Publications /

Policy Brief

The call for private finance mobilization received an answer in 2024, with private capital accounting for 66% of total flows in climate finance, while still reaching a record level. This flow of private finance represents a structural shift that can both be considered as a significant achievement and an underexamined governance risk. This paper argues that the growth of private climate finance, while real and consequential, does not always directly serve climate objectives. Private capital is fundamentally risk-averse, return-driven, and structurally indifferent to the adaptation needs, geographic equity, and democratic accountability that a credible climate transition requires. As public governance architecture contracts, most sharply following the United States' 2025 withdrawal from the Paris Agreement, private actors have assumed increasing authority over four core governance functions: allocating capital, pricing risk, setting standards, and shaping narratives. That authority is exercised without democratic mandate, transparent methodology, or enforceable accountability.

The paper evaluates the three dominant mechanisms through which private climate governance currently operates: voluntary frameworks such as ICMA's Green Bond Principles, TCFD, and SBTi; regulatory extraterritoriality through instruments such as the EU's Corporate Sustainability Reporting Directive and California's SB-219; and MDB-intermediated blended finance. Each model addresses a real need for governance. None is sufficient. Taken together, they leave three critical gaps unaddressed: no reliable mechanism to direct capital toward adaptation and the most vulnerable geographies; no democratic accountability to the communities most affected by transition decisions; and no coordinating architecture to make the three models coherent and mutually reinforcing. The paper concludes that closing these gaps requires treating climate governance not as a technical question of instrument design, but as a political question of who holds authority over where capital flows and on whose terms.

Introduction

The story of climate finance in the 2020s is, on the surface, one of remarkable progress. Capital flows have broken records. Private investment has surpassed $1 trillion annually for the first time. Green bonds, sustainability-linked loans, and transition finance instruments have moved from niche to mainstream within a decade. By almost any aggregate metric, the mobilisation of private capital for the climate transition has exceeded what was considered plausible at the time of the Paris Agreement.

However, there is more than just numbers in financing climate change, the underlying issue is tracking the governance scheme of the capital flows, and the interests it serves, beyond the one of the climate objectives. In fact, record volumes of private climate finance are not the same as a governed transition. What this distinction demands, therefore, is analytical precision. Aggregate metrics obscure the governance structures through which capital flows, the instruments through which it is deployed, and the interests it ultimately serves. The type of climate finance in operation carries material justice implications: debt-based instruments such as bonds and insurance products risk entrenching already financially and ecologically vulnerable actors in deeper deficit, while the benefits of financialized climate governance are frequently captured by neoliberal institutions and market-based actors rather than those most exposed to climate risk (Ananthararajah and Setyowati, 2022)

1. When the private sector shapes the climate finance landscape

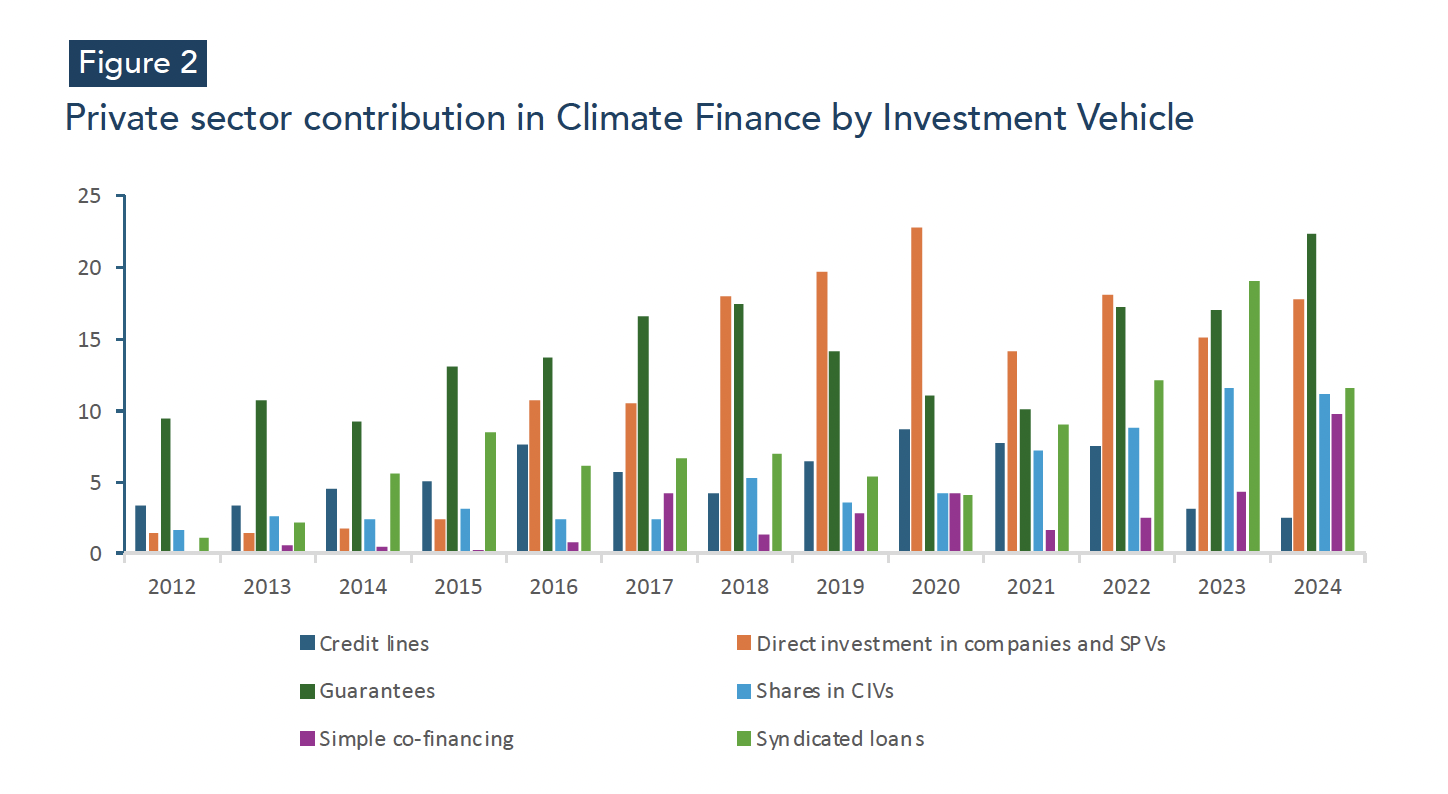

Global climate finance reached a record $2 trillion in 2024, more than doubling the levels observed six years earlier. Despite this rapid growth, funding remains well below the scale required to maintain a trajectory consistent with a 1.5°C warming limit, highlighting a persistent and critical financing gap. Private climate finance surpassed$1 trillion for the first time, underpinned by household investment in electric vehicles, rooftop solar, and energy-efficient housing. Over the 2012–2024 period, private sector contributions to climate finance have grown considerably, though the composition of investment vehicles has shifted in notable ways.

