelerated as of Thursday when the bank sudden move to raise cash scared depositors and shareholders. On Friday, the FDIC seized SVB.

SOME MARKET INFORMATION

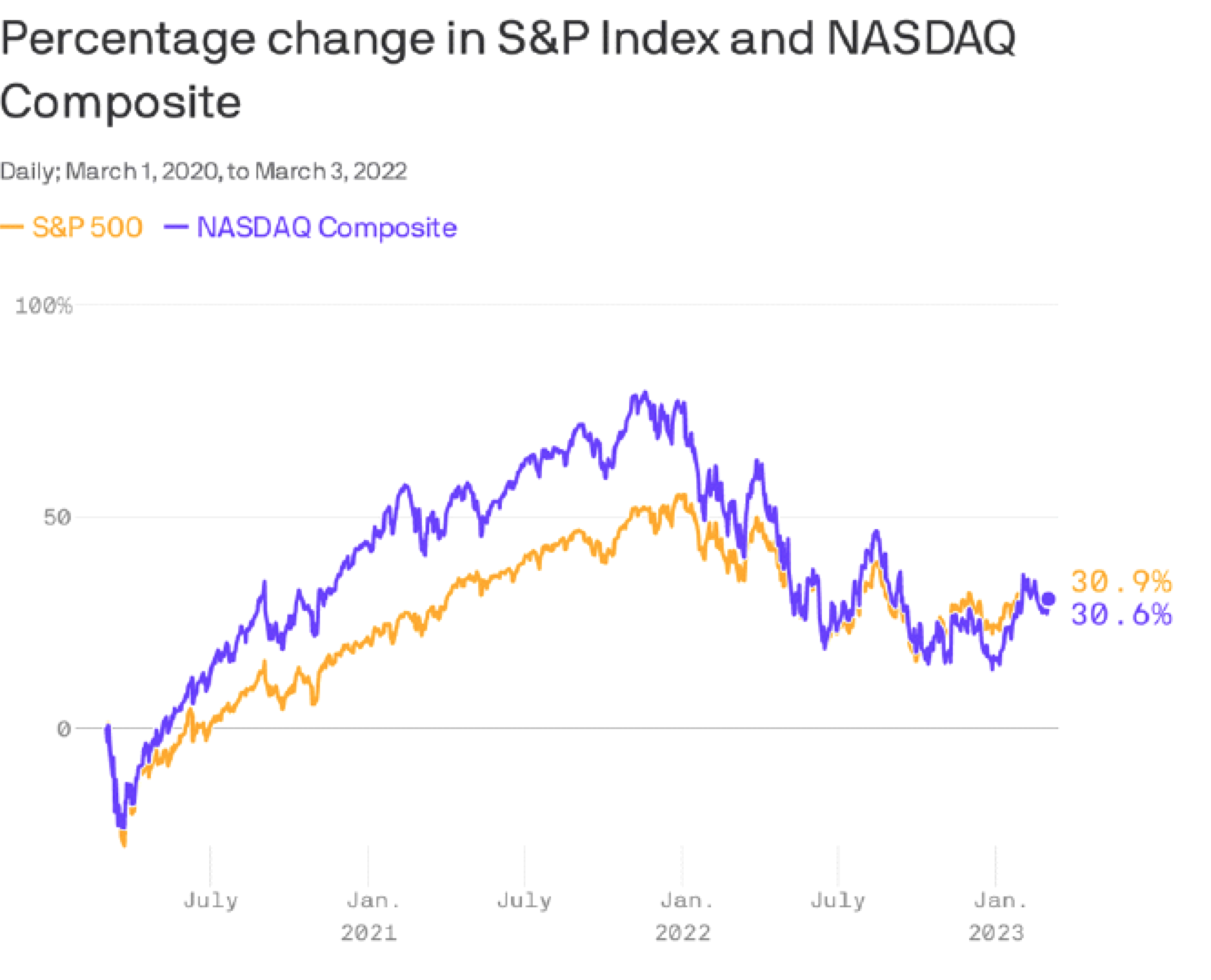

The behavior of the Nasdaq and S&P indexes in the period preceding the event is described in Figure 1

We can observe the following features on Figure 1

-

Remarkably, the compound returns on both indexes over the 3-year period were identical, at the (high) level of more than 30%.

-

However, the Nasdaq had achieved by October 2021 (over the first 17 months) a return of 70% - the period during which Tech stocks were invincible- and then experienced a sharp decline of 40% in the following 18 months.

