Publications /

Policy Brief

The arrest of Venezuelan President Nicolàs Maduro caused international astonishment, raising questions about respect for international law. And, quite logically, the operation led to numerous analyses, both of the political, security and geostrategic arguments put forward by Washington, and of the underlying ambitions behind this decision, which has no real precedent in recent history. In addition to the fight against narco-trafficking, it was of course the oil issue that came first, noting the country's supposedly considerable reserves. However, there is little doubt that it will be extraordinarily difficult to return to the record production levels of past decades.

Questions were also raised about the reality of Venezuela's mineral resources and mining reserves, in order to meet the United States' ambitions to secure strategic metals. But with coltan, bauxite and aluminium, the potential of Venezuela remains equally hypothetical. One thing is certain, however: from Venezuela to Ukraine, via Greenland and the Democratic Republic of Congo, American power is accompanied not only by the famous "Monroe Doctrine", but also by a "raw materials doctrine", an essential part of an expansionist strategy reminiscent of the theory of "spheres of influence". Fossil fuels are at least as important as strategic mineral resources, where economic determinants may be secondary, and where preemption by levers other than commercial action is no longer ruled out.

US President Donald Trump's assertion that the United States would "recover" Venezuela's stolen oil clearly confirms the centrality of hydrocarbons to his power strategy. However, many questions remain about the economic relevance of such an approach and, more generally, about the underlying motives behind it. Increased control over the supply of hydrocarbons, revenge for a history that saw American oil companies "driven out" after waves of nationalization in what was once one of their Eldorados, the first step towards conquering the Venezuelan subsoil and its strategic mineral resources, the strangulation of Cuba, the blow dealt to China's great rival and a piece of a complex geostrategic puzzle where the return of "spheres of influence" seems obvious: the answers, in the form of conjectures, are multiple and largely interdependent.

THE UNCERTAIN COMMERCIAL POTENTIAL OF THE VENEZUELAN OIL SECTOR

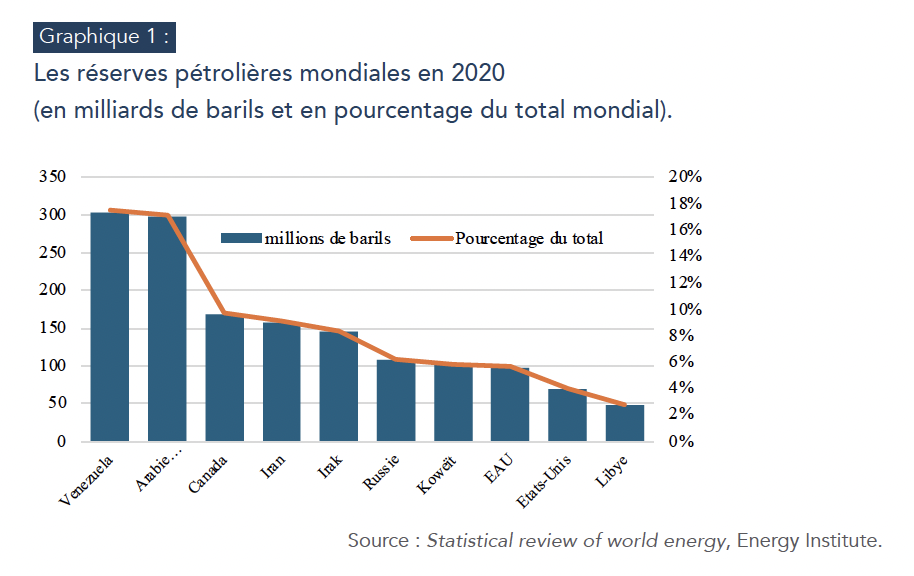

The size of Venezuela's oil reserves is certainly one of the most frequently cited reasons for Washington's offensive. According to 2020 data from the Organization of Petroleum Exporting Countries (OPEC), compiled by the Energy Institute, Venezuela's reserves are the largest in the world, thanks to the Orinoco oil belt. Estimated at 300 billion barrels, these reserves would represent 17% of the world's proven reserves1 and, under implicit American control, would give the United States access to over 20% of the world's oil.

Venezuelan gas reserves represent a "potential" share of global supply (graph 1). Venezuelan gas reserves are comparatively much smaller: estimated at 6.3 billion cubic meters (m3), they represent "only" 3.3% of the world total, well behind those of Russia and Iran, leaders in this field with 19.9% and 17.1% of proven reserves respectively, by the end of 2020.

