Publications /

Opinion

Scarcity of inputs and goods has been felt all over the world because of disruptions to global value chains since the beginning of the pandemic. Factory closures in China at the beginning of 2020, lockdowns in many countries and, subsequently, congestion in logistics networks for transporting goods, capacity constraints in the face of sudden increases in demand, and labor shortages, have combined to negatively affect the availability of inputs and products worldwide.

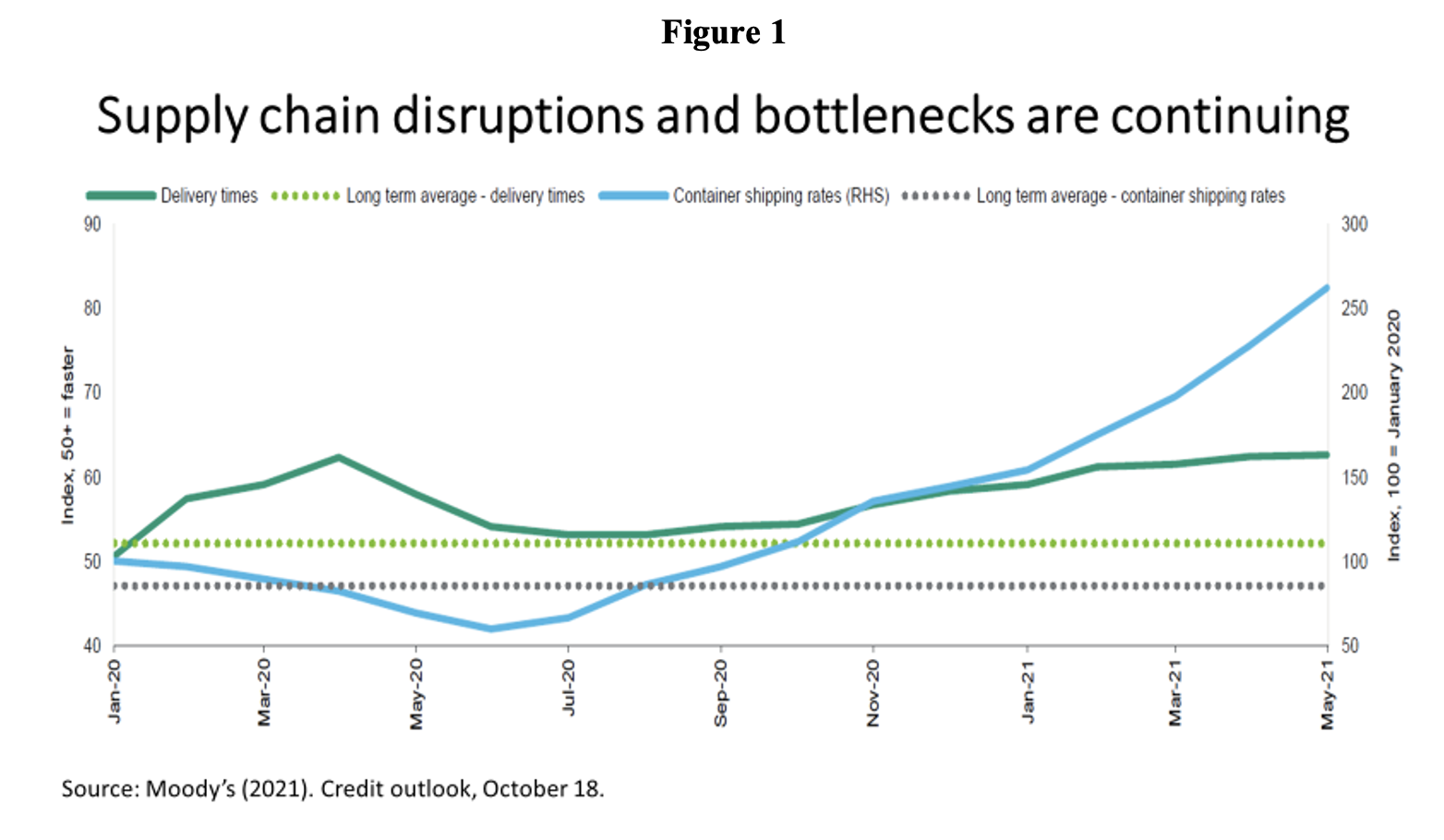

Higher freight prices and unprecedented delays in parcel delivery times have become widespread. Figure 1—from Moody’s Credit Outlook report of October 18—shows global manufacturing suppliers’ delivery times as measured by the Purchasing Managers’ Index (PMI), and container shipping rates as measured by the Harper Petersen Charter Rates Index. PMI data are inverted by subtracting data from 100; therefore, increasing (decreasing) PMI data indicate faster (slower) delivery times. Container shipping rates are monthly averages of weekly data. Global supply chain disruptions have been at historic highs and shipping and logistics constraints are not yet abating.