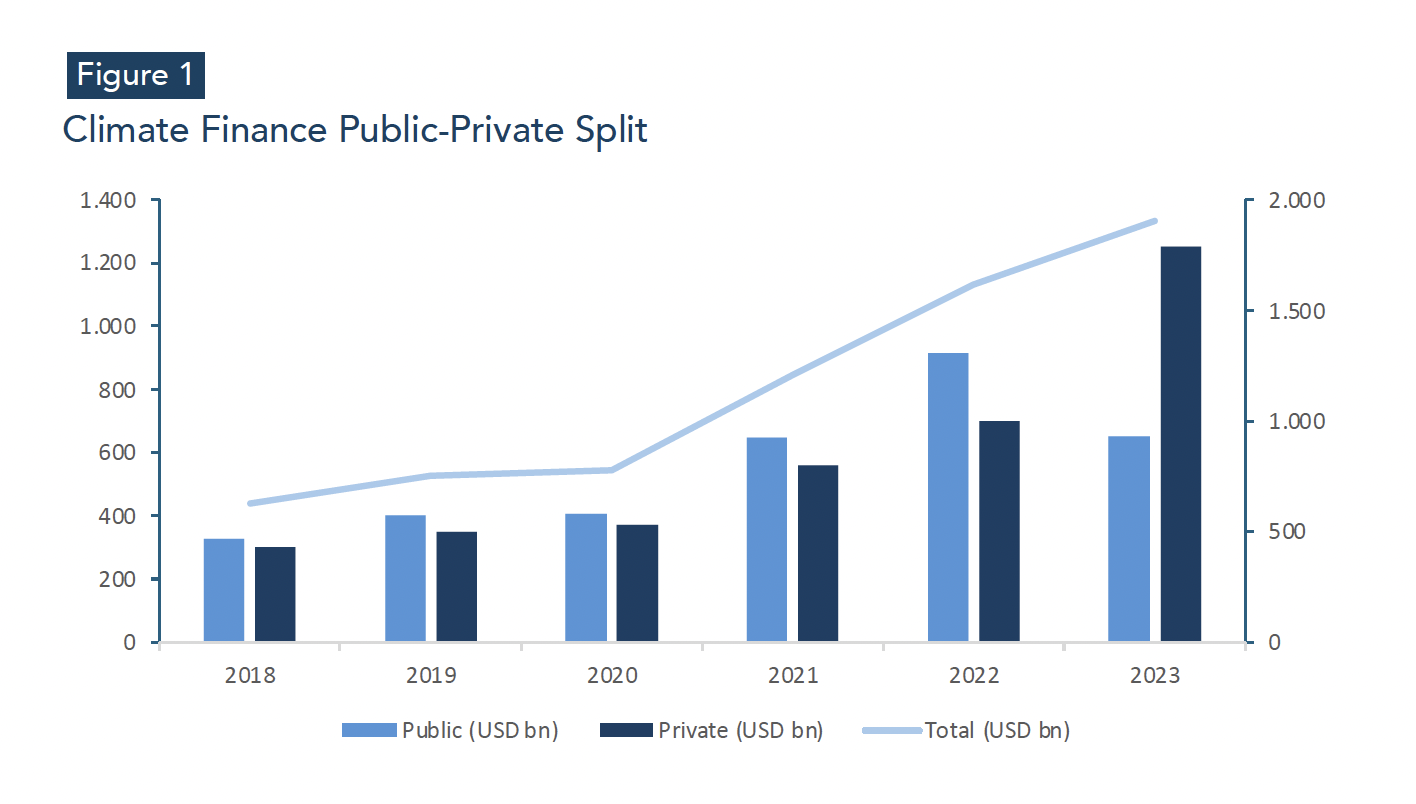

The annual split between public and private climate finance from 2013 through 2023 reveals a decisive structural shift in who is driving climate investment. In the early part of the period, public and private contributions were broadly comparable in scale, with private flows totaling approximately USD 177 billion against a public contribution of USD 154 billion in 2013. By 2023, that balance had fundamentally changed: private finance reached USD 1.27 trillion, accounting for 66% of total climate flows, while public finance, at USD 659 billion, had grown substantially in absolute terms but had been far outpaced in relative weight. However, even at record levels, current climate finance covers less than a third of what science demands, a gap that no instrument or sector trend visible in the data comes close to bridging, and one that must anchor all policy discussions about mobilization strategy going forward.

The evolution of private sector contributions to climate finance (Figure 1) between 2012 and 2024 reflects not merely a gradual scaling of capital flows, but a series of discrete structural shifts shaped by landmark policy developments, macroeconomic shocks, and a deepening institutional architecture around climate risk. In the early years of the observed period, between 2012 and 2016, private sector contributions remained modest and relatively undifferentiated. Credit lines and direct investment in companies and Special Purpose Vehicles (SPVs) constituted the primary channels, while instruments such as guarantees, syndicated loans, and shares in Collective Investment Vehicles (CIVs) played a marginal role. This early-period flatness is consistent with the broader state of climate finance architecture at the time: fragmented, largely donor-driven, and not yet anchored by the kind of credible long-term policy signals necessary to attract large-scale private capital. The growth rate of private climate finance was slower than that of the public sector and remained far below the pace needed to meet a 1.5°C global warming scenario, with at least USD 4.3 trillion in annual finance flows required by 2030 (Butler, 2024).

The first major inflection point emerges around 2017, with a pronounced rise in guarantees alongside sustained growth in direct investment in companies and SPVs. This shift coincides directly with the implementation phase of the 2015 Paris Agreement and the establishment of the Network for Greening the Financial System (NGFS, 2024) by eight central banks and supervisory authorities, a signal that climate risk was beginning to be treated as a systemic financial concern rather than a peripheral development issue. The surge in guarantees during this period is particularly revealing as public actors sought to de-risk the investment space and crowd in reluctant private capital, risk-mitigation instruments naturally rose to prominence. Public institutions, multilateral development banks, climate funds, and philanthropies assumed first-mover and longer-term risk, funded the development of surrounding infrastructure, and built enabling environments, a dynamic that the dominance of guarantees in this period reflects with precision (Li, et.al, 2025).