Like many OPEC statistics, Venezuelan oil reserves are declarative. According to many experts, they are therefore probably overestimated, due to the very notion of "proven reserves" and, consequently, to the very particular nature of Venezuelan oil. Reassessed by Hugo Chavez's government without any independent audit, they soared in the two-thousand years even though no major discoveries had been made. They rose from 80 billion barrels in 2005 to 211 billion in 2009, then to 297 billion the following year, a level at which they have more or less remained. In 2011, the average price of Brent crude was around 111 USD per barrel (bbl), leading the Venezuelan government to classify the Orinoco reserves as proven reserves, i.e. exploitable despite the industrial complexity of extracting and refining them. With

"Merey 16" Venezuelan oil is a "heavy" or "extra-heavy "2 type, highly viscous and rich in sulfur3 . As a result, it requires large quantities of diluents to be extracted and special refining, making it much more expensive to process than light oil. Its profitability is therefore intrinsically dependent on high prices. However, these have fallen back since the record highs of 2011 and 2012, without reserves being revised downwards.

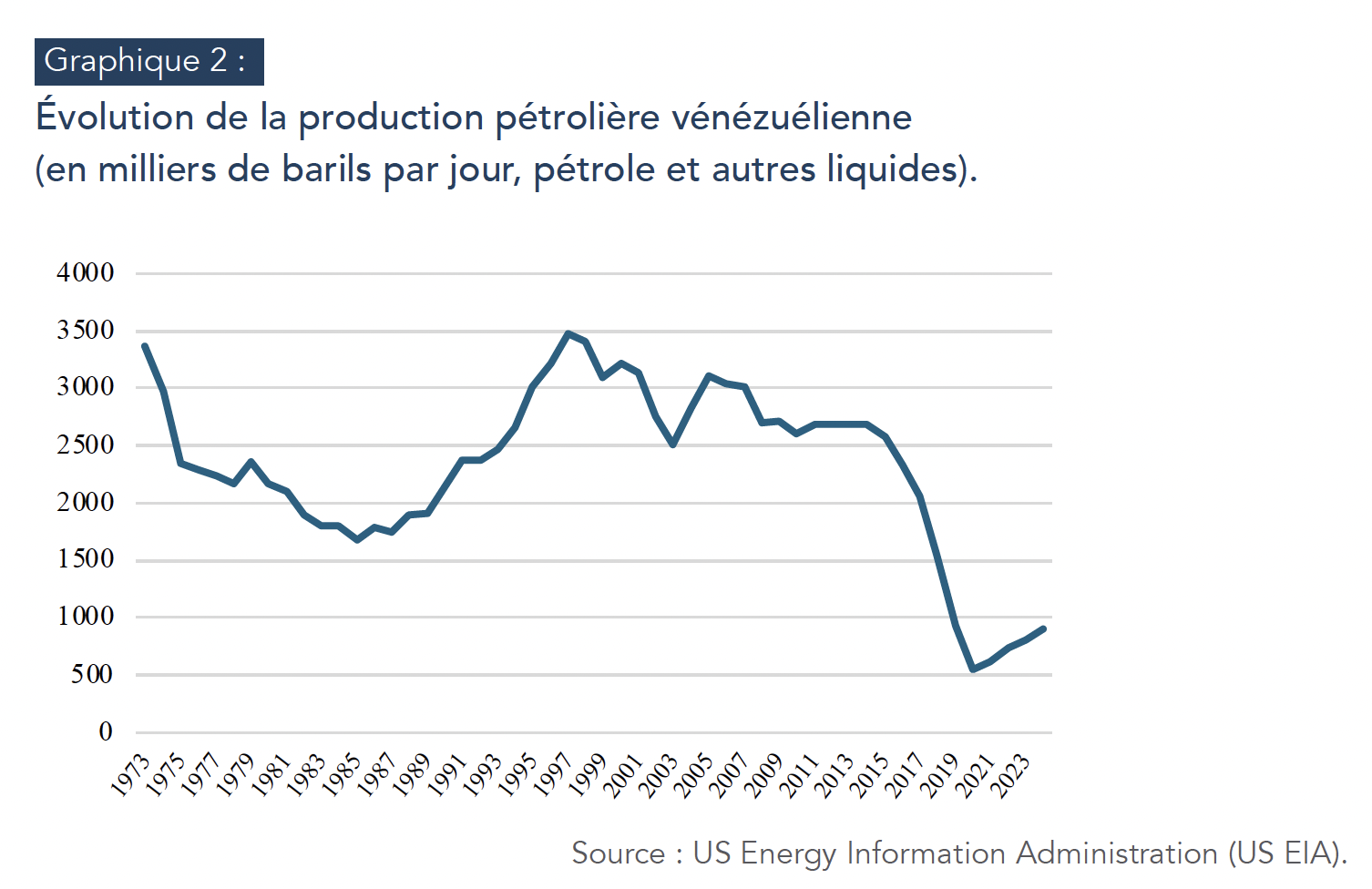

Moreover, Venezuela's oil-rich subsoil has not translated into high production levels over the past decade. After reaching a record of 3.75 million barrels per day (Mb/d) in 19704 and returning to the 3.5 Mb/d mark in 1996 and 2004/2005, the country's supply reached a low point in 2021 at 665,000 barrels per day, before recovering slightly to 960,000 barrels per day, representing barely 1% of world crude oil (compared with around 7% in 1970). There are several reasons for this. The second wave of nationalization initiated in 2001 by Hugo Chavez5 led to a simultaneous withdrawal of international oil companies, poor management and under-investment in logistical and production infrastructures, which require a high level of maintenance given the corrosive nature of heavy and extra-heavy oil, as well as a loss of local expertise. This was accentuated in 2006/2007 with the nationalization of the Orinoco projects in the south-east of the country, where ExxonMobil, ConocoPhillips, Chevron and Total were also positioned. From 2017 onwards, the imposition of US sanctions will reinforce this decline (graph 2).

A RETURN TO AMERICAN IMPORTS.

While a recovery in Venezuelan production seems possible, a return to historic levels is proving particularly difficult, given the colossal investments required to achieve this, the reluctance of the US majors to do so, and the current low crude oil prices. As a reference, Rystad Energy estimates that USD 53 billion would be needed to sustain Venezuelan supply at around 1.1 Mb/d. Reaching a production level of 3 Mb/d by 2040 would require investments of around USD 183 billion over the next 14 years, as well as more remunerative prices than today. However, according to the specialized agency, 200,000 to 300,000 barrels per day could be recovered over the next two years. In a context of oversupply and relatively low prices, Venezuelan supply counts for little, and this reality explains why crude oil markets reacted only slightly to the US administration's announcement that between thirty and fifty million Venezuelan barrels would be sold at market prices. Falling below the USD 50/bbl threshold, the sharper decline in Western Canadian Select (WCS) was explained by the increased competition between Canadian and Venezuelan oils on US soil.

