Publications /

Opinion

As the introductory textbook to economics by Nobel Prize Paul Samuelson, who served several generations of students, including mine, said: “It is easy to teach economics to a parrot. Two words are enough: supply and demand”. These two factors suggest 2023 will be a year of upward trend for most commodity prices.

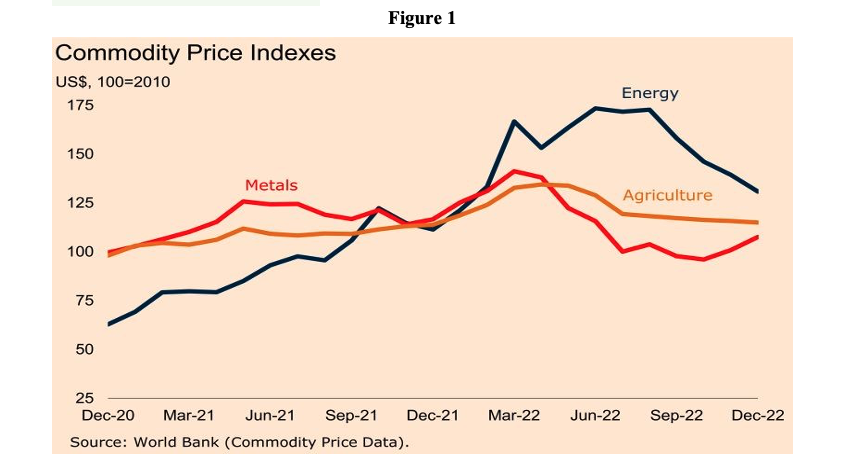

Last year was marked by shocks and volatility in commodity prices, with two distinct moments. After the sharp rise in the first half, due to the invasion of Ukraine by Russia, the rise in interest rates that led to a slowdown in demand, on a global scale, caused a sharp a drop in prices in the second half of the year (Figure 1).

In 2023, both the demand and supply sides point to upward pressure across much of commodity prices. On the demand side, the US, Europe, Japan, and other countries are on an economic slowdown, with recession or not. On the other hand, after the suspension of the "Covid zero" policy in China, the country's GDP should grow between 5.2%, according to the IMF World Economic Outlook update forecasts by analysts and multilateral institutions. This is after the 3% GDP increase last year. As central banks approach peaks in their hikes in basic interest rates, after which the latter will likely stay stable for a while, their effects in terms of volatility should recede.

On the supply side, low inventory levels and lack of investment in the recent past will restrict capacity on the supply side to respond. The limits of lack of supply are visible in almost all segments, with stocks at operating levels in a critical situation and/or production capacity used to the limit.

Analysts at Goldman Sachs suggested that commodities, as an asset class, are expected to outperform other asset classes this year. According to them, it will be the third consecutive year in which this happens. They project returns on the S&P GSCI Commodity Index of around 9.9% over three months, 17.3% over six months and 31.2% over one year.

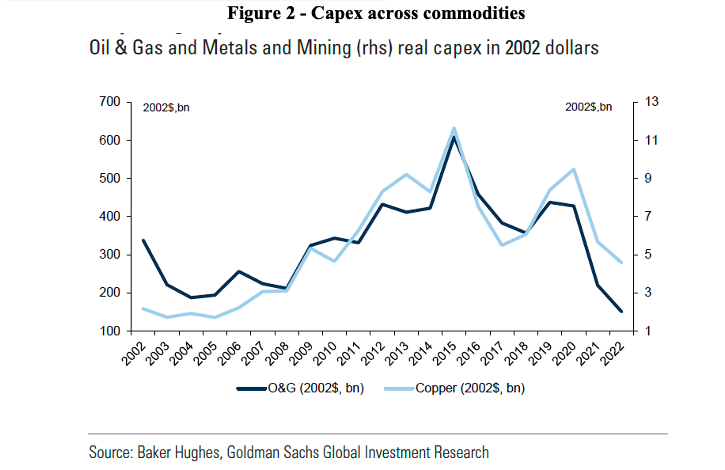

The global drop in investments in fixed capital, in real dollar amounts, in the copper and gas and oil sectors from 2015 onwards- particularly from 2020 onwards -, despite the rise in prices, is impressive (Figure 2). In the case of gas and oil, there is a reflection of their prospective drop in demand with the energy transition, while copper’s demand is increasing exponentially. Crude oil, refined petroleum products, LNG and soybeans are expected to be the main beneficiaries of rekindled Chinese demand, Goldman Sachs said.

In its recently released forecast report for commodities, the EIU (Economist Intelligence Unit) foresees oil and natural gas prices remaining elevated at levels close to or above current levels. OPEC production (including Russia) is expected to decline by around 3 million barrels/day from its recent peak in late 2022.

It is worth keeping an eye on, in 2023, how cohesive OPEC will remain in its commitment to reduce production quotas in the face of pressure from Western countries. The share of the oil market covered by OPEC has declined from 40% in mid-2016 to below 35% last year. Despite its agreed production cuts, idle production capacity remains limited.