The period between 2018 and 2020 saw direct investment in companies and SPVs reach its pre-pandemic peak, before the COVID-19 shock introduced a significant disruption. Climate finance growth slowed in many emerging and developing economies amid pandemic-constrained public budgets, interruptions to project implementation, and worsened borrowing conditions, with sub-Saharan Africa and Latin America and the Caribbean particularly affected, their climate finance in 2020 falling below 2018 levels (Baysa, et.al, 2024). Yet the recovery that followed was both swift and structurally consequential. From 2021 onward, guarantees rebounded strongly and direct investment regained momentum, driven by green recovery stimulus packages launched across major economies. Annual climate finance more than doubled between 2018 and 2022, rising from USD 674 billion to USD 1.46 trillion (Naran, et.al, 2022), a trajectory clearly reflected in the upward momentum visible in (Figure 2) across this period.

The most recent phase, spanning 2022 to 2024, is characterized by a broad-based surge across multiple investment vehicles, with guarantees reaching their highest observed levels and syndicated loans emerging as a meaningfully growing instrument for the first time. This acceleration maps onto a new era of green industrial policy, anchored most prominently by the United States' Inflation Reduction Act and equivalent frameworks across the European Union and Asia-Pacific. The World Bank Group alone delivered a record USD 42.6 billion in climate finance in fiscal year 2024, a 10% increase on the previous year, with IFC contributing USD 9.1 billion in long-term climate finance through its private sector arm (Broché, 2024). The rise of syndicated loans signals a maturation of the climate finance market: as projects grow in scale and complexity, multi-lender structures have deepened, drawing in a broader range of financial institutions and expanding market infrastructure.

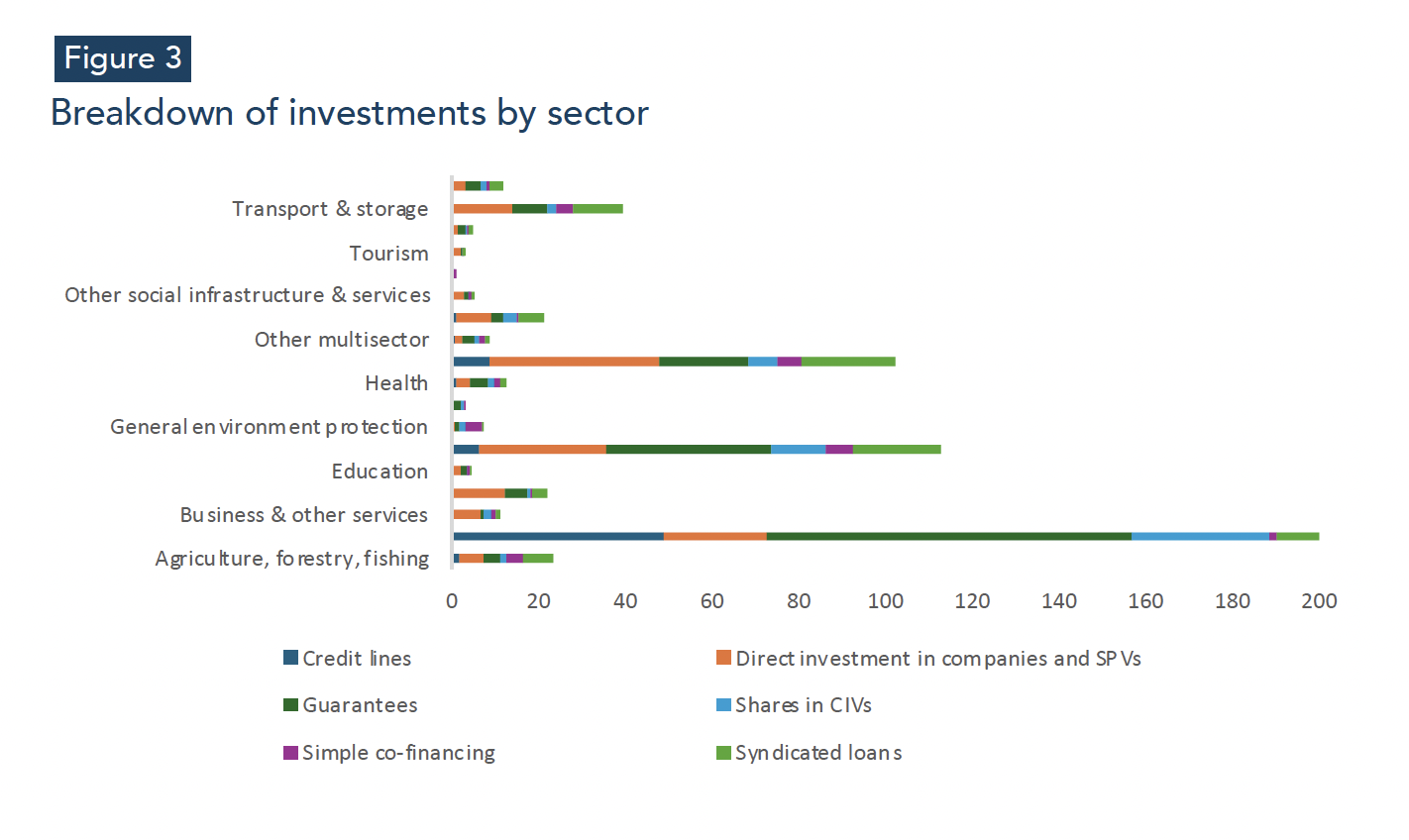

When the lens shifts from investment vehicles to sectoral distribution, a strikingly uneven picture emerges. Figure 3 reveals that private climate finance has not flowed evenly across the economy, but has instead concentrated heavily in a small number of commercially attractive sectors. Business and other services dominates by a considerable margin, absorbing close to 200 units of aggregate investment, driven primarily by guarantees, shares in CIVs, and credit lines. Health and General environment protection follow at roughly 100 units each, also sustained substantially by guarantees, suggesting that public risk absorption has been the decisive factor enabling private entry into these sectors as well. This concentration pattern is consistent with global trends: energy and transport, the two largest-emitting sectors where private finance dominates, continue to attract the majority of climate flows, with energy drawing 44% of total mitigation finance and transport 29% (Naran, et.Al, 2024) while sectors with enormous mitigation and adaptation potential remain chronically underfunded.