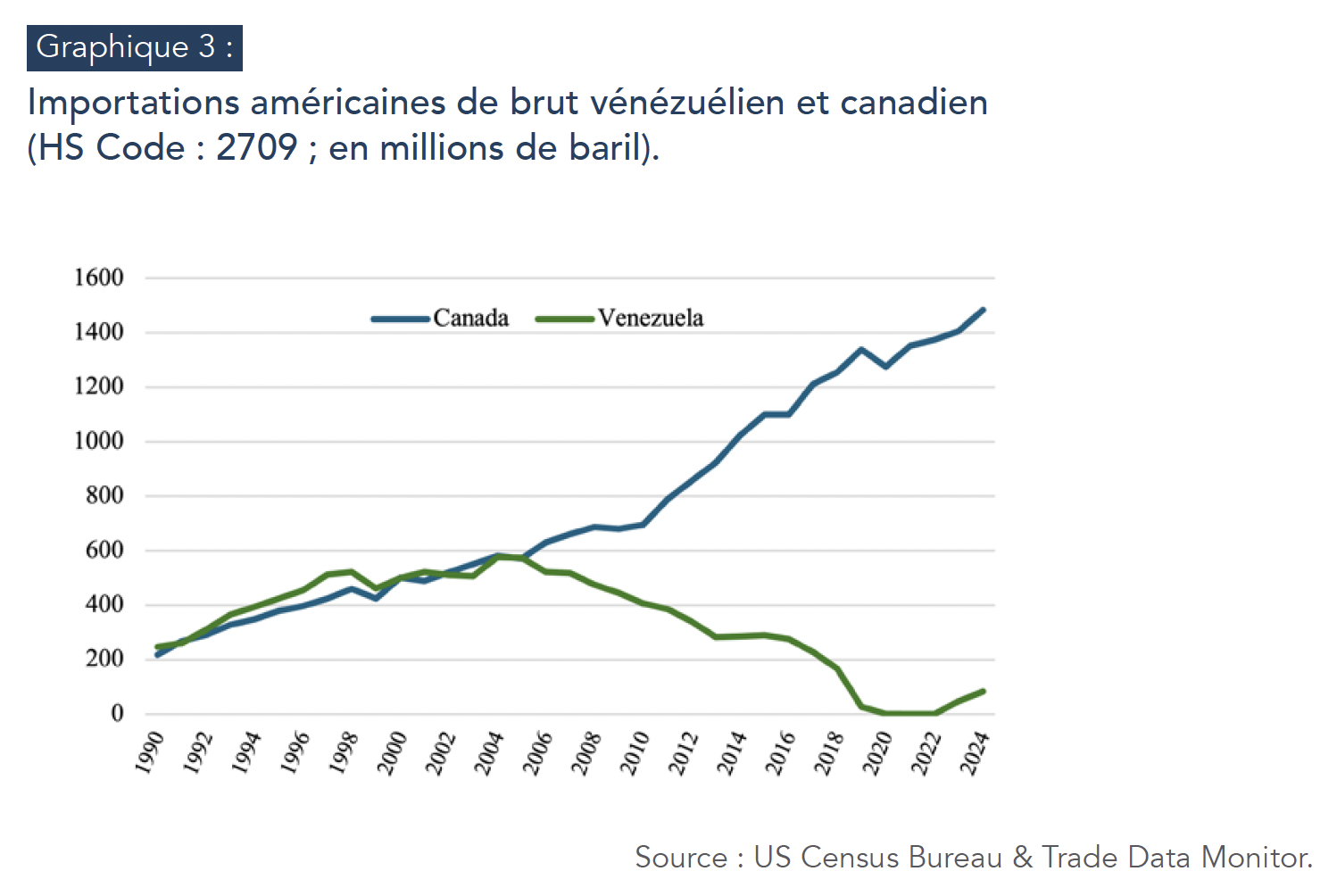

These major uncertainties about Venezuela's oil potential make it necessary to clarify the political and geopolitical reasons for the American offensive. However, it is highly probable that an economic argument may have legitimized it. Because of its physico-chemical characteristics, Venezuelan extra-heavy oil has only a limited place on world markets, but like Canadian oil sands, it is particularly well suited to refineries located around the Gulf of Mexico6. Around 70% of the crude oil purchased by the United States is heavy oil, 60% of which comes from Canada. U.S. imports of Venezuelan crude reached 577 million barrels in 2004, on a par with imports from Canada (graph 3). Their sharp fall since then (-493 million between 2004 and 2024) has been accompanied by a symmetrical rise in purchases of Canadian oil (+903 million over the same period). A resumption of Venezuelan imports would thus have the advantage of limiting American dependence on its neighbor, while at the same time limiting the cost of fuel in the United States, a decisive factor in the purchasing power of the country's households and also in the electoral politics of the Republican president. The refining industry is also particularly rich in jobs in the United States. Access to low-cost oil could therefore boost profit margins and, all other things being equal, sustain the sector's dynamism.

OBVIOUS GEOPOLITICAL AIMS.

