Publications /

Opinion

The commercial and geopolitical interdependence between China and Latin America makes any U.S. claim to promote a "decoupling" between them impractical. Digital technologies and critical minerals will be in the crosshairs of the North American National Security Strategy

In November 2025, the White House released a new version of the United States government's "National Security Strategy". The section on the Western Hemisphere is presented as "the Trump corollary to the Monroe Doctrine". Recall that the Monroe Doctrine was announced in 1823 by U.S. President James Monroe, with the central idea that European powers should no longer "colonize or interfere in the Americas".

Donald Trump's version aims to:

"[...] After years of neglect, the United States will reassert and enforce the Monroe Doctrine to restore American preeminence in the Western Hemisphere, and to protect our homeland and our access to key geographies throughout the region. We will deny non-Hemispheric competitors the ability to position forces or other threatening capabilities, or to own or control strategically vital assets, in our Hemisphere."

In place of European powers, China's growing presence in the hemisphere is a central theme in the document. It speaks of reinforcing the U.S. role as the "partner of choice," limiting China's ability to secure lasting positions in critical sectors such as infrastructure, energy, telecommunications, and digital networks.

This is not something new, of course. In 2019, I participated in a documentary produced by the Foreign Policy Association and aired by the PBS (Public Broadcasting System) network in which North American politicians "warned" Latin Americans about "traps" embedded in Chinese financing and investments in the region. The typical response from Latin Americans was to ask what the U.S. proposed to put in China's place, as the Asian country has filled a certain void in the recent past. The new version of the "Strategy" effectively signals ways to reaffirm the country's proactivity in the region. To what extent, and how, would this be done?

