Publications /

Opinion

The February 20 United States Supreme Court decision against President Donald Trump’s use of the U.S. International Emergency Economic Powers Act (IEEPA) to establish tariffs has led him to resort to other legal instruments. So-called U.S. reciprocal tariffs on countries set out in April 2025 were based on IEEPA, as were tariffs that allegedly punished countries for allowing fentanyl into the U.S. Trump tried to evade the constraints presented by other legal instruments that could facilitate tariffs, but is now forced to resort to them if he wants to rebuild the tariff wall he raised in 2025.

Among the alternatives to IEEPA, Trump immediately resorted to Section 122 of the 1974 Trade Act, which authorizes the use of temporary import surcharges (up to 15%) or quotas for up to 150 days, in order to deal with significant balance-of-payments deficits. The Trade Act was passed at a peculiar time, when the international monetary system was abandoning the fixed exchange-rate regime established at Bretton Woods. It has never been used to impose broad and lasting trade barriers.

In contrast to the reciprocal tariffs, however, Section 122 allows only a universal tariff. Furthermore, it needs to be validated by Congress before the 150-day limit expires.

Shortly after the Supreme Court ruling, Trump announced a 15% surcharge but subsequently reduced this to 10%. A 15% rate would have immediately conflicted with bilateral agreements made with the United Kingdom, the European Union, Japan, and others. Announcements by these countries that they would suspend the confirmation of such agreements certainly weighed on Trump’s decision to stick with a 10% duty.

But more may follow. Trump has already said that he will also deploy Section 301 of the Trade Act, which authorizes the adoption of tariffs as compensation for ‘unfair’ trade practices by other countries, after investigations. Another provision that could be triggered is Section 232 of the 1962 U.S. Trade Expansion Act, which refers to reasons of ‘national security’ trade restrictions. Not to mention the Smoot-Hawley Act of 1930.

The reason Trump relied on IEEPA in April 2025—ultimately unsuccessfully, given the Supreme Court’s decision—was that these alternatives did not facilitate differentiation between countries targeted by tariffs. They also require processes that are anything but automatic and do not eliminate Congress’s role. However, Trump’s references to them in the wake of the court decision corroborated his announcement that he had not abandoned the direction of his trade policy. It is also worth remembering that sectoral U.S. tariffs—steel, aluminum, and automobiles—remain in effect.