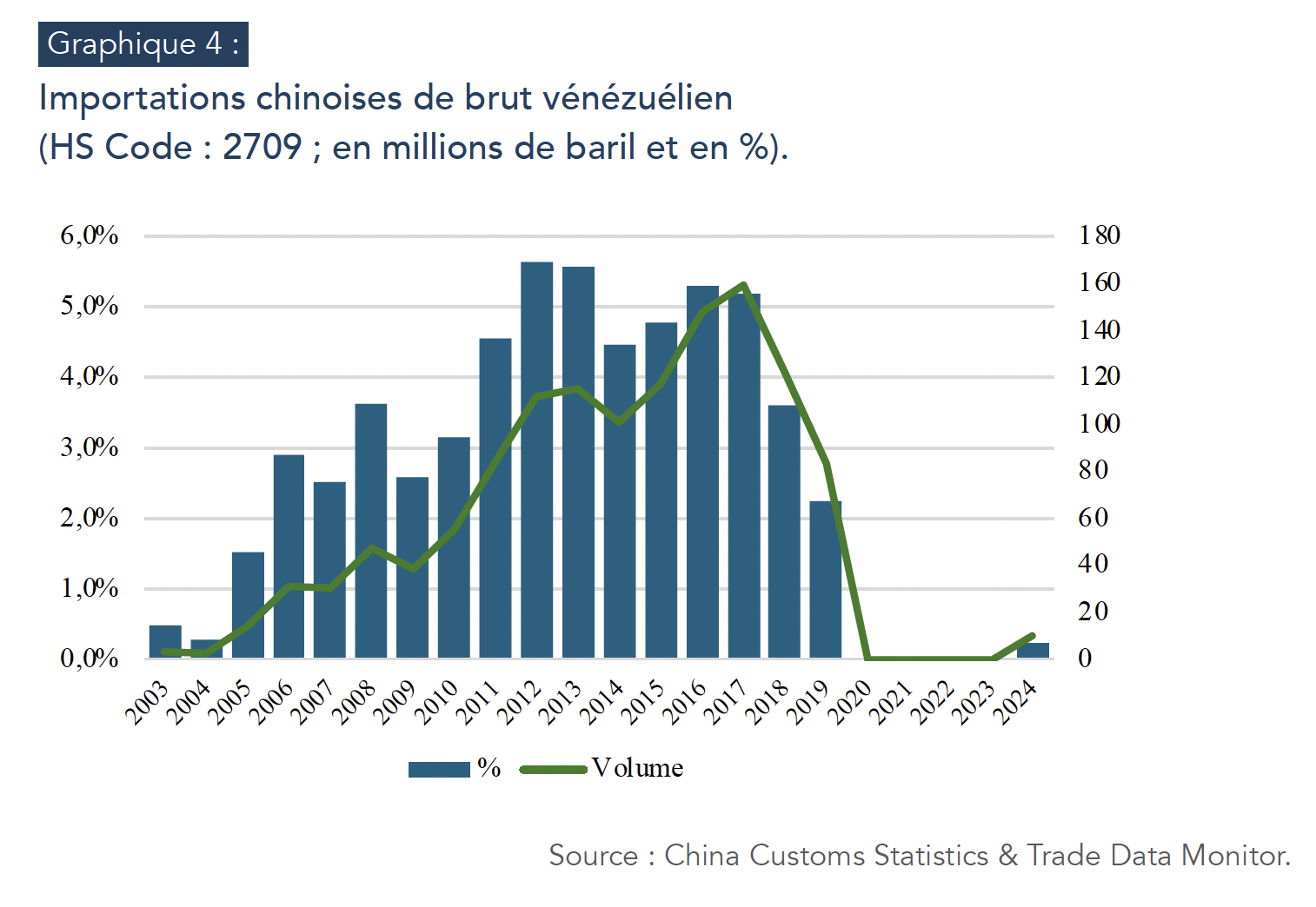

This reorientation of Venezuelan oil flows towards the USA is likely to penalize Cuba and China. While customs statistics for the former are still unavailable, those - official - for the world's second-largest economy do not reveal any significant dependence (graph 4). For example, of the 4 billion barrels imported into China in 2024, only 9.84 million came from Venezuela, putting this country in 21st place among its suppliers (0.25% of total crude imports), far behind Russia, Saudi Arabia, Malaysia, Iraq and Oman (in descending order).

However, these figures may only imperfectly represent the reality of crude oil flows between Venezuela and China, due in particular to various techniques or strategies aimed at concealing the Venezuelan origin of the oil, in order to circumvent US sanctions and the banking risks associated with transactional financing of sanctioned cargoes: reclassification of exports from this country by certain commodity trading houses, use of phantom fleets, ship-to-ship transshipments and falsification of location signals for tankers leaving Venezuela. The so-called "teapots", small independent Chinese refineries, often located in Shandong province, are hungry for Western-sanctioned, and therefore discounted, oil due to their low margins. According to the Kpler news agency, actual flows to China would have been 768,000 barrels/day in 2025, or around 3% of total Chinese crude imports (Downs & Palacios, 2026).

Denial of crude oil exports to Cuba is undoubtedly another reason for American intervention. According to Kpler, Venezuela delivered some 15,000 barrels/day7 to that country for refining and power generation. As Donald Trump has announced, a cessation of Venezuelan exports would be a further tool of pressure on the regime, already widely threatened by the United States in the context of statements made by the American president in the wake of Nicolàs Maduro's capture and extradition8. It remains to be seen whether the new Venezuelan leadership will accede to this request, as interim President Delci Rodriguez has declared that the country will continue to freely exercise its "right to self-determination and national sovereignty" in its relations with Cuba, which "have always been based on fraternity, solidarity, cooperation and reciprocity "9.

CONTROL OVER VENEZUELAN MINERAL RESOURCES?