These disruptions have consequences for inflation and GDP. In the United States, the Federal Reserve’s (Fed) ‘beige book’ released two weeks ago pointed to a slowdown in the pace of GDP growth in the third quarter of 2021 because of disruptions in supply chains, labor shortages, and uncertainty around the Delta variant of COVID-19.

In the meantime, inflation has risen. The consumer price index that serves as the main reference for U.S. monetary policy, released on October 29, 2021, showed an increase of 4.4% in the last twelve months, above the rate that serves as a reference as the average pursued by the Fed.

Higher inflation has been a global phenomenon, even if with different intensities and multiple determinants. Several emerging-market and developing countries have faced rising commodity prices without simultaneous capital inflows and nominal exchange rate appreciation, which has translated into higher domestic prices of consumer baskets.

J.P. Morgan has estimated an acceleration in global consumer prices to close to an annual rate of 5% in the third quarter of the year, negatively impacting household purchasing power and consumer goods spending, before moderating this quarter (Figure 2). Supply disruptions have been a major factor, particularly in advanced economies. However, scarcity of imported inputs has also impacted manufacturing activity in emerging market and developing economies: for example, Brazilian automakers halting production lines because of the lack of semiconductors.

It is essential to understand that the delays in delivery since 2020 have two aspects: supply and demand. On the supply side, complexity, density, and geographic distribution of value chains make final delivery highly vulnerable to blockages at any link.

On the demand side, there have been significant changes in composition and volume since 2020. The substitution of consumption of contact-intensive services by electronic home goods has led to an explosion in demand for semiconductors, for example. At the same time, particularly in advanced countries, fiscal support packages have enabled families to maintain their disposable income during the pandemic. This has happened to such an extent that in September, consumers in the U.S. were able to use accumulated savings to keep shopping at a pace above the increase in their personal incomes.

