Publications /

Opinion

Greek Prime Minister Alexis Tsipras has already completed two notable labors. First, he led his radical left-wing Syriza party to an improbable election victory in January 2015. Then, also improbably, he won a resounding no vote in a referendum on July 5 on accepting the terms of Greece’s international creditors for a new bailout package.

According to Greek mythology, there are ten more labors to go, and indeed, it will probably take that many to redeem the Greek economy. Tsipras’s next labor already looms as he arrives in Brussels on July 7 for another round of negotiations with creditors.

Tsipras’s chances of success may be low, but they are higher than they would have been had the International Monetary Fund (IMF) not recently issued a preliminary revision to its debt sustainability analysis. That reassessment declared Greece effectively bankrupt and so in need not only of far-reaching reforms but also of debt forgiveness.

The IMF’s verdict, the people’s thumbs-down to more austerity, and Greece’s collapsing economy make for a Herculean task, but one that focuses the mind. Now, Tsipras knows that he is close to the endgame. Not only is the postreferendum euphoria likely to fade fast, but with banks closed and cash withdrawals limited to €60 ($66) a day, Athens and Thessaloniki may also be only days away from riots.

The creditors, for their part, know that the time has come when they must either let Greece exit the eurozone or swallow hard and provide new financing on terms that are a major improvement on those they offered before the referendum. At the same time, the European Central Bank, by downgrading the collateral it is willing to accept from Greek banks since the no vote, has shortened the fuse on potentially explosive negotiations.

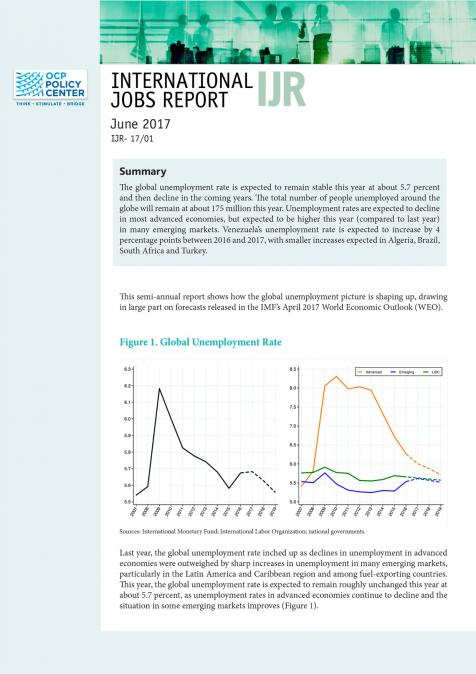

Meanwhile, Americans, who have done much better than eurozone members at deploying aggressive stimulus policies to revive growth, are watching the Greek crisis disapprovingly but with great interest. TV audiences are especially intrigued by a race to the finish line that has more stages than the Tour de France. Security analysts fret about the dangers of such deep rifts among their closest allies. However, economists have concluded that the spillover effects from the crisis on the United States are likely to be minimal—even though every twist alternately unnerves or elates Wall Street.

So, talks between Athens and its creditors must conclude soon. But no one knows how the complicated politics of the eighteen other eurozone members—each with vastly different perspectives—will unfold. Nor is it known whether a deal will be struck or what kind of deal it might be. What is clear, however, is that for any agreement to be workable, it must contain the following four essential elements. Call this plan A.

First, a deal must include budgetary measures and structural reforms, complete with timetables and review procedures, that demonstrate the Greek’s government serious intent on reforms. These reforms must aim both to reignite growth and to durably improve government finances.

Second, the creditors’ terms should comprise an equally strong commitment to debt relief. That is important given the IMF’s emphatic statement that even if Greece does everything right, the country will require €50 billion ($55 billion) of financing over the next three years and that, moreover, its debt load is not sustainable. The debt relief process must include a clear timetable and be explicitly conditioned on achieving budgetary and reform targets.

Third, there must be provisions to recapitalize the Greek banking system and provide ongoing emergency liquidity support over the duration of the program.

Fourth, a deal should include humanitarian support for the large segment of the Greek population that is currently incapable of acquiring basic necessities and for which the situation is about to get worse. Incidentally, should Germany choose to carry a disproportionately large share of this burden, it could win many friends in Greece.

If the parties cannot agree on these essential measures, either because of Tsipras’s reluctance to make the needed commitments or because of the creditors’ resistance to forgive debts and provide new money for Greece, then it is time for plan B.

Plan B, which some would argue is preferable to plan A, consists of Greece introducing a parallel currency that enables it to achieve a devaluation and—very probably—grow again on the basis of a much-expanded tradable sector. This course has merits as well as many risks; but plan B absolutely does not have to represent a litigious break from the eurozone.

Plan B could include some of the elements of plan A in a modified form, such as an orderly restructuring of Greek debts against a number of (almost certainly more lenient) reform and budgetary targets designed to make sure the devaluation succeeds. The scheme could involve temporary European Central Bank support to Greek banks as a progressive redenomination of Greek debits and credits is carried out.

Also as in plan A, plan B could include provisions for humanitarian aid during the difficult transition period to a new currency. The creditors could hold open the possibility—undoubtedly far in the future—that Greece might return to health, phase out its parallel currency, and avail itself of all the facilities available under the European System of Central Banks.

Regrettably, Greece’s relations with its eurozone creditors have been increasingly cast as a zero-sum game—or, worse, in Manichaean terms of good versus evil. The reality is that both Greece and its creditors have an overwhelming joint interest in a viable Greek economy within the European Union. Those joint interests would remain even if Greece were to adopt a parallel currency.

The euro, after all, is not a religion. It is certainly not intended as a cult that burns sinners at the stake. The euro is a monetary arrangement, and a very imperfect one at that.

This article was published by Carnegie Endowment for International Peace.