Figure 2 confirms this gap with particular clarity in the case of agriculture, forestry, and fishing, which attract a modest and highly fragmented allocation, relying heavily on credit lines and direct investment in SPVs, with minimal presence of guarantees or syndicated loans that have propelled growth elsewhere.

The data presented across both figures points to a structural tension that policymakers can no longer afford to treat as a secondary concern. The growing dominance of guarantees as the preferred instrument of private climate finance confirms that private capital remains fundamentally risk-averse: while guarantees have proven effective in mobilizing volume, the increasing dependence on public balance sheets to underwrite private participation raises serious questions about fiscal sustainability and scalability, particularly in a context where public budgets in emerging and developing economies are already under strain.

2. The new governance of climate finance and its implications

The years 2024 and 2025 have produced a paradox in climate finance: private climate capital has broken records, while the public climate architecture has fractured. Understanding what this means for the transition requires examining not only who holds capital, but who holds authority over how it flows.

Climate finance encompasses local, national, and transnational funding from public, private, and alternative sources aimed at supporting actions to mitigate and adapt to climate change. The Convention, the Kyoto Protocol, and the Paris Agreement call on wealthier Parties to provide financial assistance to those that are less endowed and more vulnerable, reflecting the fact that countries differ greatly in both their contributions to climate change and their capacity to address its impacts. In practice, however, climate finance is a complicated landscape, populated by a wide range of stakeholders with differing levels of power and influence, making it difficult to navigate for those trying to access it or push for greater accountability.

The retreat of public governance and the rise of private authority

The institutional architecture governing climate action is contracting at precisely the moment private capital is expanding. On January 20, 2025, President Trump signed an executive order withdrawing the United States from the Paris Agreement for the second time (Hillier, 2025), simultaneously rescinding the US International Climate Finance Plan and directing agencies to cease or revoke any financial commitment made under the UNFCCC. The immediate fiscal consequence was sharp: the withdrawal reduced the convention's annual operating budget by 21%, leading to reduced conference hours and the cancellation of regional events (Larsen, Alayza, and Caldwell 2025). More consequentially, it ratifies a pattern already visible across development finance institutions and G20 governments: public actors scaling back the direct deployment of climate capital faster than they put alternative governance mechanisms in place to replace it.

On the other side of this paradox, a growing number of major corporations and financial institutions have backed away from their formal climate commitments (Convergence, 2024), yet the capital itself kept flowing, directed by mandates and market logic rather than policy. That divergence between institutional retreat and capital persistence exposes the inadequacy of treating climate governance as synonymous with government action.

Private actors, including asset managers, development finance institutions, sovereign wealth funds, and industry coalitions, have stepped into this space, gaining increasing authority over the climate transition. This authority is not rhetorical. Climate governance encompasses at least four overlapping functions: (1) allocating capital across sectors and geographies; (2) pricing risk to determine where investment is commercially viable; (3) setting standards that define credible climate action; and (4) shaping narratives that influence what governments, investors, and civil society consider legitimate or possible. Today, private actors wield significant influence over all four. BlackRock's own framing illustrates the logic: sustainability is no longer something addressed after strategic investment decisions have been made, but is indispensable to making them (Climate Policy Initiative, 2024). When the world's largest asset manager internalises climate into portfolio construction as a matter of fiduciary duty, it is not implementing an external policy but rather making policy for the companies in its portfolio, the sectors it favours, and the geographies it prices as investable.

Accountability gaps, distributional risks, and the path forward

Record volumes of private climate finance are not synonymous with a governed or just transition. The concentration of private authority over these governance functions raises a critical and underexamined risk: the absence of public accountability and transparent decision-making. Public climate governance, for all its limitations, operates within frameworks of democratic legitimacy — governments are elected, international agreements are ratified, and public institutions are subject to audit, parliamentary scrutiny, and freedom-of-information obligations. Private actors do not face these constraints. Their climate commitments are largely self-declared, their methodologies proprietary, and their motivations structurally mixed, combining genuine sustainability objectives with fiduciary obligations to maximise returns for shareholders or beneficiaries (New Climate.org, 2025).

This matters because the institutions that define green standards, rate climate risk, and allocate transition capital are not neutral and hold direct financial interests in the outcomes of the markets they influence. ICMA's Green Bond Principles, for instance, have become the de facto global standard for the $5 trillion sustainable bond market (Johnson, 2023), yet this standard-setting role is carried out not by an intergovernmental body but by an industry association whose membership comes largely from the financial sector itself (ICMA, 2023). When a major asset manager endorses a particular taxonomy or disclosure framework, it simultaneously shapes the regulatory environment for products it manages and sells. This conflict is structural rather than incidental, reflecting the embedded incentives of private authority over public goods (Braun, 2021; Gabor, 2021). When private actors define what counts as "transition" activity and self-certify compliance, the risk extends beyond individual greenwashing to systemic legitimacy erosion, where the architecture of climate-labelled finance is perceived less as governance and more as marketing (Ali, et.Al, 2026).

The credibility problem is not merely technical. It reflects a structural tension: the institutions most active in designing transition finance standards are also among its primary beneficiaries, creating incentives to prioritise market growth over environmental rigour. Both the Transition Finance Market Review (Gov. UK, 2024) and OECD assessments (OECD, 2023) have flagged that voluntary frameworks risk becoming a floor rather than a ceiling, with actors claiming alignment to Paris while deferring actual emissions reductions.

Private climate governance also produces a democratic deficit in transition planning. Critical decisions on energy systems, industrial policy, and the distribution of transition costs and benefits are increasingly not made by legislatures or multilateral bodies. Communities most affected such as coal-dependent regions, energy-poor populations, small island states, are largely absent from these processes. This lack of procedural legitimacy is not merely a normative concern; it is a practical governance risk (Kuzembo, et.Al, 2016). Transitions lacking democratic legitimacy are vulnerable to political backlash, as demonstrated by the anti-ESG legislative movement in the United States between 2023 and 2025 (Hanawalt and Fitch, 2025).

The distributional consequences are equally concerning. Private capital's risk models embed structural inequity into the architecture of the global transition: the countries least responsible for historical emissions face the highest financing barriers to decarbonization. Incoherent climate governance can thus be directly linked to higher costs of capital and increasing inequalities in access to growth opportunities, the opposite of what climate justice requires.

These developments make the current moment particularly consequential. The 2025 US setbacks coincide with key milestones: COP30 in Belém, revised Nationally Determined Contributions, and the first Global Stocktake follow-up cycle (Asian Development Bank, 2024; UNFCCC, 2023). The central question is whether the resulting leadership vacuum will catalyse stronger coordination among committed nations or accelerate the devolution of climate governance toward non-state actors whose accountability remains unresolved.