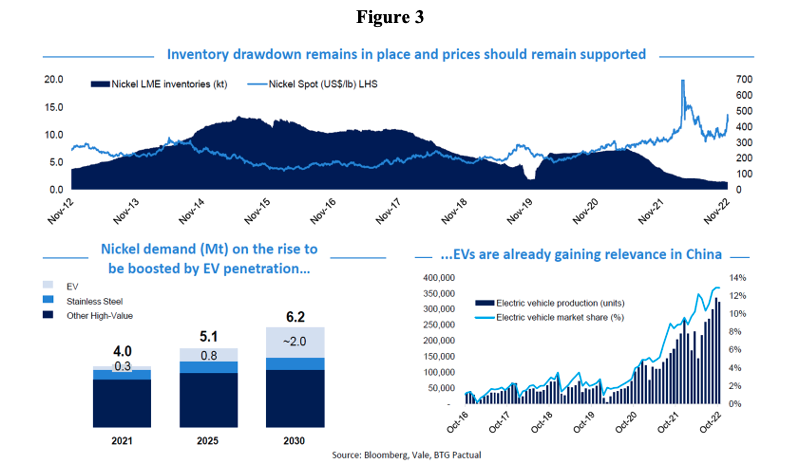

In the case of metals and minerals - copper, aluminum, iron ore and others - the trend is upward, benefiting from Chinese demand. Also in a recent report, BTG Pactual highlighted how low global aluminum inventories are. The production and export of Brazilian iron ore remains at levels far below its potential. In the case of nickel, whose demand tends to grow exponentially with the spread of electric cars, BTG Pactual shows how the use of these vehicles has expanded in China (Figure 3).

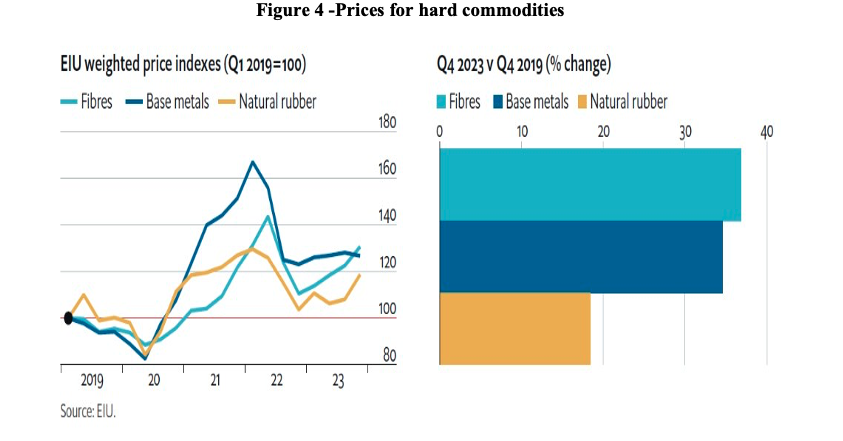

According to the EIU report, an increase in prices of “hard commodities” (fibers, base metals, natural rubber) is expected in 2023, recovering part of last year's decline (Figure 4).

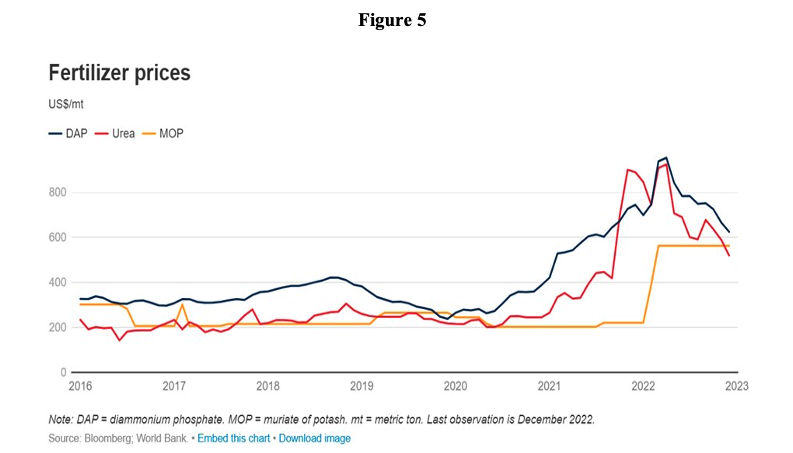

According to the World Bank's commodities team, fertilizer prices have declined from the peaks of early 2022, but remain at historically high levels (Figure 5). The drop in prices in the second half of last year partly reflected weakened demand as farmers reduced fertilizer applications due to access and availability issues. The fertilizer industry was also affected by supply-side issues, including the production crisis in Europe, disruptions due to sanctions on Russia and Belarus, and export restrictions in China.

Global food prices and corresponding commodities should remain high, as highlighted in a report by the International Monetary Fund (IMF) last month. Since December, agricultural, cereal and export prices have remained relatively stable. Corn and rice prices are 8% and 13% higher, respectively, than in January 2022, and wheat prices 2% lower. On the other hand, the ongoing war in Ukraine, energy costs and weather events are likely to keep them under pressure, despite the interest rate hikes since the second half of 2022 easing upward pressure.

As the parrot would say, the trajectory of supply and demand conditions in different segments of commodity markets indicate where their prices are going. Such conditions eventually overlap with the effects that interest rates and financial markets bring to them.

In this sense, evolution can be very different. To give you an idea, in 2022, while coal, lithium and nickel offered returns of 157%, 87% and 43% respectively, those who bet on magnesium and tin lost, respectively, 54% and 37% of their investment.

Not all commodity prices will necessarily move up. As far as energy, metals and minerals are concerned, the parrot is likely looking up at this point; definitely in this case the best thing to do is to mimic the parrot.