https://www.youtube.com/watch?v=DMIBblyHkXY

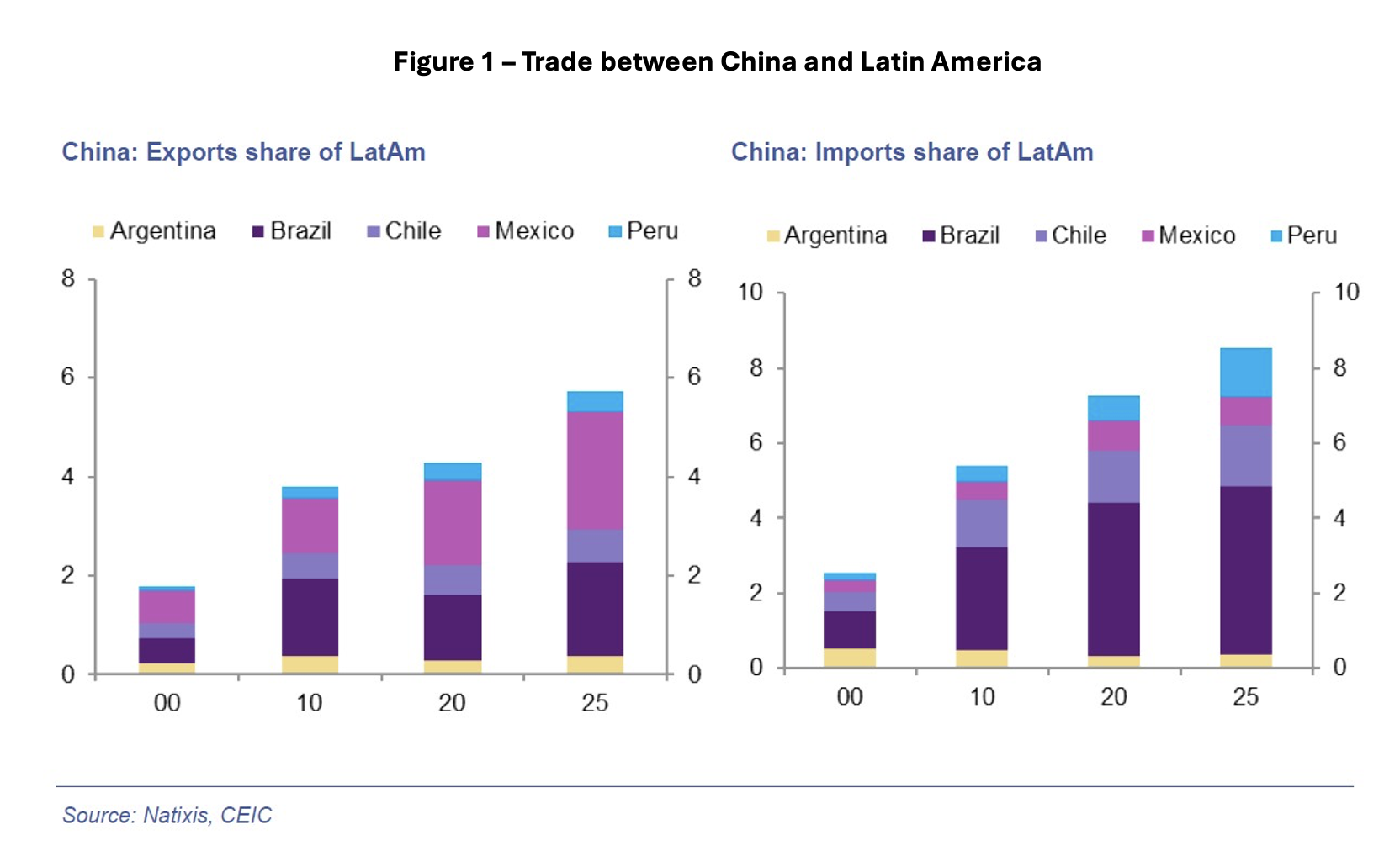

External trade between China and Latin American countries has experienced exuberant growth over the last two decades, at a rate equivalent to 10 times the growth of trade between the region and the United States (Garcia Herrero et al, 2026) (Figure 1). When Mexico is excluded, China currently leads the region's external trade. Colombia, Mexico, and Argentina have persistent bilateral trade deficits, while Brazil, Chile, and Peru have surpluses. The use of trade protectionism by the U.S. does not favor any prospect of replacing this commercial link.

How about Chinese investments and finance? Latin America and the Caribbean are the second-largest destination for Chinese direct investment (after Asia), but overall stock levels remain limited. In 2024, China accounted for less than 5% of total investment in the region, compared to 38% from the United States and about 15% from the European Union.

Essentially, Chinese investment has not kept pace with the sharp increase in trade. On the other hand, there has been a metamorphosis in capital flows from China to Latin America (Canuto, 2019). And the Belt & Road Initiative is now in a “3.0 phase” (Canuto, 2024).