Oil may not be the only raw material underpinning American intervention. Many media outlets have questioned the importance of the "rare metals" present in the country's subsoil. Put in these terms, however, the question is largely imprecise and thus reveals a persistent lack of understanding of mining reality and, perhaps more generally, of the geopolitics of raw materials. The notion of "rare metals" is misleading and even extremely ambiguous: it refers either to "strategic or critical mineral resources" or to "rare earths", the latter grouping together a set of fifteen to seventeen very specific mineral resources (the fifteen lanthanides, including neodymium and praseodymium, as well as yttrium and scandium). They are among the critical metals identified by most industrialized countries, including the European Union and the United States, but represent only a small fraction.

If we focus on rare earths, Venezuela does not produce them, and according to statistics from the United States Geological Survey (USGS), the country has no significant reserves of rare earths, i.e. those that can be exploited under current technological and price conditions. Rare earths are very likely to be present in the country's subsoil, given its geological wealth, but neither the quantities present nor the conditions for their viable extraction appear to be proven at this stage. As with the debate over Ukraine's subsoil and Washington's support for Kiyv, or the USA's plans for Greenland, there is often confusion between resources and reserves. Even if Venezuela does have rare earths in its subsoil (or other strategic mineral resources), the time of the mine is not the time of geopolitics, and it seems hard to imagine that American intervention would be strongly legitimized by a strategy of securing rare earths. It should also be remembered that the issue of mineral resources must be seen in the context of their value chains. While everything starts with the mine, bottlenecks can occur downstream, particularly in refining. Venezuela has published in January 2018, a mining catalogue10 that confirms this finding, with no mention of rare earths. Using alternately the notions of reserves and resources (which complicates the analysis), this report nevertheless indicates gold resources of 644 tonnes, significant volumes of iron ("proven reserves" of 3.63 billion tonnes), nickel (an estimated 407,885 tonnes in metallic content), bauxite ("inferred resources" of 88 million tonnes), coal, feldspars, diamonds, phosphates, as well as coltan (columbite-tantalite), although the resources of this last mineral are not quantified.

