Publications /

Opinion

We are now in the fifth week since the U.S. airstrike that killed top leaders of the Iranian regime, initiating a war involving the United States and Israel against the country. More than a month of mutual bombardments between Iran and Israel has ensued, extending to other Persian Gulf nations, U.S. military installations—and even Cyprus. From a global perspective, the impact has stemmed primarily from disruptions to regional production of goods and the blockade of the Strait of Hormuz.

An impasse currently prevails, suggesting a prolongation and probable intensification of the war: while U.S. troops are converging for potential air and naval invasions—and Trump, on March 26, extended his deadline to bomb Iran’s power plants to April 6—the Iranians have vowed to assert sovereignty over the Strait and impose heavy tolls on traffic passing through it. It is no coincidence that Fatih Birol—head of the International Energy Agency (IEA)—stated that a war with Iran poses the greatest threat to global energy "in history."

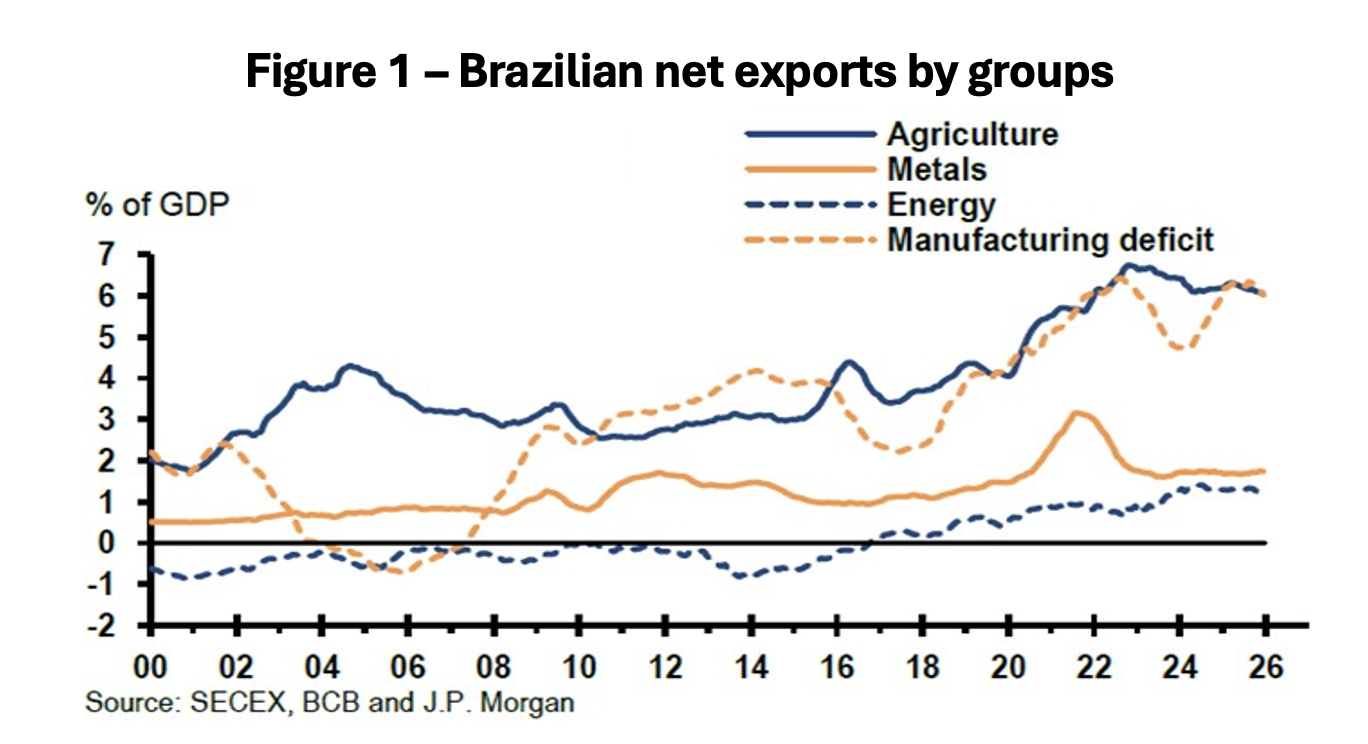

The channels through which this war impacts the Brazilian economy are manifold. On March 27, the price of Brent crude oil briefly surpassed US$110 per barrel. While this development improves the country's terms of trade—given that it is now a net oil exporter (Figure 1)—this price surge has already begun to drive up domestic costs for gasoline, diesel, and jet fuel, thereby increasing transportation, logistics, and airfare costs, and fueling inflation in the short term. Additionally, it is worth highlighting the country's dependence on imported fertilizers.