Addressing this requires a new understanding of climate governance that should be broader than regulation, encompassing not only rules, but the power of investors and institutions to direct capital and shape the trajectory of the transition. This points toward three interlinked principles of open governance: (1) transparency, through public access to information, open data portals, and budget transparency mechanisms; (2) participation, through inclusive formal engagement in decision-making; and (3) accountability, through audit institutions, ombuds offices, and grievance redress mechanisms.

3. A closer analysis of three models of Private Climate Governance and their limits

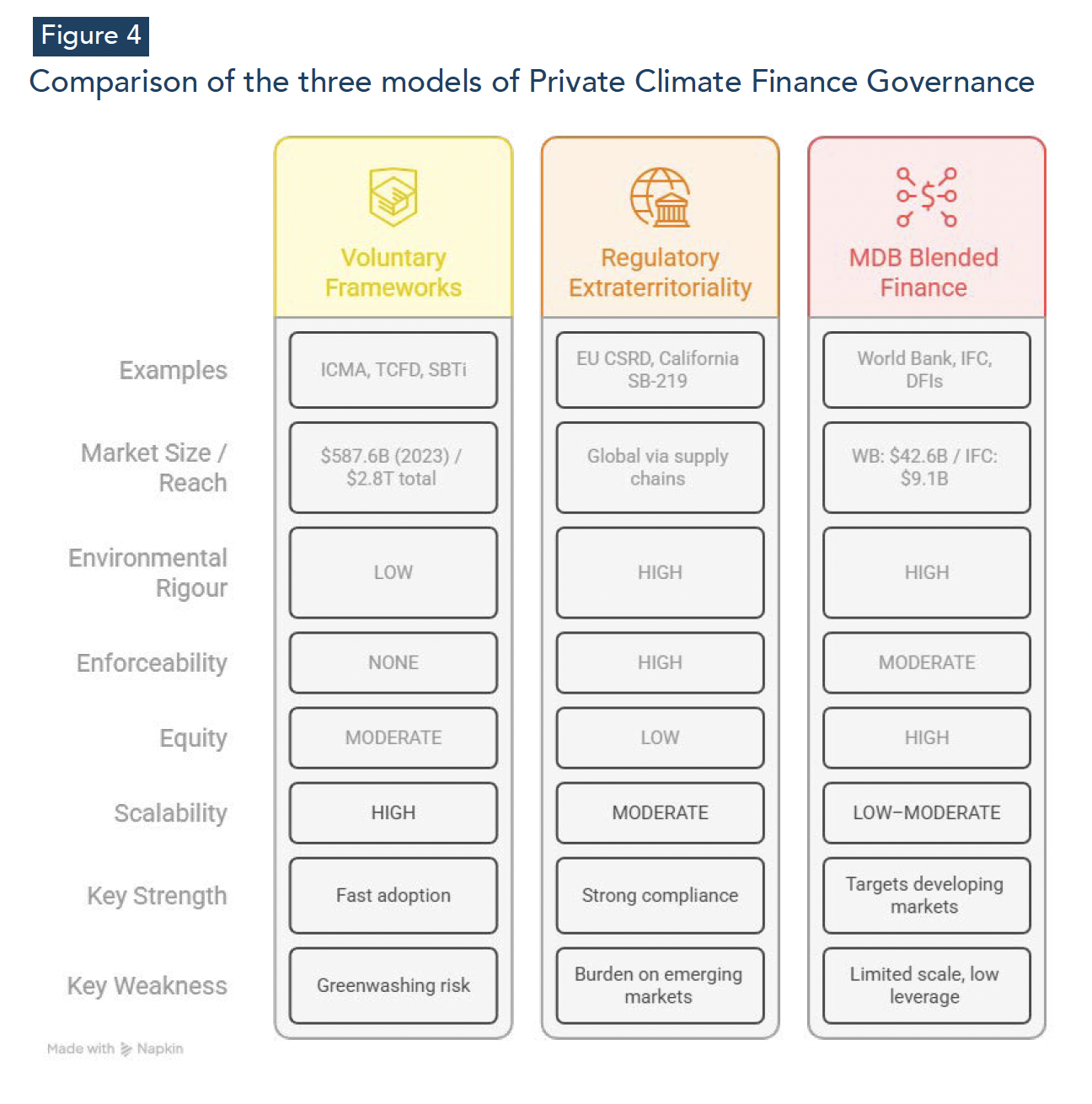

As the private sector is taking a more predominant role in climate finance, this pattern carries governance risks. However, there are mechanisms that can allow for an efficient governance of private climate capital. Among these models, there are voluntary frameworks, regulatory extraterritoriality, and MDB-intermediated blended finance. Each with a specific role and criteria, but all aim to ensure environmental rigour, enforceability, equity, and scalability.

Model 1 — Voluntary Frameworks: Necessary but Insufficient

The first and most prevalent model of private climate governance operates through voluntary standards and disclosure frameworks, of which ICMA's Green Bond Principles, the Task Force on Climate-related Financial Disclosures (TCFD), and the Science Based Targets initiative (SBTi) are the most architecturally significant. Together these frameworks have shaped the contours of the $5 trillion sustainable bond market, standardized the language through which corporations communicate climate risk to investors, and established the reference points against which institutional climate commitments are assessed (ICMA, 2025).

Their adoption has been remarkable in scale and speed. Global organizations issued $587.6 billion in green bonds in 2023, reaching $2.8 trillion in cumulative total (Kidane, 2025), a market that did not meaningfully exist fifteen years ago and that the ICMA Green Bond Principles helped constitute. In November 2025, ICMA published its Climate Transition Bond Guidelines, introducing a standalone label aimed at high-emitting sectors in energy, steel, cement, and chemicals that have found it difficult to access the sustainable finance market (Lehman-Grube, et.Al, 2024). This also highlights that voluntary frameworks continue to evolve and extend their reach into harder corners of the economy.

Yet the architecture of voluntary governance contains a structural flaw that it relies on the same institutions it is meant to govern to police their own compliance. The ICMA Green Bond Principles explicitly focus on disclosure and transparency, believing that investors themselves should decide whether something is green enough (Bretton Woods Project, 2024). This formulation is philosophically coherent as a market principle but functionally inadequate as a governance principle. When the standard-setter delegates the determination of adequacy to the market, it creates the conditions for what the literature describes as a race to the bottom on ambition: actors claim alignment with Paris while deferring actual emissions reductions, and the framework accommodates them because it has no mechanism to do otherwise.