VENEZUELAN ALUMINUM.

Venezuela does, however, have a mining history, particularly in the bauxite/aluminum sector, two resources in the same sector that are also among the strategic metals of many Western countries, and whose "perimeter" goes beyond that of the energy transition. As a reminder, NATO estimates that aluminum, along with graphite, is at risk of being oversupplied for eight out of nine military applications, while China dominates the world market and Russia, with Rusal, is one of the world's largest producers. Several alumina refining and aluminum production units have existed in Venezuela. Founded in December 1960, initially as a joint venture between the American Reynolds group and Corporación Venezolana de Guayana (CVG) before being nationalized, the Alcasa group was able to exploit the Guayana region's vast bauxite reserves, benefit from its abundant hydroelectric potential (due to the Caroni River and the Guri dam, one of the world's largest) and produce up to 100,000 tonnes11 annually, before its decline in the 2000s. Still in the Guayana region, Venalum remains one of Latin America's leading producers12 , with an installed capacity of 460,000 tonnes/year. In practice, however, production volumes are much lower, at 96,000 tonnes according to information gathered by Fastmarkets13.

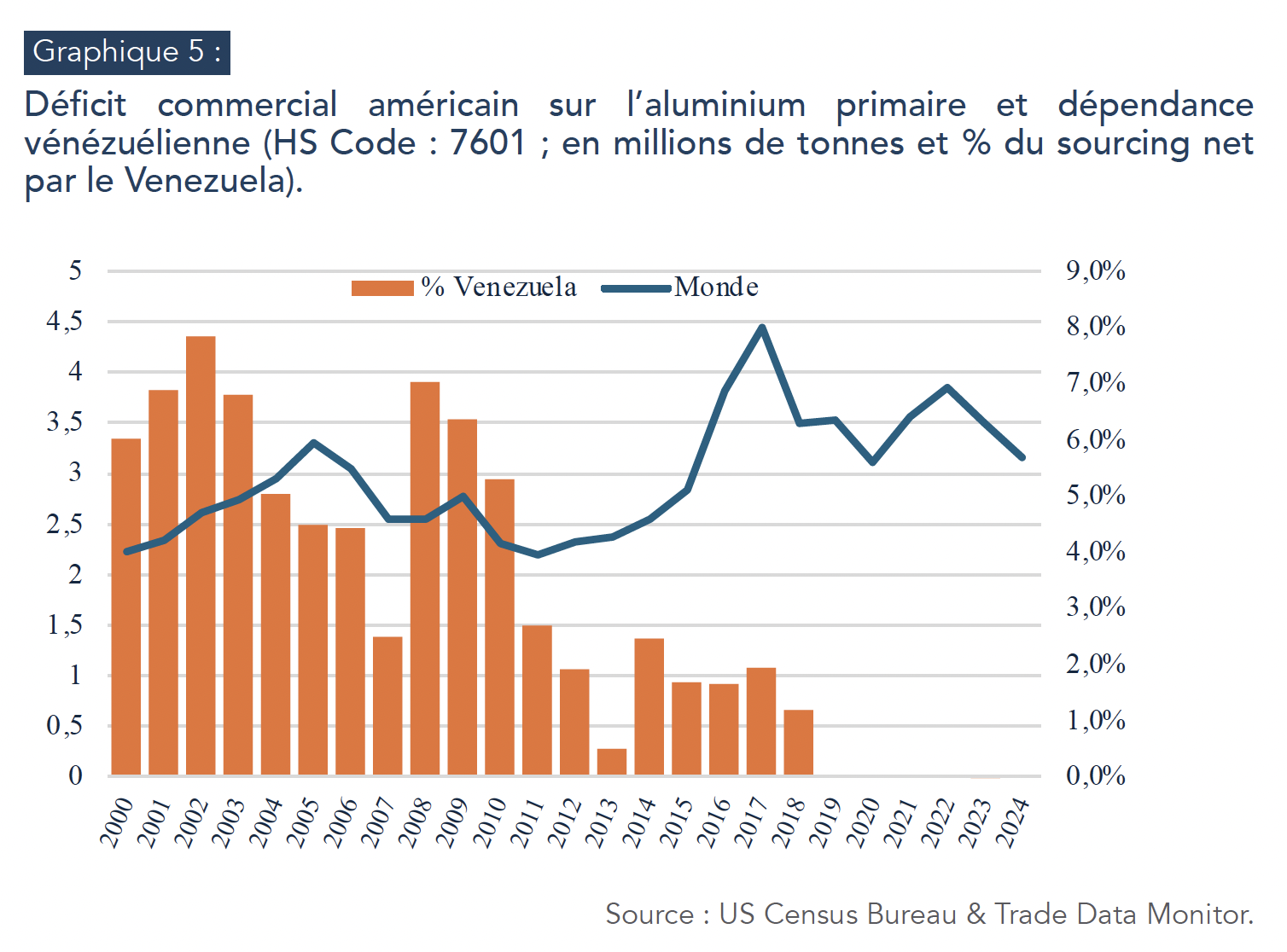

In the past, a significant quantity of Venezuelan primary aluminum has been imported into the United States. In 2002, net imports of this metal from the country reached almost 205,000 tonnes, out of a total of 2.61 Mt. Venezuela accounted for up to 7-8% of US sourcing. If, for the obvious reasons of sanctions against Caracas, these imports have been zero since 2019, the potential for diversification could therefore be interesting for Washington. Of course, as with oil, there is also the question of the investment needed to boost production, which means addressing the country's structural power generation problems14. However, given China's overwhelming domination of aluminum production, as well as Russia-China synergies in the bauxite/alumina/primary aluminum chain, it remains an interesting medium-to-long-term option in the United States' strategy of influence and hyperpower.

TO "RESTORE AMERICAN ENERGY DOMINANCE".

Was the US strategy primarily aimed at the Venezuelan regime because of its democratic deficit, or did it serve a broader ambition to "take back control" of Latin America in the face of China's significant advances? From the renaming of the Gulf of Mexico to the occupation of the Panama Canal and threats against Colombia, there seems little doubt that Washington's expansionist temptations are in line with the Monroe Doctrine. An 1823 political statement aimed at European countries, this doctrine asserts the right of the United States to "manage" the entire American continent (annexation of Texas, overthrow of the Chilean president, etc.).

Salvador Allende, interference in Nicaragua, etc.) in exchange for non-intervention in European affairs and in countries colonized by European countries. Combining political and economic interests, the Monroe Doctrine is explicitly evoked in the United States' National Security Strategy 2025 - or NSS 2025 - made public on December 4, 2025: "After years of neglect, the United States will reassert and enforce the Monroe Doctrine to restore American preeminence in the Western Hemisphere, and to protect our homeland and our access to key geographies throughout the region" (p. 15).