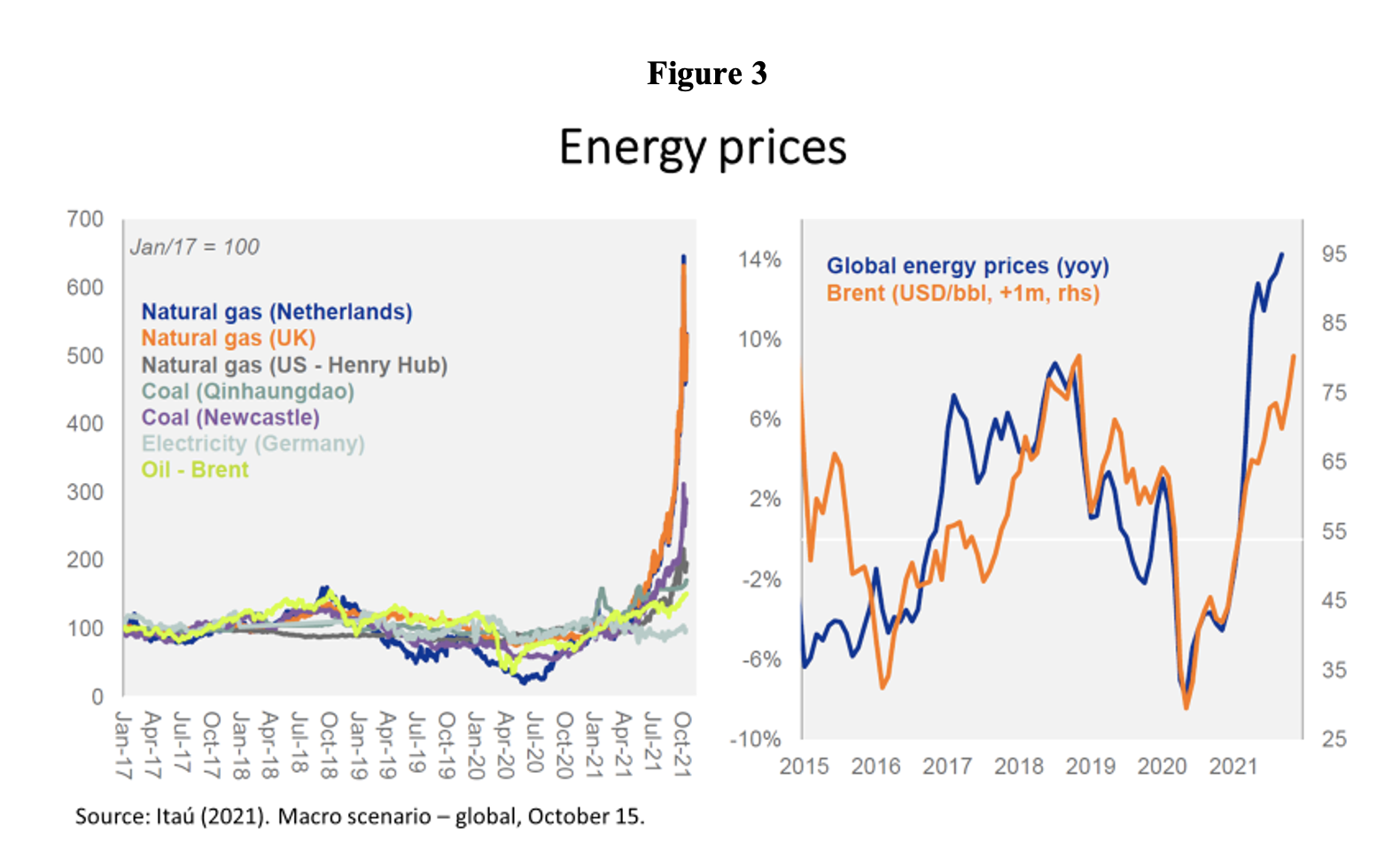

A mismatch between demand and supply can also be found in the energy price shocks (Figure 3), showing how the road to decarbonization will be bumpy. Low gas stocks in Europe, restrictions on the availability of coal in China and India, and capacity limits in the production of shale oil in the U.S. have all been faced while there is still an insufficient alternative supply of renewable energy.

In China, energy shortfalls have led to temporary stoppages in industrial production in some regions, aggravating the disruption of value chains, with global repercussions. It has become clearer than ever that there is a need to strengthen the provision of renewable energy to avoid tightness of supply relative to energy demand, and make the system less vulnerable to shocks arising from accidents and routine maintenance problems and, this year, low wind as in Europe, droughts that have put at risk hydroelectric production in Brazil, and floods in Asia hampering coal delivery.