The OECD and the UK Transition Finance Market Review have both flagged this risk explicitly, stating that voluntary frameworks risk becoming a floor rather than a ceiling, with the green label functioning more as a market signal than an environmental guarantee.

The problem is also compounded by the institutional conflict of interest at the heart of standard-setting. ICMA is an industry association whose membership comes primarily from the financial sector, the same sector that issues, underwrites, and distributes the green bonds whose standards ICMA sets. As green bond issuance grows, so does the risk of greenwashing, bonds labelled green without rigorous criteria for what qualifies (Hedley, 2025). However, the body best positioned to tighten those criteria has structural incentives to maintain market growth over environmental rigour. Voluntary frameworks have created a common language, expanded market infrastructure, and brought climate considerations into mainstream investment practice. But as the primary governance mechanism for trillions of dollars of private climate capital, they are insufficient.

Model 2 — Regulatory Extraterritoriality: Powerful but Inequitable

The second model operates through binding mandatory disclosure and due diligence requirements promulgated by major jurisdictions and enforced — through market access — beyond their borders. The European Union's Corporate Sustainability Reporting Directive (CSRD) and California's SB-219 represent the most consequential instances of this model currently in operation.

They both have significant outreach. California's requirements apply to enterprises with annual revenue of more than $1 billion doing business in California, as well as those with more than $500 million, with extraterritorial effects extending to US and non-US businesses alike (Gemayel, et.Al,, 2025) meaning that a company domiciled anywhere else in the world with California market exposure is now subject to mandatory GHG disclosure requirements set by a US state legislature. On the other hand, the EU's CSRD and Corporate Sustainability Due Diligence Directive similarly have extraterritorial effects and apply to US businesses, both directly and through indirect effects on corporate governance (IMF, 2025), covering thousands of companies globally through supply chain obligations. Between 2019 and 2024, the EU published 108 pieces of legislation under the European Green Deal (Okoronkwo, et.Al, 2024), establishing the most comprehensive mandatory climate governance architecture in the world.

The enforcement mechanism is real: under California SB-219, penalties for non-compliance with GHG emission requirements can result in fines of up to $500,000 per reporting year (Besser, 2025), while CSRD violations can attract penalties up to 5% of net worldwide turnover (PwC,2025). This binding character distinguishes this model sharply from voluntary frameworks and gives it genuine governance authority.

But its limits are equally structural. The extraterritorial reach of CSRD and California's legislation disproportionately burdens firms in emerging markets, where institutional capacity to prepare complex sustainability disclosures is constrained, audit infrastructure is less developed, and the compliance cost falls heaviest on companies least able to absorb it. A large asset manager in Frankfurt or a multinational headquartered in London can dedicate compliance teams to CSRD reporting; a mid-sized manufacturing firm in Ghana or Indonesia supplying into European value chains faces the same obligation with a fraction of the resources. The standard is formally universal but functionally inequitable in design.

Eventually, companies in emerging markets that cannot meet compliance requirements risk being de-listed from European supply chains or cut from institutional investor portfolios, accelerating the capital concentration in high-income countries that the first section of this paper already documents. Furthermore, the CSRD and CS3D have recently faced serious political opposition, with the Trump administration calling them a serious and unwarranted regulatory overreach, and far-right groups pushing for repeal or delay until 2030 and 2040 respectively (Thomson, 2026). This serves as a reminder that extraterritorial regulation, however well-designed, is fragile to political reversal in the jurisdictions that anchor it. The EU's own Omnibus simplification package (Council of the European Union, 2026) has already introduced implementation delays for second and third-wave companies, signaling that even the most ambitious mandatory disclosure framework is subject to the political economy of competitiveness concerns.

Model 3 — MDB-Intermediated Blended Finance: Most Promising, Most Underdeveloped

The third model operates through multilateral development banks, development finance institutions, and climate funds that use concessional or public capital to de-risk private investment and direct it toward public-good outcomes in emerging and developing economies. Blended finance represents the most structurally sophisticated attempt to reconcile private capital's return requirements with climate finance's distributional obligations.

Its logic is sound and its track record is the strongest of the three models. Leverage ratios for MDBs average $1 of MDB capital mobilising $0.75 of private finance, though this can be as low as $0.37 in low-income countries (Hirschel‑Burns, et.Al, 2024). Private sector investment into climate blended finance increased by almost 200% in 2023 (World Bank, 2024), in addition to a 60% increase in commercial financing from development finance institutions and multilateral development banks. The World Bank Group alone delivered a record $42.6 billion in climate finance in fiscal year 2024, and the IFC's private sector arm contributed $9.1 billion in long-term climate finance. These figures demonstrate the model's capacity for scale when adequately capitalised.

Yet the aggregate data exposes how far the model remains from the scale required. Despite positive signals from the blended finance market in 2024, a lack of structural standardisation continues to slow the rollout and replication of blended structures, with concessional capital in many cases mobilising public commercial funding from MDBs and DFIs rather than private investment (Climate funds update, 2024), a circularity that undermines the model's core rationale. Critical gaps remain, particularly in adaptation finance and the mobilisation of private capital for climate resilience projects. Only 32 adaptation blended finance transactions were recorded between 2021 and 2023, with a total value of $3.5 billion, compared to 132 climate mitigation transactions with a total value of $26 billion, a ratio of 7.4 to 1 that maps directly onto the adaptation finance gap documented in Section I.

The structural constraints are well-diagnosed but inadequately addressed. Risk-sharing and mitigation tools such as guarantees, first-loss capital, and FX hedging are insufficiently scaled; many transactions are bespoke, with a lack of structural standardisation slowing replication; and prudential regulations do not fully recognise MDB guarantees for capital relief. This means that even when MDBs successfully de-risk a transaction, the private capital that responds may receive no regulatory incentive to participate.

MDBs and DFIs are under increasing pressure to improve their headroom or lending capacity while increasing private sector mobilisation targets, particularly as the US reduces its engagement in multilateral institutions, a double bind in which the most effective model is being simultaneously asked to do more and given fewer resources to do it with.

4. The Systemic Gap: What No Single Model Provides

The figure above, and the analysis of the three models provide a map of complementary and partially overlapping inadequacies. Each model addresses a particularity: voluntary frameworks create common language and market infrastructure; regulatory extraterritoriality establishes binding floors and enforcement mechanisms; blended finance channels capital toward public-good outcomes in underserved geographies. Together they have produced the record climate finance volumes documented in Section I.

