Publications /

Opinion

On July 15, Turkey’s tumultuous 2016 took a shocking twist as elements within the country’s military attempted a coup against the government of President Recep Tayyip Erdogan. The putsch rapidly snapped at the seams, and a night that began with soldiers blocking bridges yielded a morning with those same soldiers flogged by civilians in the street.

In the days following the attempt, Erdogan declared a three-month state of emergency and began purges of depth and breadth that extended beyond public ministries and into the private sector. Thus far, analysts have primarily focused on the political and social implications, and for good reason. Until recently, Turkey had been hailed as a model country in a neighborhood of profound instability. Now, many question the extent to which Erdogan will consolidate power, and what implications this could have for Turkish democracy and for broader regional geopolitics.

But in the coming months, Turkey’s economic resilience could play an equally important factor in determining the outcome of the current upheaval. And, while Erdogan is now portrayed as a conservative strongman, his stewardship of the economy is critical to understanding his popularity. Should Turkey’s economy falter, his domestic support could dissipate as well.

Despite Erdogan’s influence in shaping Turkey’s recent economic rise, the country faces specific challenges that threaten to complicate matters in the months ahead.

The Erdogan Economy

To a degree, Erdogan’s popularity stems from his efforts to create a space for religion in Turkey’s public sphere. It is a popular - and populist - approach. Poorer Turks throughout broader Anatolia (as opposed to the more cosmopolitan cities of Istanbul and Izmir in western Turkey) have historically been more religious and chafe at the perceived elitist secularism that has prevailed in the country since the days of Kemal Ataturk, the founder of modern Turkey, and they have rallied around Erdogan’s conservative populism.

But this is not Erdogan’s only appeal. He has also proved to be a steward of the Turkish economy, and this has earned him significant support from small and mid-sized businessmen who recall the chaos of the late 1990s - characterized by violent swings in GDP and annual inflation that routinely topped 80 percent. Political and economic turmoil hit a crescendo in 2001, when capital flight sparked a banking and financial crisis. Over the course of that year, “GDP contracted by 7.4 percent in real terms, wholesale price inflation soared to 61.6 percent, and the currency lost 51 percent of its value against the major foreign monies.”

Erdogan first assumed power in the wake of this meltdown. His Justice and Development Party (AKP) party won two-thirds of seats in parliament in 2002, and Erdogan himself became prime minister in 2003 - a year in which inflation still topped 25 percent. In subsequent years, he entrenched a stabilization effort (spearheaded earlier by former economy minister Kemal Dervis), implementing reforms consistent with International Monetary Fund and European Union (EU) recommendations that once again made Turkey an attractive destination for foreign direct investment. Inflation dropped to 8.5 percent in 2004, and it has hovered in that range since.

Improved macroeconomic conditions combined with a friendly disposition toward international business and investment created a favorable atmosphere for growth, which averaged 6.9 percent annually from 2003 to 2007. This was high-quality, sustainable growth predicated on investment, multifactor productivity enhancements, and competition. In particular, Turkey’s “Anatolian Tigers” - industrial firms from conservative heartland cities like Konya and Kayseri - emerged as globally competitive forces. All told, Turkish exports increased from US$22.47 billion in 2000 to US$106.93 billion in 2014.

Although the Turkish economy continued to grow after an initial dip during the global financial crisis of 2008-09, the quality of this growth has not matched that of the initial Erdogan years. Rather than reaping the benefits of productivity gains, increased consumption and credit have buttressed recent growth, including government-led construction projects that could precipitate budget deficits, benefit firms with ties to the government, and may not even be necessary in the first place. The shift has somewhat muted the Anatolian Tigers’ roar: From 2003 to 2008, exports to the EU increased over 300 percent. Since then, they have increased just 7 percent, though the EU’s own economic slump certainly plays a role in this deceleration as well.

Erdogan would do well to return to his initial economic approach, but challenges on the horizon may make this difficult.

Video: Talking Turkish Economics- Samuel George with Dr. Daron Acemoglu

Frontier Challenges: Short- to Long-Term Threats to Turkey’s Rise Tourism Declines amid Security Risks

The most immediate threat to Turkey’s economy is a dramatic drop in tourism receipts. With tremendous cultural, historical and geographic diversity, Turkey has become a hot-spot for international vacationers. In 2015, nearly 40 million tourists visited Turkey - the globe’s sixth highest arrivals total - injecting roughly US$30 billion into the country’s economy. Including tourism’s indirect effect, the sector contributes about 12 percent of the country’s total GDP.

Even before the July coup attempt, the tourism sector had been rocked by terrorism, civil strife and diplomatic fallouts. Over the last six months, Turkey has increasingly become a target for the Islamic State group, which specifically targets locations popular with international tourists. Conflict with Kurdish separatists has led to deadly attacks in major cities, military crackdowns, and controls on movement in the country’s southeast. The latter has been particularly deleterious for cities and towns that had been gaining in popularity as off-the-beaten-path tourist destinations. For example, Diyarbakir, the region’s capital, had made a sustained effort to revamp tourist infrastructure; now even U.S. government officials face travel restrictions to the city. Even towns in the region that have not been involved in conflict such as Mardin, an ancient jewel of a village, face sharply declining tourism receipts given travelers’ overall aversion to the region.

Shaky relations between Ankara and Moscow have also punished the industry. Previously, Russians constituted one of the largest groups of tourists in Turkey, but travel restrictions imposed by the Kremlin in late 2015 led to a precipitous decline. These restrictions have since been lifted, but it remains to be seen if Russian vacationers will return in full force.