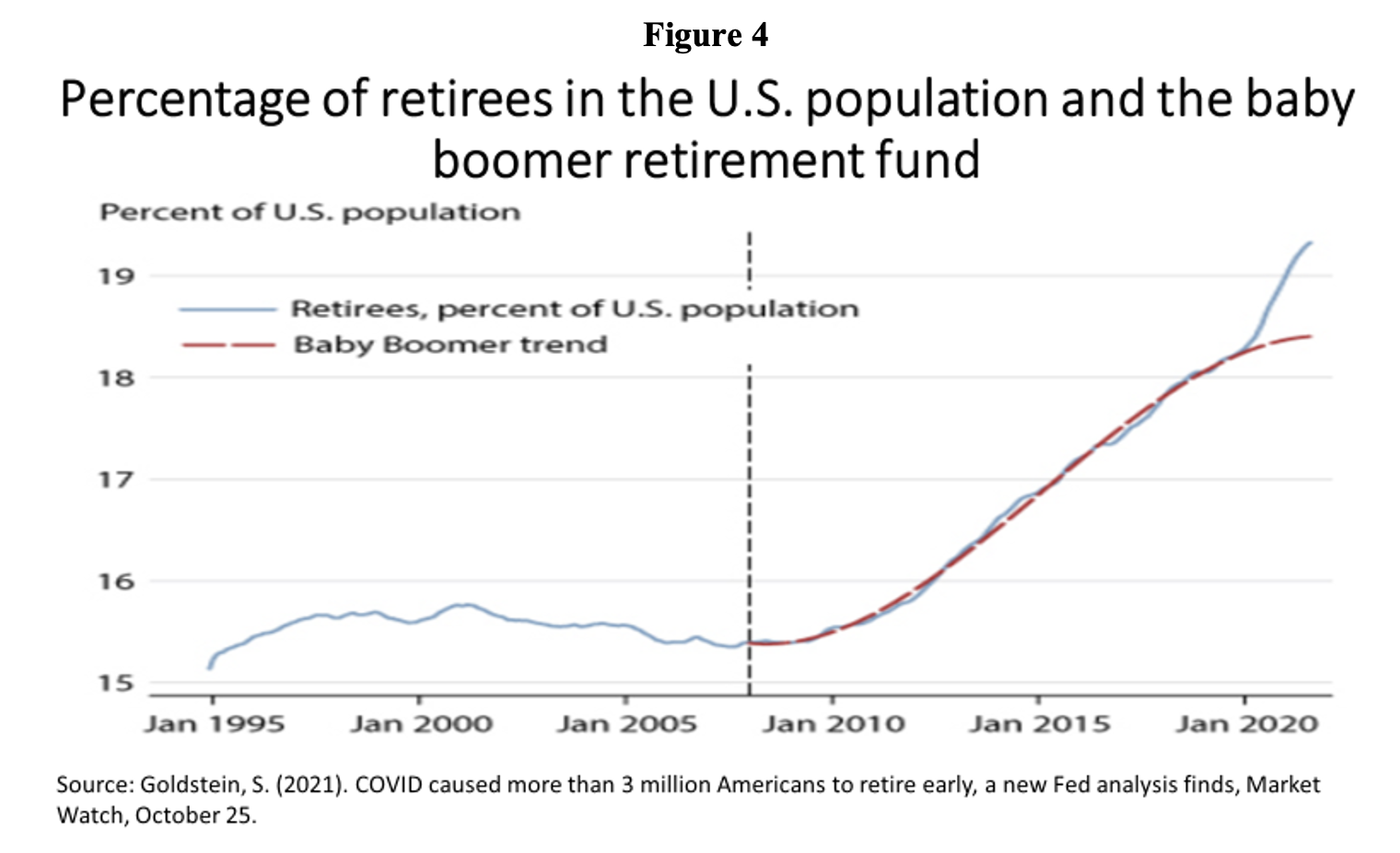

The running of supply chains in the U.S. has also been affected by an unexpected shrinkage in the workforce because of acceleration in retirements caused by the pandemic. According to Miguel Faria e Castro of the Federal Reserve Bank of St. Louis, more than half of the 5.25 million people who left the country's workforce, from the beginning of the pandemic until the second quarter of 2021, corresponded to more than 3 million excess retirements during COVID-19 (Figure 4). The author suggests two major reasons: greater health risks for older adults and/or because of enrichment resulting from the appreciation of financial assets that has reflected monetary policy during the pandemic.