However, when the three models are analyzed together, they still leave three critical governance gaps unaddressed. First, none of the three models has a reliable mechanism to ensure that the capital flowing through them reaches adaptation rather than mitigation or reaches the most vulnerable countries rather than the most commercially attractive ones. The distributional logic of each model, market adoption for voluntary frameworks, market access for regulatory extraterritoriality, commercial viability for blended finance, systematically privileges investable geographies and bankable sectors. Second, none of the three models provides just accountability to the communities most affected by the transition. Standard-setting bodies are industry-led, regulatory frameworks are designed by and for high-income jurisdictions, and MDB governance structures remain dominated by shareholder voting rights tied to capital contributions. Third, and most fundamentally, there is no architecture that coordinates the three models toward a shared set of outcomes: no mechanism that ensures voluntary commitments are consistent with binding disclosure requirements, or that blended finance instruments are directed by the same taxonomy that green bond markets use to define eligible investment (Albuquerque, et.Al, 2023).

What is missing is not another instrument. It is the overarching governance architecture that could make the existing instruments coherent, accountable, and adequate to the scale of what the transition demands. That is the gap this paper argues must be closed, and closing it requires treating climate governance not as a technical question of instrument design, but as a political question of who holds authority over where capital flows and on whose terms.

Conclusion

In both financial and political terms, private climate finance will play a decisive role in the global energy transition over the coming decade. The record volumes documented in this paper represent a clear structural shift in who funds the transition and on what terms. However, volume does not translate into governance. The central finding is not that private climate finance has failed, but that it has succeeded in ways that do not automatically serve the objectives climate finance is meant to achieve.

The central tension this paper has traced is not between public and private finance, but between capital volume and governance authority. Record flows of private climate finance have not resolved, and in some respects have deepened, the question of who holds legitimate authority over where the transition goes, who bears its costs, and who captures its benefits. That question is now more open than at any point since Paris, precisely because the institutional architecture that once anchored it is contracting.

The three governance models examined here are not failures. They are partial solutions operating without coordinating logic, each optimized for the actors that designed them rather than for the communities most exposed to climate risk. Closing that gap requires accepting an uncomfortable premise: that the governance of private climate capital is a political problem, not a technical one. Instrument design, disclosure standards, and blended finance structures matter, but they are insufficient as long as the authority to define what counts as a credible transition, and to enforce it, remains concentrated in institutions with structural incentives to prioritize market growth over environmental and distributional rigor.

What the current moment demands is still more capital, but also the political will to build governance architecture with real accountability, geographic equity, and democratic legitimacy at its core. COP30 and the revised NDC cycle offer a narrow window to move in that direction. Whether that window is used will determine not the quantity of climate finance, but the transition it actually delivers.

Bibliographic references

Anantharajah, K., and A. Setyowati. 2022. “Beyond Promises: Realities of Climate Finance Justice and Energy Transitions in Asia and the Pacific.” Energy Research & Social Science 89 (July). https://www.sciencedirect.com/science/article/pii/S2214629622000561.

Butler, C. 2024. “Closing the climate finance gap”, Chatham House, (November). https://www.chathamhouse.org/2024/11/closing-climate-finance-gap/04-increasing-demand-climate-finance

NGFS, 2024. “Annual Report 2024”, Welcome to the NGFS website | Network for Greening the Financial System

Li, Shengzi, Valerio Micale, and Maddy Taylor. 2025. Tracking the Transition: Global Private Financial Institutions’ Progress toward Net Zero. November 6, 2025. Climate Policy Initiative. https://www.climatepolicyinitiative.org/publication/tracking-the-transition-global-private-financial-institutions-progress-toward-net-zero/.

Naran, Baysa, Barbara Buchner, Matthew Price, Sean Stout, Maddy Taylor, and Dennis Zabeida. 2024. Global Landscape of Climate Finance 2024. Climate Policy Initiative. https://www.climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2024/

Broché, Ben. 2024. “Emerging Trends, Challenges, and Opportunities in Climate Finance.” The Global Innovation Lab for Climate Finance, September 17, 2024. https://www.climatefinancelab.org/news/emerging-trends-challenges-and-opportunities-in-climate-finance/

Hillier, Debbie. 2025. “Can the Private Sector Plug the Adaptation Finance Gap?” World Economic Forum, June 10, 2025. https://www.weforum.org/stories/2025/06/can-the-private-sector-plug-the-adaptation-finance-gap/

Larsen, Gaia, Natalia Alayza, and Molly Caldwell. 2025. “How to Get Finance Flowing to Climate Adaptation.” World Resources Institute, November 13, 2025. https://www.wri.org/insights/how-get-finance-flowing-climate-adaptation.

Convergence. 2024. “Climate Blended Finance Market Sees 120% Increase Driven by Private Sector, New Report from Convergence Finds.” Press release, October 30, 2024. https://www.convergence.finance/news-and-events/news/climate-blended-finance-market-sees-120-increase-driven-by-private-sector-new-report-from-convergence-finds.

Climate Policy Initiative. 2024. Understanding Global Concessional Climate Finance 2024. Climate Policy Initiative. https://www.climatepolicyinitiative.org

NewClimate Institute. 2024. Climate Change Performance Index 2025. Bonn, Germany: NewClimate Institute. https://www.newclimate.org/publications/climate-change-performance-index-2025

Johnson, Lamar. “US Sustainable Funds Saw Net Outflows in 2023: Morningstar.” ESG Dive, February 6, 2024. https://www.esgdive.com/news/us-sustainable-funds-net-outflows-2023-morningstar

International Capital Market Association (ICMA). Green Bond Principles (GBP), June 2025. Zurich: ICMA, 2025. https://www.icmagroup.org/sustainable-finance/the-principles-guidance/green-bond-principles-gbp/.

Braun, Benjamin (2021). Asset manager capitalism as a corporate governance regime. In J. Hacker, A. Hertel-Fernandez, P. Pierson, & K. Thelen (Eds.), The American Political Economy: Politics, Markets, and Power (pp. 270–294). Cambridge University Press.

Gabor, Daniela. “The Wall Street Consensus.” Development and Change 52, no. 3 (May 2021): 429–459. https://doi.org/10.1111/dech.12645

Ali, Amjad, Jairaj Gupta, and Emad Elkhashen. “Greenwashing in Sustainability Disclosures: A Systematic Review of Manifestations, Measurement, and Corporate Finance Implications.” SSRN Scholarly Paper, January 16, 2026. https://ssrn.com/abstract=6080506

GOV.UK, 2023, Department for Energy Security and Net Zero and HM Treasury. Transition Finance Market Review. Published December 18, 2023. https://www.gov.uk/government/publications/transition-finance-market-review.