-

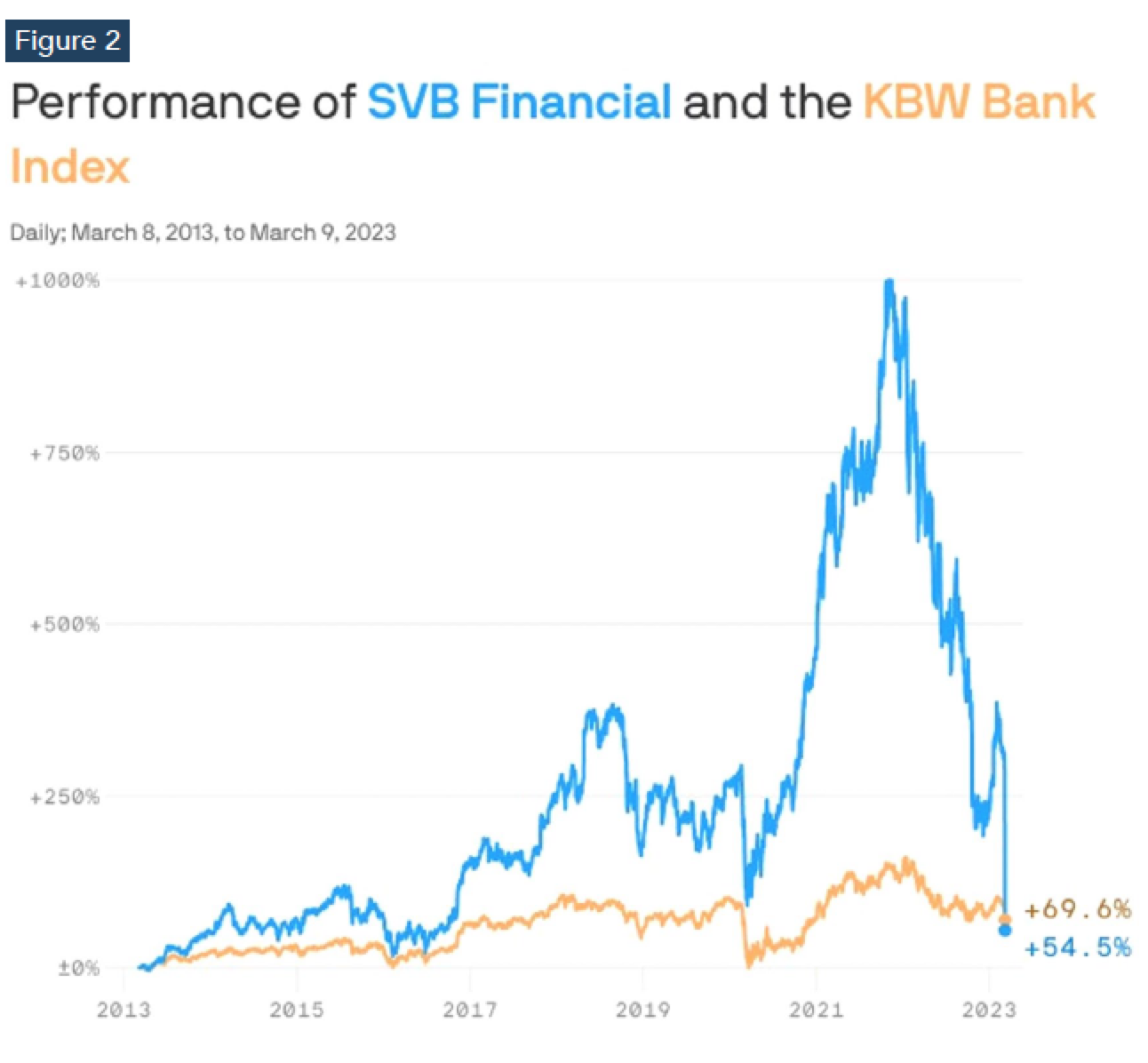

The Silicon Valley Bank, located in the heart of the Bay area, had startup founders as its primary customers, and Figure 2 shows that its share prices followed in an amplified manner the tumultuous ride of the Tech sector in the last two years. Note that SVB is one of the 24 banks included in the KBW Bank Index depicted below.

Looking at the SVB share price behavior during the first two months of 2023, one understands why the CFO sold 11 days before the collapse more than $3.5 million worth of bank stocks and the CEO sold for $3.6 million. In both cases, the executives had filed paperwork 30 days in advance of the sales, following the rule established in 2000 by the Securities and Exchange Commission (SEC) called Rule 10b5-1 meant to prevent insider trading -The SEC and Justice Department are investigating the sales of these stocks. On the other hand, some shareholders have filed a class action lawsuit against the two executives and SVB, alleging that the management of the bank had intentionally did not disclose that rising interest rates would leave the bank ‘particularly susceptible to a run’.

THE HISTORY OF THE COLLAPSE

- SVB, the bank of Californian startups with subsidiaries all over the world, collapsed in the evening of Thursday, March 9. It had been facing a liquidity crisis, created in particular by the suggestions of Mr Powell on Tuesday March 7 that a further rise of interest rates would be necessary to stop the persisting inflation.