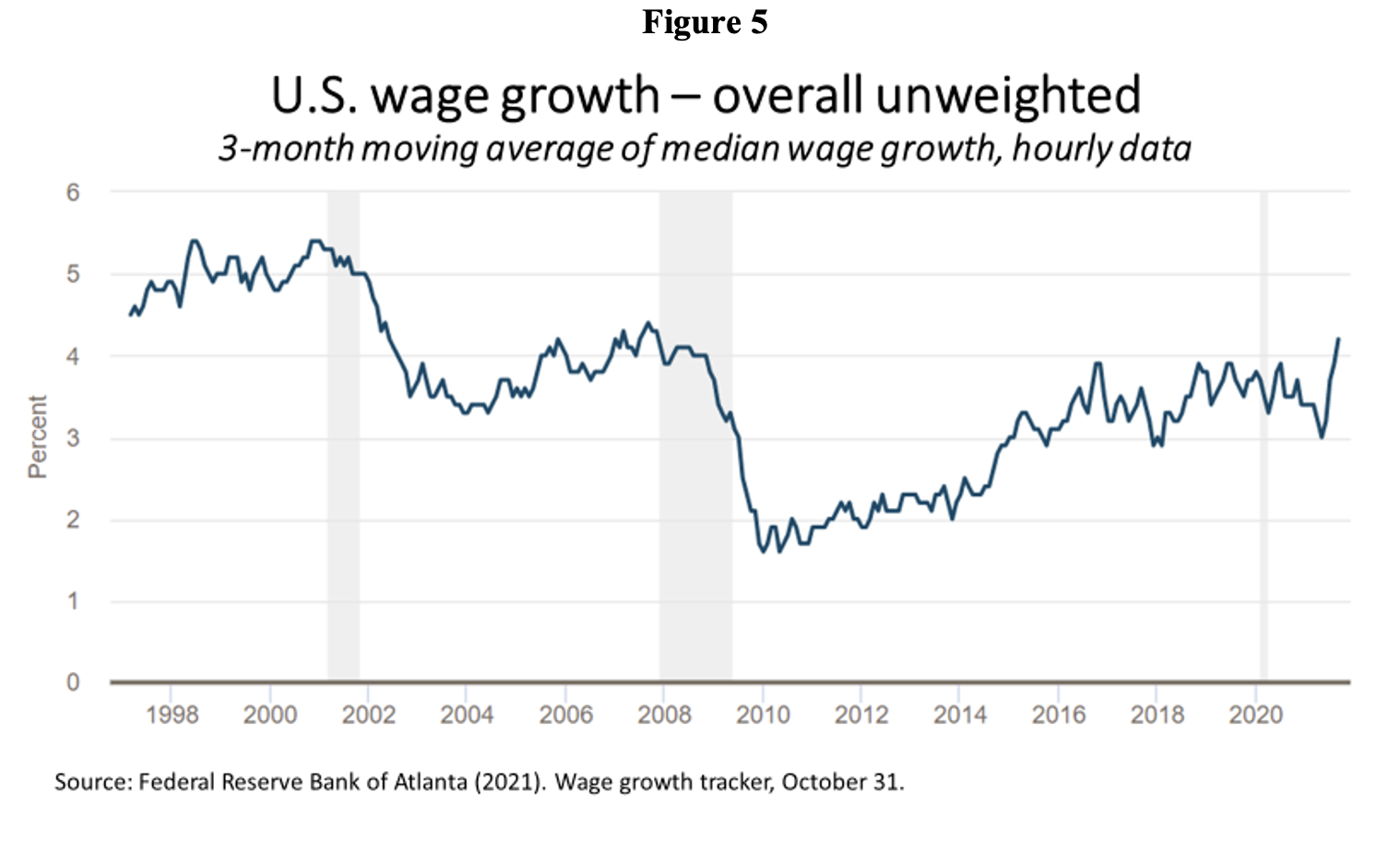

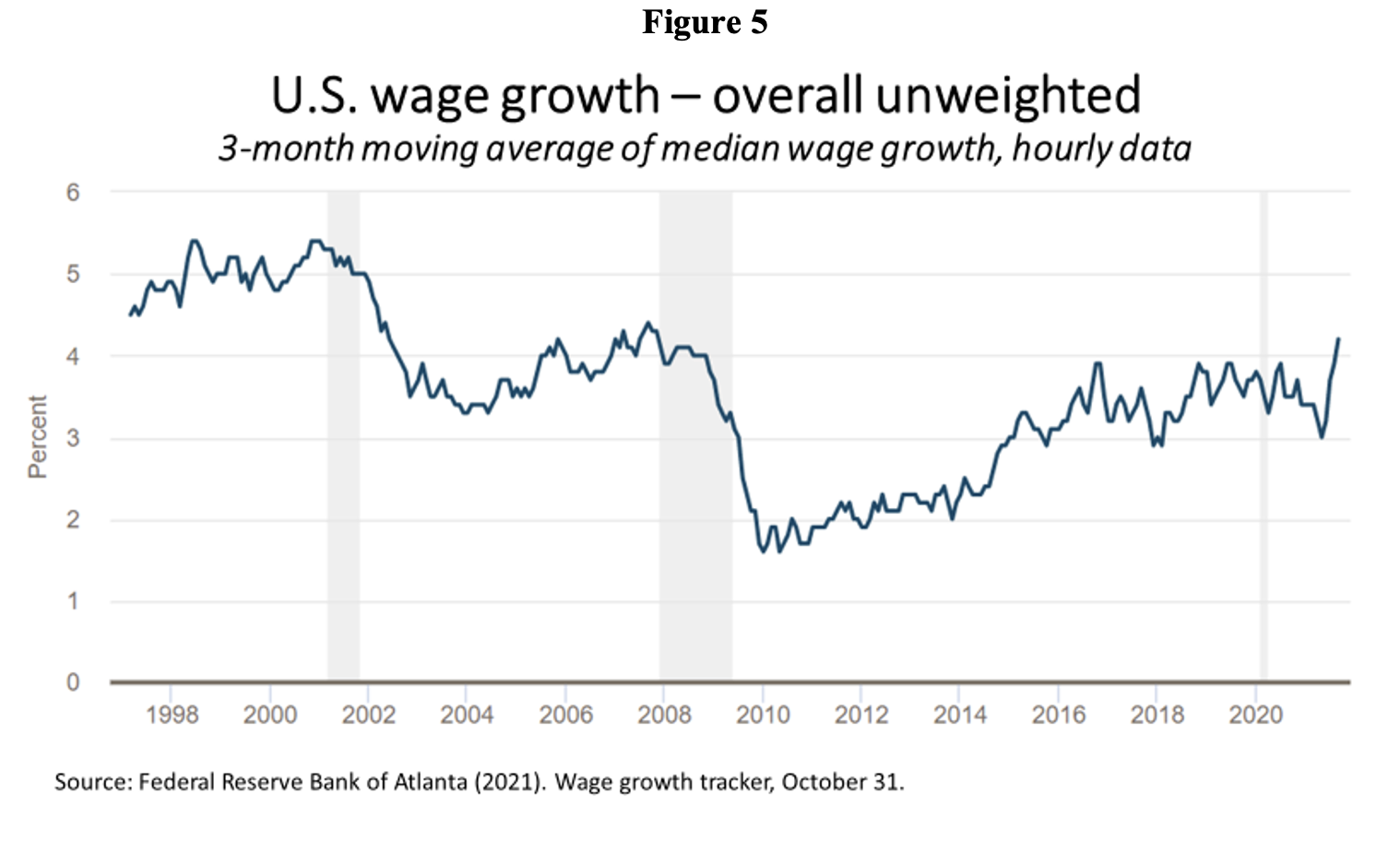

The pace of the U.S. economic recovery and attempted rebuilding of value chains as the economy has reopened has had to deal with with labor shortages, temporarily or not. The fact is that nominal wage increases have climbed (Figure 5).