While the ambition here is not to review the new Monroe Doctrine (or "Donroe" by introducing President Donald Trump's name through the prism of raw materials), it is worth noting the Republican administration's commitment to "restoring American energy dominance". It states: "Increasing our net energy exports will also deepen our relationships with our allies while reducing the influence of our adversaries, protect our ability to defend our shores and, when necessary, project our power. We reject the disastrous ideologies of 'climate change' and 'Net Zero' that have done so much harm to Europe, threaten the United States and subsidize our adversaries" (p. 20).

Against this backdrop, a final argument can be put forward, without prejudging the importance of the American intervention. A long-standing territorial dispute exists between Venezuela and Guyana, with the Bolivarian Republic contesting the attachment of the Essequibo region to the latter on the basis of borders defined during the colonial period. The antagonism has been exacerbated since the discovery, in 2015, of vast offshore oil reserves (on the Stabroek block) off the Essequibo, by US oil giant ExxonMobil. In November 2025, the country's crude production reached 900,000 barrels/day, with production capacity set to reach 1.7 Mb/day by 2030. However, Venezuela held a referendum in 2023, the result of which affirmed that the population supported the annexation of Essequibo; it also passed a law officially declaring the territory an integral part of the country, despite international opposition. In a sign of growing tensions between the two countries, a Venezuelan military vessel approached the oil installations of ExxonMobil and its partners in March 2025, which was perceived as a provocation by Caracas towards Georgetown15. Exacerbated since the discovery of the Stabroek oilfields, territorial rivalries between the two countries have been intense. The American intervention thus counters possible threats to Guyana's national interests, reduces the so-called "country risk" and could thus encourage international investment in the country.

CONCLUSION

The American intervention is clearly one of the first operational declinations of Donald Trump's NSS 2025 and, in that respect, one of the markers of the end of the Cold War.

This is the "international order by rule" approach promoted by his predecessor Joe Biden and inherited from President Woodrow Wilson (Hénin, 2026). Raw materials naturally occupy a central place. From this point of view, it's interesting to note the importance of questions surrounding American ambitions regarding Venezuela's potential resources in strategic metals. What's intriguing here is the idea that, in the field of commodities, there could be a motivation other than oil, as if oil were not enough to fully justify American intervention, because the future "necessarily" lies in the mineral resources essential to the energy transition and the digital revolution. Of course, it costs nothing to ask the question, but neither oil nor gas are unfortunately raw materials of the past. And this reality will endure.