-

SVB reacted by selling $21 billion of bonds, reportedly at a loss of $1.8 billion - still a very small fraction of the $209 billion the bank held in assets. SVB also tried to raise $2.5 billion in equity from the venture-capital community that represented a large part of its customer base. The result was a run on the bank.

-

It is worth observing that the statistical independence of the decisions of thousands of depositors to deposit or withdraw money does not hold in the real world where the state of the economy tends to affect all customers in the same way. The FDIC which was created to prevent bank runs by guaranteeing their deposits up to $250,000 cannot easily prevent a bank run in a highly connected world, in particular when the depositors know each other and text their friends to advise them to withdraw their money from a bank about to collapse.

-

Note that after a long period of interest rates Fed officials had tried to announce their interest rate moves deliberately over the whole previous year to avoid the turmoil created in 1994, when the Fed doubled its short - term benchmark rate from 3 to 6% in a 12-month time period. This contributed to the demise of the financial institution Kidder Peabody (itself greatly related to the wrongdoings of the star bond trader and a few executives), to the bankruptcy of the wealthy Orange County in California (led by an incompetent Treasurer, Mr Citron), as well as the Mexican peso devaluation – this one required a bailout from the US and the International Monetary Fund.

WHAT DOES ECONOMIC THEORY SAY?

In a remarkable timing, the most recent recipients of the Nobel Prize in Economics (2022), Ben Bernanke, Douglas Diamond and Phil Dybvig, were three US academics who had devoted part of their excellent research to matters related to banks. Ben Bernanke went on to become the 14th Chairman of the Fed from 2006 to 2014. The other two authors continued to spend their academic lives in prestigious US universities after having produced in 1983 the famous Diamond and Dybvig model on ‘bank runs’.

- The model shows how banks’ mix of illiquid assets (such as business or mortgage loans) and liquid liabilities (deposits which may be withdrawn at any time) may ‘naturally’ give rise to panics among depositors.

- The banks in the model act as intermediaries between savers who prefer to deposit in liquid accounts and borrowers who prefer to take long-maturity loans. Under ordinary circumstances, banks provide a valuable service by channeling funds from many individual deposits into loans for borrowers: by aggregating funds from many different depositors, banks help depositors save the high transaction costs they would have to pay in order to lend directly to businesses.

- But the model shows that banks are very vulnerable to panics, or bank runs: If a depositor expects all other depositors to withdraw their funds, then it is irrelevant whether the banks’ long term loans are likely to be profitable; the rational response for her/him is to rush to take her deposits out before the other depositors remove theirs.

- In fact, the Nash equilibrium reached in the model has two equilibrium states, one where the bank run is a type of self-fulfilling prophecy: each depositor’s incentive to withdraw funds depends on what they expect other depositors to do. If enough depositors expect other depositors to withdraw their funds, then they all have an incentive to rush to be the first in line to withdraw their funds.

-

The authors conclude, among other results, in favor of a Deposit Insurance backed by the Government - Indeed, the Federal Deposit Insurance Corporation had been created in 1933 in response to the thousands of bank failures that had taken place in the 1920s and early 1930s. However, the current situation is that there are at the present time $19 trillion of deposits in US banks - 8 trillion being insured by the FDIC - both numbers being very large. This explains why the President of the US and the Fed stepped in very rapidly after the run on SVB to avoid contagion in the system, invoking a ‘systemic risk exception’ to declare all deposits insured ($152 billion worth of deposits out of 175 billion were not insured; part of them were meant to ensure the payroll of startup employees)

WHAT DOES FINANCIAL THEORY SAY?

The practice of Asset Liability Management (ALM) in banks emerged in the 1970s as a necessary practice in an environment of high and rapidly changing interest rates with some Savings & Loans going to bankruptcy.

Leaving aside the (valid) subject of the credit profiles of bank borrowers, a key issue in ALM is the temporal adequacy of the Assets to the Liabilities, in particular to those Liabilities which are deposits that have to be repaid on demand.

It seems sure that the classical ALM indicators were not in place at SVB, possibly because of the absence for most of 2022 of a Chief Risk Officer who was replaced by an inexperienced risk management committee (and some possible insider trading by the CEO and CFO did not make the internal situation sounder).

In order to get interesting returns on its assets, SVB had a large portfolio of medium to long term bonds, creating a ‘duration gap’ between assets and liabilities of six years at least according to estimates. The Canadian economist Frederick Macaulay who had been working at the National Bureau of Economic Research from 1926 to 1938 brilliantly introduced in 1938 the simple but key concept of ‘bond duration’, in the simple setting of a flat yield curve with parallel moves. This indicator was extended in the mid- 1980s and 1990s when more complicated models for the yield curve dynamics were proposed, as well as a number of ‘risk markers’ that provide a safe monitoring of the impact of market moves - both in terms of interest rate risk and liquidity risk - on the balance sheet of a bank.