OECD, 2023, OECD Guidance on transition finance, https://www.oecd.org/content/dam/oecd/en/publications/reports/2022/10/oecd-guidance-on-transition-finance_ac701a44/7c68a1ee-en.pdf

Kuzemko, Caroline, Matthew Lockwood, Catherine Mitchell, and Richard Hoggett. 2016. “Governing for Sustainable Energy System Change: Politics, Contexts and Contingency.” Energy Research & Social Science 10: [page range]. https://doi.org/10.1016/j.erss.2015.12.022.

Hanawalt, Cynthia, and Andy Fitch. “State Anti‑ESG Movement Evolves to Target Investor Access.” Climate Law Blog, August 21, 2025. https://blogs.law.columbia.edu/climatechange/2025/08/21/state-anti-esg-movement-evolves-to-target-investor-access/

Asian Development Bank. Asia‑Pacific Climate Report 2024: Catalyzing Finance and Policy Solutions. Manila, Philippines: Asian Development Bank, 2024. https://www.adb.org/publications/asia-pacific-climate-report-2024

United Nations Framework Convention on Climate Change (UNFCCC). 2023 NDC Synthesis Report: Synthesis of Nationally Determined Contributions under the Paris Agreement. Bonn: UNFCCC, 2023. https://unfccc.int/ndc-synthesis-report-2023

International Capital Market Association (ICMA). 2025. “The Executive Committee of the Principles Announces a Practitioner’s Guide on Sustainable Bonds for Nature, alongside Updates to Existing Guidance.” ICMA News in Brief, June 26, 2025. https://www.icmagroup.org/News/news‑in‑brief/the‑executive‑committee‑of‑the‑principles‑announces‑a‑practitioners‑guide‑on‑sustainable‑bonds‑for‑nature‑alongside‑updates‑to‑existing‑guidance/

Kidane, Luam. 2025. “Dependency by Design: How the JET‑IP Structures South Africa’s Energy Future.” Transnational Institute, November 20, 2025. https://www.tni.org/en/article/dependency‑by‑design‑how‑the‑jet‑ip‑structures‑south‑africas‑energy‑future

Lehmann‑Grube, Katrina, Imraan Valodia, Julia Taylor, and Sonia Phalatse. “What Happened to the Just Energy Transition Grant Funding?” Wits University, March 28, 2024. https://www.wits.ac.za/news/latest‑news/research‑news/2024/2024‑03/what‑happened‑to‑the‑just‑energy‑transition‑grant‑funding.html

Bretton Woods Project. 2023. “World Bank’s $1 Billion Loan to South Africa Risks Undermining Just Transition by Doubling Down on ‘De‑Risking’ Private Capital.” Bretton Woods Project, October 23, 2023. https://www.brettonwoodsproject.org/2023/10/world‑banks‑1‑billion‑loan‑to‑south‑africa‑risks‑undermining‑just‑transition‑by‑doubling‑down‑on‑de‑risking‑private‑capital/.

Organisation for Economic Co‑operation and Development (OECD). 2013. Action Plan on Base Erosion and Profit Shifting. Paris: OECD Publishing. https://www.oecd.org/content/dam/oecd/en/publications/reports/2013/07/action‑plan‑on‑base‑erosion‑and‑profit‑shifting_g1g30e67/9789264202719‑en.pdf.

European Commission. 2025. “Corporate Sustainability Reporting Directive (CSRD).” Accessed Month Day, Year. https://finance.ec.europa.eu/regulation‑and‑supervision/financial‑services‑legislation/implementing‑and‑delegated‑acts/corporate‑sustainability‑reporting‑directive_en

California Legislature. 2023–2024. Senate Bill No. 219. Accessed Month Day, Year. https://leginfo.legislature.ca.gov/faces/billTextClient.xhtml?bill_id=202320240SB219

PricewaterhouseCoopers (PwC). The Corporate Sustainability Due Diligence Directive. Zürich: PwC Switzerland, 2025. https://www.pwc.ch/en/publications/2025/the‑corporate‑sustainability‑due‑diligence‑directive.pdf

Gemayel, Edward R., Samuele Rosa, Vidhi Maheshwari, Christoph Ungerer, and Peter Lindner. Laying the Ground for Scaling up Climate Finance in Sub‑Saharan Africa, WP/25/99 (May 2025). International Monetary Fund, 2025.

Besser, Lauren. 2025. “A Comparative Analysis of California Senate Bill 219 and Other Global Reporting Regulatory Frameworks.” GSI Environmental Inc., June 24, 2025. https://www.gsienv.com/a‑comparative‑analysis‑of‑california‑senate‑bill‑219‑and‑other‑global‑reporting‑regulatory‑frameworks/

Thomson, Daniel. “Omnibus I — the European Union Concludes CSDDD and CSRD Reforms.” Clifford Chance (Business & Human Rights Insights), February 24, 2026. https://www.cliffordchance.com/insights/resources/blogs/business-and-human-rights-insights/2026/02/omnibus-i-the-european-union-concludes-csddd-and-csrd-reforms.html

Council of the European Union. “Simplification of EU Rules.” Consilium, accessed April 2026. https://www.consilium.europa.eu/en/policies/simplification/

Hirschel‑Burns, Tim, and Rishikesh Ram Bhandary. A Roadmap for Unlocking the Potential of Multilateral Development Banks Exists – and the G20 Just Endorsed It. Boston University Global Development Policy Center, December 9, 2024. https://www.bu.edu/gdp/files/2024/10/G20-MDBs-Report-FIN.pdf

Climate Funds Update. CFF12‑2024‑ENG‑SIDS‑DIGITAL. Climatefundsupdate.org, 2024. https://climatefundsupdate.org/wp-content/uploads/2024/04/CFF12-2024-ENG-SIDS-DIGITAL.pdf

Albuquerque, Marianna, Rim Berahab, Sabrine Emran, Rogerio Studart, and Afaf Zarkik. 2023. A Common ESG Language to Unlock Funding for Sustainable Infrastructure Projects in Developing Economies. T20 Policy Brief, June 2023. Policy Center for the New South and ThinkTwenty (T20) India. https://www.policycenter.ma/publications/common‑esg‑language‑unlock‑funding‑sustainable‑infrastructure‑projects‑developing