Whether it's the Ukraine, Greenland or the DRC, the United States is obviously very interested in strategic mineral resources, but it needs to gain time in the face of China's great advance in all related sectors. Dominating and promoting fossil fuels as much as possible is one way of doing this (as is promoting the dollar in international transactions). In this return to the doctrine of "spheres of influence", which we are witnessing and which considerably reinforces the risk of conflict, mastery of energy and fuel is essential, as is mastery of "basic" raw materials for the military industry, notably bauxite and aluminium, for which Venezuela has interesting potential.

BIBLIOGRAPHY

- Downs, E., Palacios, L. (2026), "US Action Threatens Venezuela-China Oil Flows, Debt Repayment, and Investments", https://www.energypolicy.columbia.edu/venezuela- china-oil-ties-severely-impacted-by-us-action/, blog post, Center on Global Energy Policy at Columbia University| SIPA.https://www.energypolicy.columbia.edu/venezuela-china-oil-ties-severely-impacted-by-us-action/

- Fattouh, B., Meidan, M., Economou, A., Ochoa, O. (2026), "Oxford Institute for Energy Studies Rewiring Venezuelan Crude Oil: Impacts, Risks, and Market Constraints", https://www.oxfordenergy.org/wpcms/wp-content/uploads/2026/01/OIES-PPT- Rewiring-Venezuelan-Crude-Oil-12Jan25.pdf.https://www.oxfordenergy.org/wpcms/wp-content/uploads/2026/01/OIES-PPT-Rewiring-Venezuelan-Crude-Oil-12Jan25.pdf

- Henin, P-Y. (2026), "La stratégie 2025 de sécurité nationale : une autre vision du monde", Notes de l'IRIS, January, https://www.iris-france.org/wp-content/uploads/2026/01/ ObsEtatsUnis_2026_01_NSS2025_Note_EN.pdf.https://www.iris-france.org/wp-content/uploads/2026/01/ObsEtatsUnis_2026_01_NSS2025_Note_FR.pdf

- Messari N. (2025), "The United States and Venezuela: Beyond the Bilateral Dimension, Policy Brief, n°66/25, Policy Center for the New South, https://www.policycenter.ma/ publications/united-states-and-venezuela-beyond-bilateral-dimension.https://www.policycenter.ma/publications/united-states-and-venezuela-beyond-bilateral-dimension.

[1] Proven reserves are defined as volumes of oil whose probability of recovery, given existing extraction techniques and economic conditions, exceeds 90%.

[2] See, in particular, Ambrose, J. (2026), “Dense, sticky and heavy: why Venezuelan crude oil appeals to US refineries”, The Guardian, 5/01. https://www.theguardian.com/business/2026/jan/05/venezuelan-crude-oil-appeals-to-us-refineries.

[3] Merey 16 has an API (American Petroleum Institute) gravity of 16: the lower the value, the heavier the crude oil. When it is below 22° API, it is referred to as heavy crude, and as extra-heavy crude when it is below 10° API. By comparison, Brent has an API gravity of 38, placing it in the category of light crude (above 31.1° API). The sulfur content of Merey ranges between 2.5% and 3.4%.

[4] According to U.S. EIA statistics.

[5] Following that of Carlos Andrés Pérez, who notably created in 1976 the state-owned company Petróleos de Venezuela S.A. (PDVSA) to manage the country’s oil industry.

[6] https://www.reuters.com/business/energy/us-gulf-refineries-ready-run-venezuelan-crude-2026-01-08/.

[7] Some sources provide higher estimates, around 35,000 barrels per day. See, for example: https://www.bbc.com/news/articles/cx2kv2gn62vo.

[8] On January 11, 2026, the U.S. president stated on his social network Truth Social: “Cuba lived, for many years, on large amounts of oil and money from Venezuela. In return, Cuba provided ‘security services’ for the last two venezuelan dictators, but not anymore! There will be no more oil or money going to Cuba - zero! I strongly suggest they make a deal, before it is too late”.

[10] This document can be freely downloaded at the following address: https://www.desarrollominero.gob.ve/wp-content/uploads/2024/04/Minerals_Catalog_2018.pdf.

[11] Or even more, with an installed capacity of nearly 200,000 tonnes per year in the 1990s.

[12] However, this region accounts for only a very small share of global primary aluminium supply. South American production volumes are estimated at 1.417 million tonnes in 2025 by the Aluminium Institute, representing only 2% of global output.

[14] As a reminder, approximately 15,000 kilowatt-hours are required to produce one tonne of primary aluminium.

[15] https://apnews.com/article/venezuela-guyana-oil-exxonmobil-1142faf844adffab680b3b643bd27799