All told, Turkish tourism receipts fell 36 percent year on year in the second quarter of 2016, and this does not take into account cancellations and tepid demand as the country enters a period of “national emergency.” Should Turkey stabilize its security situation, this dip could be but a short-term shock as the downturn does not reflect deeper structural flaws in sector. But that is a big “if,” and, for the moment, Turkey’s reputation as a top vacation destination has certainly taken a hit.

Leery of the Lira: Macroeconomic Turbulence Ahead?

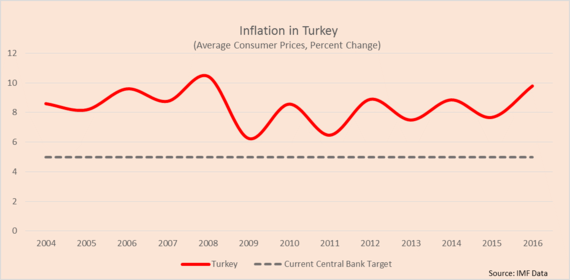

The macroeconomic discipline that supported Turkey’s strong economy may be fraying at the edges. For example, eager to prop up growth, Erdogan spearheaded a 30 percent increase in the minimum wage in late 2015. While economists expect a subsequent short-term boost on consumption , the wage hike will continue to put pressure on an already struggling lira. To be sure, inflation has decreased from the crisis years of the late 1990s, but it has hovered stubbornly between 8 and 10 percent, well above the central bank’s target rate of 5 percent.

Turbulence in emerging market exchange rates adds to Turkey’s currency vulnerability. As markets anticipate a stronger U.S. dollar, emerging market currencies from the South African rand to the Colombian peso have depreciated. Turkey’s lira is no exception, having fallen nearly 50 percent against the dollar in the last two years. This can be particularly painful for corporations with foreign-denominated debt.

The Central Bank of Turkey has maintained reasonably high interest rates in order to defend a fluctuating currency, but Erdogan has made it clear that he views tight monetary policy as a drag on growth. Murat Cetinkaya, central bank chairman since April, has since overseen multiple cuts to the overnight lending rate in what could reflect the politicization of the central bank. This trend deserves careful attention in the aftermath of the July coup attempt, given that Erdogan may be positioned to exercise more influence than ever before - and may feel the pressure to ramp up growth. While the bank has thus far been spared from post-coup purges, the Ministry of Finance has not - 1,500 of its officials have been suspended.

To be fair, not all global trends augur poorly for Turkey. U.S. Federal Reserve tapering appears slower than many expected, and oil prices remain low - two factors that ease Turkish macroeconomic tension. But pressure could intensify should foreign investors become skittish. Turkey routinely runs a current accounts deficit, though this has actually tightened in recent years, and is not particularly onerous to begin with (see chart to the right). It finances these deficits with short-term loans and portfolio investments. If this hot money cools off, it would accelerate the lira’s depreciation, stoking inflation.

Keeping it Real: Challenges in Trade

Erdogan’s initial economic success stemmed from an expanding real economy facilitated by improved diplomatic relations around the globe. For example, the country’s growing trade with the EU coincided with intensified dialogue regarding Turkey’s accession to that body. Both sides have since taken steps that make any such advancement highly unlikely. According to a recent study by the Bertelsmann Stiftung , this could have negative economic consequences, especially as the EU pursues other trade agreements, such as the Transatlantic Trade and Investment Partnership (TTIP), which would not include Turkey. Should the EU and United States agree on TTIP without any changes to the EU-Turkey customs union, the automotive and mechanical sectors could contract 10 percent and 4 percent in trade volume, respectively.

While Turkish trade relations with traditional partners in the EU face complications, opportunities with newer partners are no sure bet either. Turkey exports about 7.5 percent of its goods (in dollar value) to Syria and Iraq - two countries whose economies will likely remain in turmoil for the foreseeable future. Syria, in particular, stands out as a disappointment. In the years leading up to the Syrian civil war, Turkey sought to deepen economic ties with its neighbor to the south, viewing Syria as a “gateway to the Arab world for Turkish goods” as a 2009 Brookings Institution article put it. The statistics support the narrative: in 2006 Turkey exported US$573 million worth of goods to Syria. By 2010, that figure increased to US$1.85 billion. However, since the outbreak of Syria’s civil war in 2011, that figure has dropped to an annual average of about US$1 billion.

Finally, diverging geopolitical goals threaten Turkish trade relations with Russia, a country that receives about 4 percent of Turkish exports. Russian President Vladimir Putin actively backs his Syrian counterpart Bashar al-Assad. Erdogan, for his part, has supported Assad’s removal. The situation came to a head in November 2015 when Turkey downed a Russian jet that had entered its airspace, leading to Moscow’s enforcement of economic sanctions against Turkey. Ankara has since taken steps to improve relations both with Moscow and Damascus, but given the tenuous geopolitical situation, further disruptions to trade are not out of the question.

An Economy at the Crossroads

All things considered, Turkey’s economy is not at a breaking point. Annual growth between 3 and 4 percent may underwhelm, but emerging market GDP expansion is down across the globe: Mexico, Brazil and South Africa would be very pleased with Turkey’s growth projections. Budget and current account deficits persist, but they are manageable. Moreover, Turkey has demonstrated the capacity to compete in Europe with quality manufactured goods, and it has an industrial belt that could protect it from the vicissitudes of commodity prices.

Yet Turkey’s economy is at a crossroads, and how the country emerges from the current period of political crisis could dictate its ability to meet its challenges. Will power consolidation and purges render a compromised central bank? Will truculence with major partners such as the EU and Russia lead to deceleration in real-sector growth? Will human rights abuses and risk aversion lead investors to steer clear of Istanbul? And how will a population on edge react to what many expect to be a miserable summer in tourism receipts?

The answers to these questions could have more of an impact on Erdogan’s longevity, and on Turkey’s stability, than the half-baked putsch attempt of July 15.