We also learnt at that time that, in order to correct an excess of duration gap, several solutions were available, among which :

-

Buy interest rate derivatives with a high sensitivity to interest rate changes, such as caps or swaptions, in order to reduce the duration of the total assets (since the liabilities side of a commercial bank has by nature a shorter duration). These derivatives may be costly to purchase from big financial institutions, however.

-

Create a situation of ‘self immunization’ of the balance sheet, by selling more floating rate mortgages to customers and buying for the bank portfolio (good rating) corporate bonds which are classically floating rate notes - both types of instruments being less sensitive to interest rate moves.

WHAT LIES AHEAD?

The American press frequently suggested in the two weeks following the demise of Silicon Valley Bank a comparison with Credit Suisse but the two situations were in fact quite different and there was nothing of a ‘bank run’ in the case of Credit Suisse. The formerly prestigious Swiss bank with its large activity of wealth management had performed in the last few years a remarkable number of large missteps, from internal rivalries to a $5.5 billion loss suffered from its gigantic investment in the hedge fund Archegos Capital Management, to the ‘tuna bonds’ scandal in Mozambique. Hence, the acquisition of Credit Suisse by its sister bank UBS was only a matter of months or days.

The case of SVB leaves open the problem of ‘moral hazard’ created when the President and the Treasury announced that deposits of more than $250,000 would be protected. The portfolio of assets of SVB was greatly composed of Government bonds and not of complicated structured securities; the rating of SVB by the major agencies was A, a very good grade suggesting a focus only on the credit worthiness of the lines of the balance sheet, but not on the Asset Liability structure. The deposits at SVB had doubled in 2021; and the lack of risk management inside the bank in 2022 was sadly complemented by the absence of supervision by US regulators after the application of the 2010 Dodd Frank Act had been limited in 2018 (by decision of the then President and Congress) reduced to banks with a balance sheet of more than $250 billion (instead of $50billion in 2010); the balance sheet of SVB at the time of the collapse was $212 billion.

Besides reinstating the Dodd Frank Act in its original form and rules defined after the financial crisis of 2008, US regulators need to ensure that they will provide in the future a proper attention to the numerous regional banks which constitute the tissue of the US banking system. Between 2015 and 2023, the share of real estate loans granted to customers by smaller banks (outside the 25 largest US banks) in the US went from 57% to 69% and loans to small and midsize businesses based on the information local lenders have built up over the years. So, if the deposits moved to a bigger bank in the county, a loan request by the small business would require a possibly long review of its credit worthiness before the loan was granted. According to the Wall Street Journal of March 20, 2023 a survey conducted by the FDIC in 2016 and 2017 had found that nearly 80% of banks with less than $10 billion in assets characterized most of their loans as going to small-business borrowers.

CONCLUSION

Going forward, both small and large banks will have, in the near future, to add to their stress tests the one created by a wave of large withdrawals generated by customers placing their orders on their Iphones without any conversation with a bank representative.

Regarding the Fed and other central banks, they face a difficult choice at this moment: keep rates high to control an inflation which continues to be arguably elevated or loosen monetary policy to ‘reassure’ the financial markets. The US, European and Japanese banks have lost around $460 billion in market value in two weeks in March. The visible cause is the rapid increase of reference interest rates in the US and other major economies. The deeper cause is the unwinding of a crisis created by more than a decade of artificially low interest rates (sometimes negative) – a situation for which there is no equivalent in the history of humankind, hence no place to turn to in order to infer the possible effects - manufactured by ‘Apprentis sorciers’ central bankers in many developed countries.

REFERENCES

-

B. Bernanke and AS, Blinder, 1992, ‘The Federal Funds Rate and the Transmission of Monetary Policy’ , American Economic Review

-

D. Diamond and D. Dybvig, 1983, “Bank Runs, Deposit Insurance, and Liquidity’,

Journal of Political Economy

-

J. Lahart and T. Demos, 2023 ‘Local Banks Could Leave Gaps that Are Hard to Fill’, Wall

Street Journal March 20

-

H.Geman and R.Portait, 1990 ‘A Framework for the Interest Rate Risk Analysis of a Portfolio and Bank Asset Liability Management’, American Stock Exchange Colloquium Proceedings

-

F. Macaulay,1938, ‘The Movements of Interest Rates. Bond Yields and Stock Prices in the United States since 1856, National Bureau of Economic Research, New York

-

N.N. Taleb, 2012 ‘ Antifragility: Things that Gain from Disorder’, Incerto collection