The OECD’s Interim Economic Outlook 2026 report, released this week, indicates a slight downward revision in its GDP growth projections for Brazil for 2026 and 2027—dropping from 1.7% to 1.5% this year, and from 2.2% to 2.1% next year—compared to the report issued in December. The overall trade balance is expected to benefit from rising prices for crude oil exports. Conversely, it is worth noting the negative, albeit less significant, impact that freight and other costs will have on other components of the current account of the balance of payments.

Regarding trade with Middle Eastern countries affected by the war, Brazil exports goods amounting to approximately 0.6% of its GDP to the region, while imports account for roughly 0.3% of GDP. Certain specific sectors will suffer heavier impacts, such as corn exports, 25% of which are destined for the Middle East, according to Cassiana Fernandez et al. (2026). It is also important to highlight that 15% of Brazil's fertilizer imports originate from the war-affected region—fertilizers with properties that render them non-substitutable by those from other sources, such as those imported from Morocco.

Tax revenue is expected to rise, reflecting the increase in oil exports. The Ministry of Finance estimates that a Brent crude price of US$100 per barrel would result in an increase of nearly 1% of GDP in additional revenue relative to the 2026 budgetary projections.

At the same time—as in many other countries—fiscal measures have been implemented to mitigate the effects of rising diesel prices. On March 12, the government eliminated federal taxes on diesel (PIS/Cofins), imposed a 12% levy on crude oil exports, and established a 50% tax on diesel exports, in addition to launching a direct subsidy of 0.32 reais per liter (equivalent to 6% of the price of 5.42 reais per liter on March 1), effective until December 2026. Analyses by industry experts to which I have had access suggest that this package—already in force via provisional measures and awaiting parliamentary approval—tends to be fiscally neutral.