Uncertain Impacts

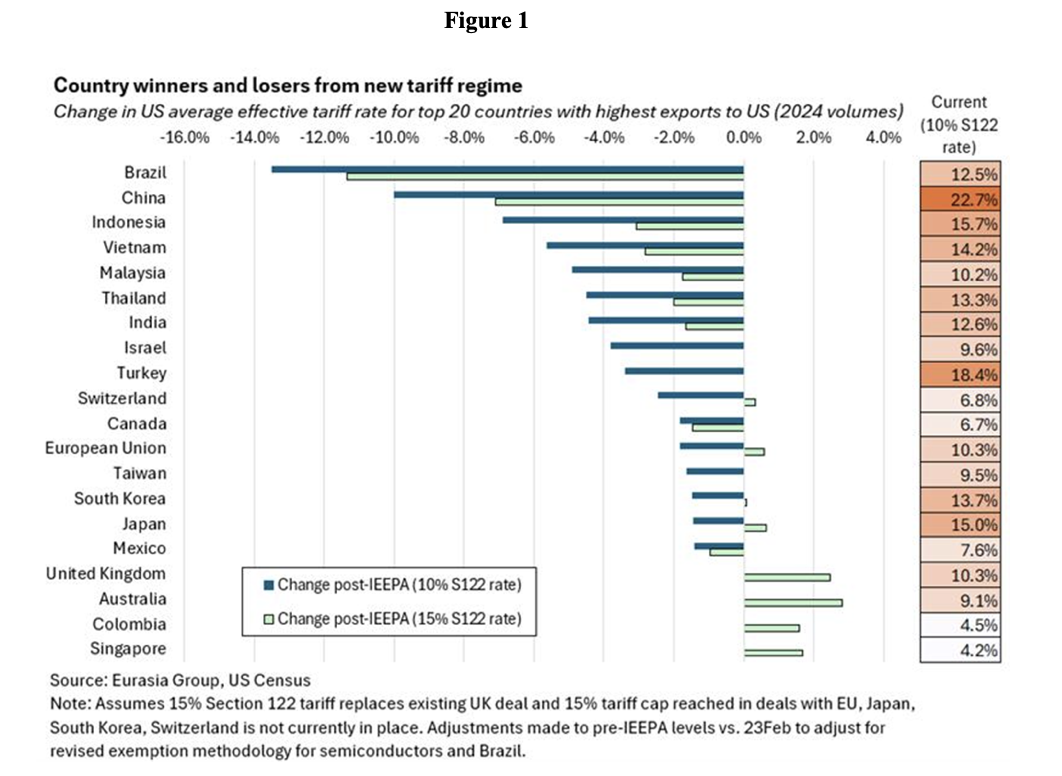

Regardless of the new tariff structure, the countries affected most directly by the IEEPA tariffs have been given some relief, at least in relative terms. This is the case for Brazil, India, China, Canada, and Mexico, and for Southeast Asian countries that were previously facing rates of 19%-20%. Figure 1 (from a February 24 Eurasia Group report, New 10% tariff eases fears around US trade deal breaches, for now) illustrates how the unwinding of IEEPA tariffs will impact U.S. trade partners differently.

Recall that extraordinary tariffs on Brazil—with references to former president Jair Bolsonaro’s trial and Brazilian Supreme Federal Court decisions—were applied under IEEPA, as were Trump’s punishments directed at India for buying Russian oil, and China for fentanyl.

Brazilian enthusiasm at the nixing of these tariffs must be tempered, however, by the fact that an investigation into Brazil under Section 301 is already underway. This is also the case for China. In July 2025, an investigation started into policies and practices that allegedly harm U.S. companies, including Brazil’s public electronic-payment tool (Pix), some trade tariffs, the exercise of intellectual property, and illegal deforestation. The result could be used as an excuse for new tariffs on Brazil. Similar processes will have to be implemented with the other countries if Sections 301 and 122 are to replace IEEPA.

It is also likely that questions will arise about the legality of the new overall Section 122 tariff. Litigation will probably focus on the issue whether the U.S. president has authority to declare a balance-of-payments emergency. This is not simple: what constitutes a situation that would justify such an assertion? Should services—in which the U.S. has a surplus—be accounted for together with the trade deficit in goods?

The issue will not be resolved before the end of the current 150-day Section 122 validity period, but, judging by what happened with IEEPA, the courts will not block its use until any finalverdict from the Supreme Court If the White House uses Section 122 as a bridge while conducting country-specific investigations under Section 301, the complexity and uncertainty associated with Trump’s tariffs will remain extremely high.

In any case, Trump’s promise to restructure tariffs using, for example, Section 301 will inevitably be a complex and laborious process, with the need for new case-by-case investigations, in addition to those already underway. There is no way to easily fulfill Trump’s promise to rebuild the tariff wall as it was.

Other Implications

The Supreme Court’s decision on the IEEPA tariffs also has implications far beyond the reconfiguration of Trump’s tax wall. As Marcus Vinícius de Freitas has so aptly pointed out in an article published in Brazil:

“The recent decision by the United States Supreme Court requiring Donald Trump to continue operating strictly within the existing legal framework for imposing trade tariffs goes far beyond a technical episode of constitutional law. It offers an almost pedagogical reading on the functioning of the American institutional system, and on the real limits of presidential power, even when exercised in an assertive, personalistic, and confrontational manner.”

There is also the issue of the return of taxes collected as IEEPA tariffs. Estimates suggest that of the $264 billion collected as tariff revenue by the U.S. last year, $130 billion derived from the now-retrospectively canceled IEEPA tariffs. But some estimates put the number as high as $175 billion.

Trump always said that exporters to the U.S. would pay the tariffs. In economic terms, this has proven largely wrong, as the cost of the tariffs has been passed on to domestic producers and consumers. A study by the Federal Reserve Bank of New York that showed the extent to which this has happened even earned a reprimand from Kevin Hassett, one of Trump’s advisors.

The U.S. has the peculiarity of allowing foreign companies to act directly as registered importers, known as ‘importers of record’. In the Financial Times on February 26, Alan Beattie quoted the global logistics technology company Flexport as saying that its analysis of customs data suggests that Chinese importers of record accounted for 9% of trade with China before Trump hiked tariffs in April 2025, but this rose to 20% by the end of 2025.

This also means that the U.S. administration, while causing consumers to bear a loss, will disburse billions of dollars to several Chinese companies that have aggressively targeted the U.S. market. Think about that from the perspective of domestic tariff and taxpayers...

The IEEPA tariff journey has not ended well. The tariffs under IEEPA ended up being an illegal tax based on flawed economic principles, reluctantly revoked under belated legal pressure, and with the consequence that those who were said to be the object of ‘punishment’ will be compensated. The insistence on seeking punishment through other legal means risks extending the fiasco, while keeping uncertainty high.