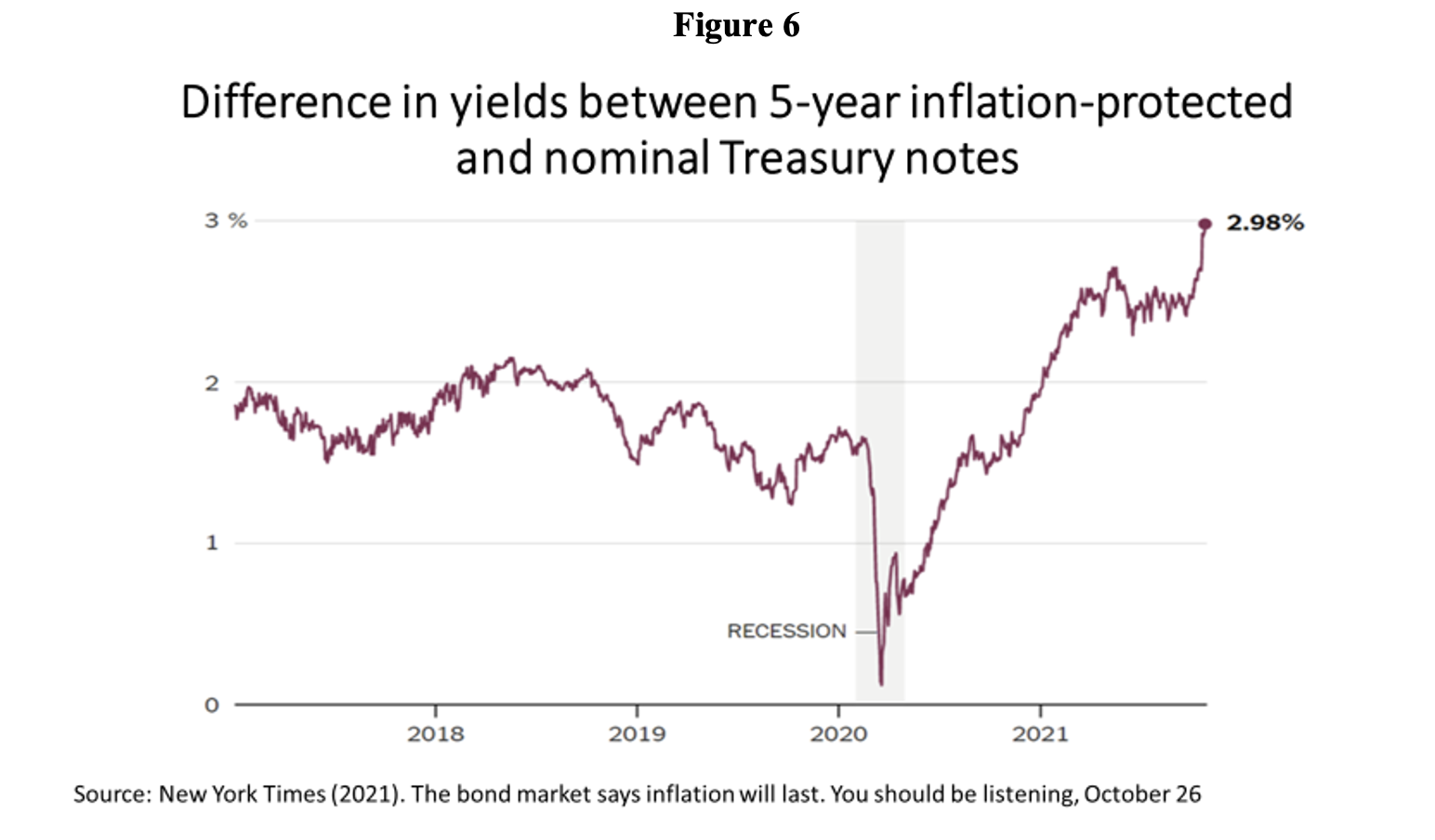

The inflationary scenario has started to change with the perspective that value chain disruptions and supply constraints will take some time to be fixed, taking at least until the first half of 2022. In the U.S., the difference in rates of return between nominal 5-year Treasury bonds and those protected against inflation in the same period, rose in recent weeks from levels of around 2.5% to close to 3% per year (Figure 6). While this partly reflects a greater perception of risks stemming from errors in inflation forecasts themselves, the fact is that it suggests that investors expect higher inflation to persist.

The ‘tug-of-war’ between hawks and doves over how the Fed should proceed with monetary policy will become more dramatic. Inflation is always a matter of mismatch between demand and supply, regardless of the origin of shocks. However, as Randal K. Quarles, one of the Fed's Board of Governors, expressed it at an event two weeks ago:

“The fundamental dilemma that we face at the Fed right now is this: Demand, augmented by unprecedented fiscal stimulus, has been outstripping a temporarily disrupted supply, leading to high inflation. But the fundamental productive capacity of our economy as it existed just before COVID—and, thus, the ability to satisfy that demand without inflation—remains largely as it was, and the factors that are disrupting it appear to be transitory. Looked at purely in that light, constraining demand now, to bring it into line with a transiently interrupted supply, would be premature. Given the lags with which monetary policy acts, we could easily find that demand is damping just as supply is increasing, leading us to undershoot our inflation target—and, in the worst case, we could depress the incentives for supply to return, leading to an extended period of sluggish activity and unnecessarily low employment. (…) I am among those who see a good chance that inflation will remain above 2% next year, but I am not quite ready to conclude that this ‘transitory’ period is already ‘too long.’ (…) Therefore, we will remain outcome based, waiting to see further improvements in employment and the evolution of inflation pressures in coming months.”

The Fed ‘soap-opera plot’, therefore, pits those who favor a ‘wait-and-see attitude’—moving on to the tapering this year and likely small rises at the end of next year—and those who think the Fed is already behind on the policy reorientation. I must confess to leaning in favor of giving more time to see if supply-chain constraints unwind, among other reasons, because inflation rates a bit higher than 2% a year in 2022 are in line with the Fed’s new average inflation targeting framework.

However, one must also keep in sight that some sort of financial adjustment is bound to happen as interest rates go up. As we approached earlier this year, the “U.S. big balance sheet economy” has been on a growth path highly dependent on the continuity of low real interest rates, as well as stretched price-earnings ratios of stocks and high corporate debt. Periodic episodes of downward adjustment of asset prices have been countervailed with lax monetary policies. And even if the gradual tightening as in the “wait-and-see” attitude shows to be the appropriate response, laxity of monetary policy as a way to avoid asset price adjustments looks to be temporarily exhausted at this time.

There is another polarized plot between those who attribute partial responsibility for value-chain disruptions to governments, and those who point to such disruptions precisely as an argument in favor of less globalization. But that will be the subject for another day.

The opinions expressed in this article belong to the author.