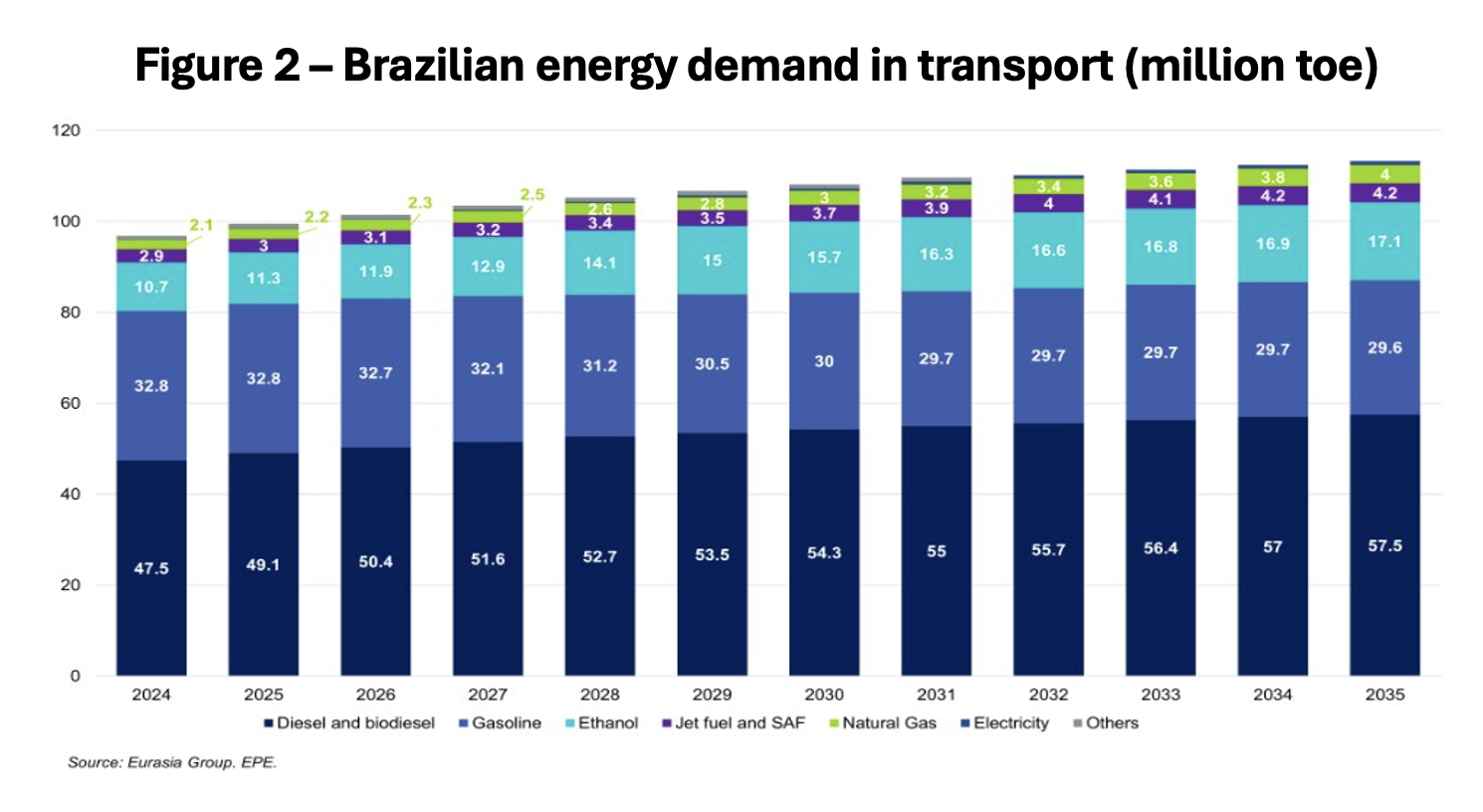

Although Brazil has become the world's sixth-largest oil exporter and possesses the globe's eighth-largest refining complex—according to Eurasia Group (2026)—the country still imports 25% of the diesel it consumes. Given the critical role this fuel plays in freight transport in the country (Figure 2) and in electricity generation across much of the Amazon region—where three million people rely on isolated diesel-powered systems—there is naturally concern regarding the impact of its price and availability should the war be prolonged. Beyond the damage already inflicted on production facilities in the war-affected region, there is also the fact that transit via the Strait of Hormuz lacks sufficient alternative transport routes in the short term.