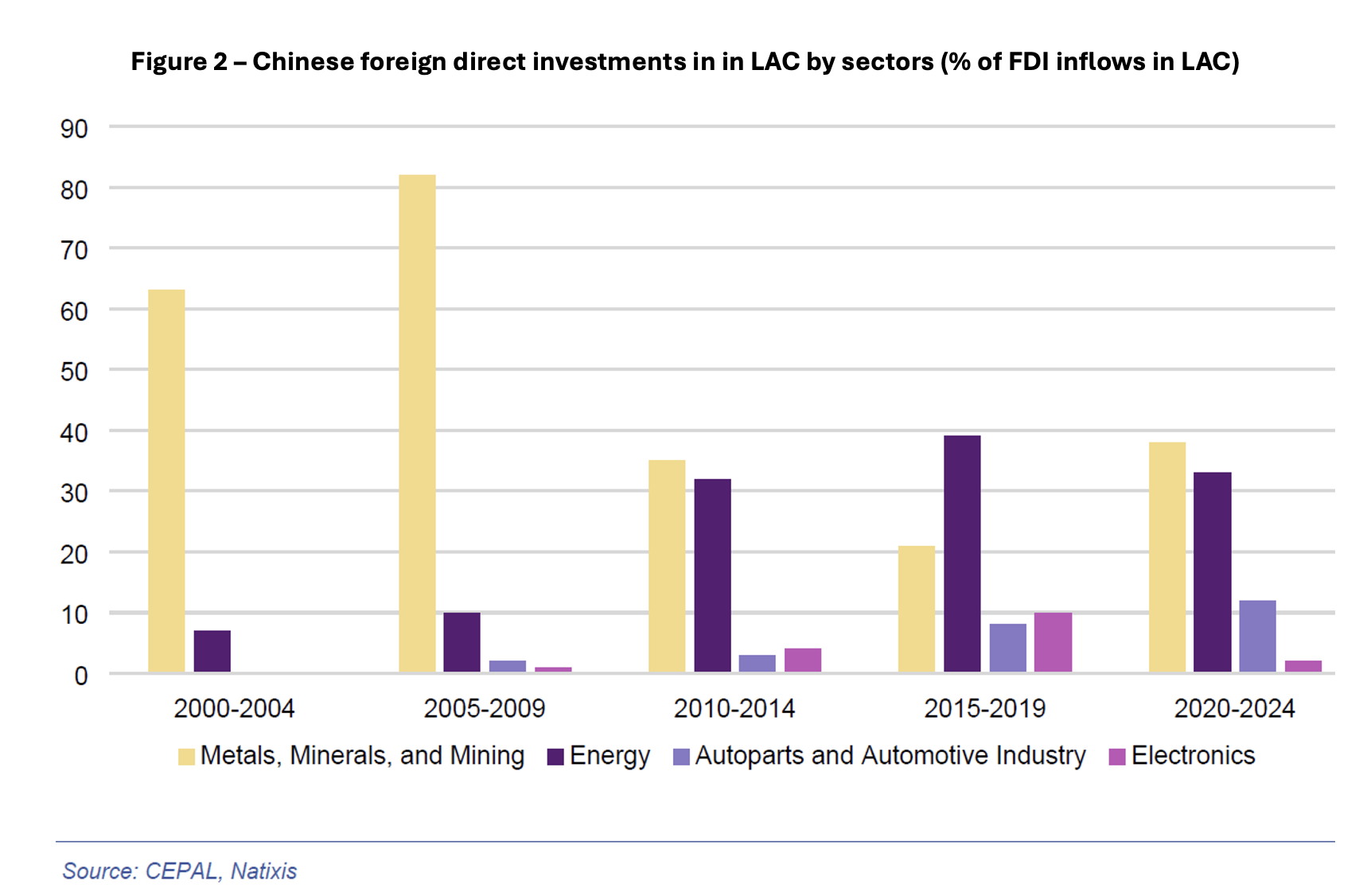

Chinese investment in the region has become more diversified in terms of sectors and geography. There has been a shift from a heavy focus on natural resources—about 95% of direct investment and finance from 2005 to 2009—to a composition where a growing share is destined for energy (including renewables since 2010) and the automotive sector (Figure 2). In the case of Brazil, there have been signs of increasing indirect engagement with agriculture production.

Brazil remains the primary destination (over 30% from 2020 to 2024), though its share has decreased as Argentina, Mexico, and Peru attract more investment. China's presence occurred predominantly through loans (project financing) rather than Foreign Direct Investment and consisted largely of acquisitions rather than "greenfield" projects. However, recent automotive investments, as well as in energy and infrastructure, suggest a path change.

In the area of international payments, a Chinese footprint has also been established (Garcia Herrero et al, 2026). The People's Bank of China (PBC) built a global network to support payments in renminbi, including the CIPS (Cross-Border Interbank Payment System), Local Currency Settlement agreements (LCS) and Bilateral Swap Lines (BSL) with other central banks.

CIPS makes cross-border payments in renminbi faster and cheaper, while also offering a messaging system alternative to SWIFT for direct participants. In South America, the number of indirect CIPS participants rose from 17 to 31 in 2024. China signed Local Currency Settlement agreements (LCS) with Brazil and Argentina, contributing to their emergence as the largest users of the Chinese currency in the region.

Concurrently, the PBC established Bilateral Swap Lines (BSLs) with Latin American countries. Brazil, Argentina, and Chile hold swap lines with China, intended to serve as a precautionary liquidity buffer rather than being actively utilized. These swap lines provide a safety net for central banks through bilateral currency swaps.

Argentina's experience in 2023 serves as a prime example of how a BSL can alleviate pressure on foreign exchange reserves—even if the instrument is restricted to payments denominated in renminbi: these payments were subsequently converted into U.S. dollars, saving Argentina from defaulting on its obligations to the IMF (Wang and Canuto, 2023). It comes as no surprise, then, that the U.S. Treasury was willing to arrange a bilateral currency swap with Argentina last year!

Regarding the Donroe Doctrine, the commercial and geopolitical interdependence between China and Latin America renders impractical any U.S. aspiration to promote a "decoupling" between them. Conversely, as pointed out by Garcia Herrero et al (2026):

- Control at strategic points – The United States has been exerting stricter control over Chinese assets in the region, particularly at strategic logistical choke points—such as the Panama Canal and Venezuela’s oil sector—areas in which China’s presence had been growing.

- Pressure via tariffs – Mexico imposed a 50% tariff on Chinese electric vehicles—a measure widely perceived as the result of U.S. pressure.

- Visa restrictions – Last February, the State Department decided to implement visa restrictions on three Chilean government officials. This action was taken in response to these officials' alleged support for a Chinese-funded submarine cable project, which the U.S. deemed a threat to critical telecommunications infrastructure and to broader regional security.

- Criticism regarding a port in Peru – Regarding the Chancay mega port—built by China near Lima—the U.S. State Department went so far as to declare that Chinese control over such strategic infrastructure in Peru could undermine the country's sovereignty, warning that "cheap Chinese money costs sovereignty."

Strictly speaking, the Donroe Doctrine will be tentatively applied—extending beyond issues of military security in the narrow sense—to the multiple dimensions of the U.S.-China technological rivalry that we addressed here last December (Canuto, 2025). The supply chain for critical minerals and rare earths, as well as digital networks, will constitute specific focal points.

-------------------------

Canuto, O. (2019). How Chinese Investment in Latin America Is Changing, Policy Center for the New South, March 14.

Canuto, O. (2024). Whither China’s Belt and Road Initiative? Policy Center for the New South, January 2.

Canuto, O. (2026). The New South as a Frontline of the U.S.-China Technological Rivalry, Policy Center for the New South, February 11.

Garcia Herrero, A.;Berber, B.; Gorguet, E.; and Mu, H. (2026). Despite Donroe Doctrine, Latin America and China to remain BFFs but with a twist, Natixis, April 14.

Wang, X. and Canuto, O. (2023). The Dollar-Renminbi Tango: The Impacts of Argentina’s Potential Dollarization on its Relations with China, Policy Center for the New South, PB - 39/23, October 13.