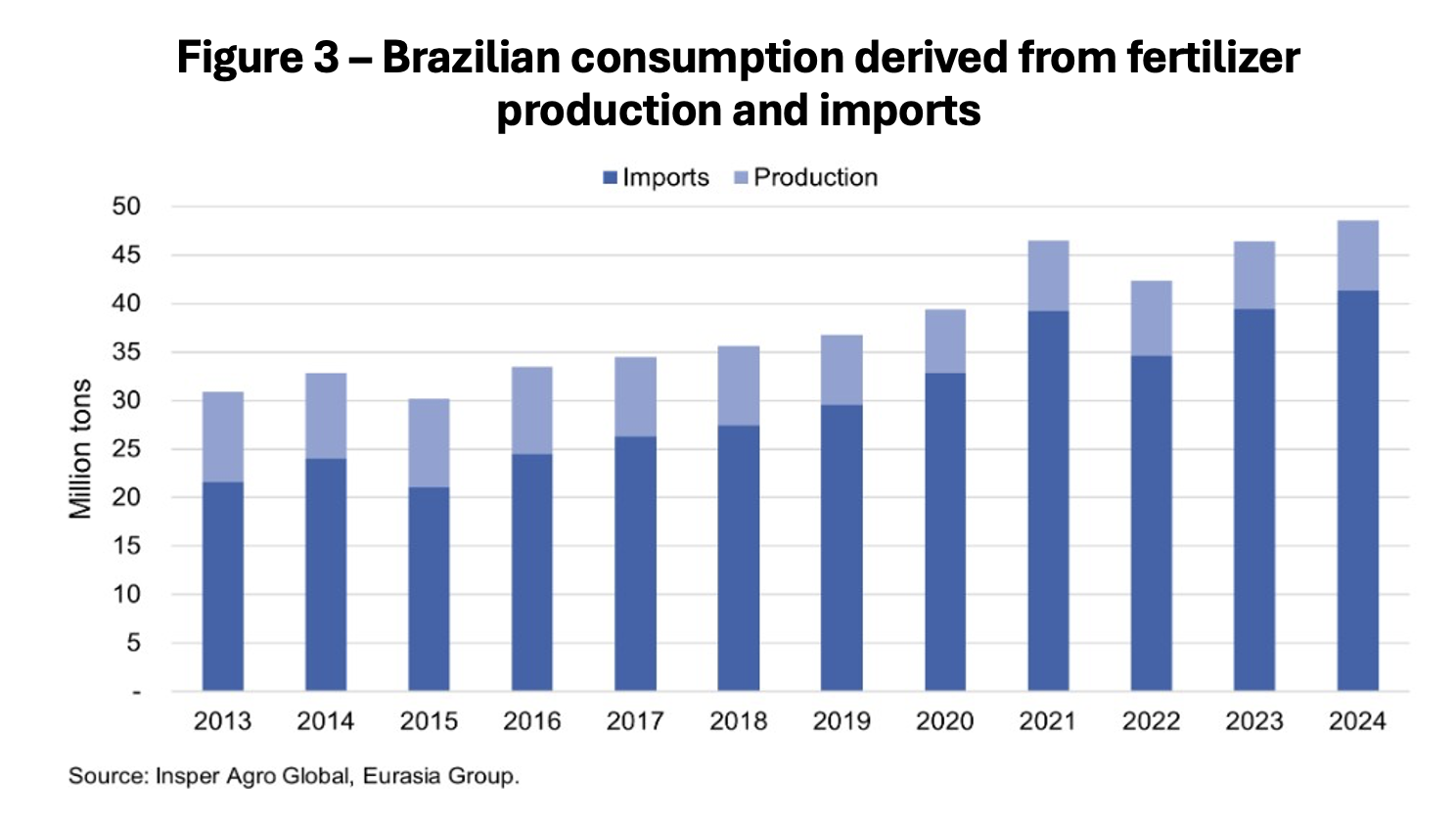

In a scenario where the war is prolonged, the issue of fertilizer dependency becomes an even greater cause for concern. Most Brazilian soil is naturally nutrient-poor, necessitating the use of fertilizers to sustain high crop yields. According to Eurasia Group (2026), fertilizers can account for as much as 34% of effective operational costs for summer corn, 30% for wheat, and 27% for soybeans and second-crop corn. Most of the country's current crop is already in the harvest phase, while producers have until roughly September to secure inputs for the next planting cycle.

Brazil currently accounts for 60% of global soybean exports and is also the world's largest producer and exporter of beef, among other food products. However, it is also the world's largest importer of fertilizers, relying heavily on imports for all three primary nutrients. Figure 3 depicts the weight of fertilizer imports relative to domestic production levels.

Iran, Qatar, Saudi Arabia, Oman, and the United Arab Emirates accounted for 36% of Brazil's urea imports in 2025—shipments that are currently blocked due to the closure of the Strait of Hormuz. Urea prices in Brazil surged by 35% in the first weeks of March and are likely to rise further as long as the Strait of Hormuz remains closed (Eurasia Group, 2026). Exposure to phosphates is also significant: 78% of Brazil's phosphate consumption is imported, and China—historically a key alternative supplier—has restricted exports to safeguard its domestic food security since the onset of the conflict.

If access to fertilizers remains restricted through September, Brazil faces a high risk of shortages and rising domestic prices—potentially as early as the 2026/2027 crop season—as highlighted in technical notes produced by the Executive Secretariat of the Ministry of Agriculture and reported by Folha de S. Paulo. These notes point to a potential phosphate deficit of between 1 and 3 million tons—equivalent to approximately 20% of Brazil's total demand.

There are also monetary and financial transmission channels through which the war impacts Brazil. The prospect of worsening inflation has already prompted the Central Bank to slow the pace of its interest-rate reductions, opting for a cut of just 25 basis points—to 14.75%—this month. One must also consider the trajectory of the U.S. dollar relative to other currencies, including the real.

Financial conditions abroad have deteriorated significantly. Global stocks and bonds suffered their largest combined sell-off this month since 2022, as the energy shock triggered by the war in Iran left investors with "nowhere to hide"—to borrow a phrase from Emily Herbert in the Financial Times. In the U.S., Treasury yields have fluctuated within a wide range on many days since the war began, as investors reassess the extent to which rising oil prices will feed into inflation and affect the Federal Reserve’s outlook on interest rates.

Strictly speaking, however, for the Brazilian economy, the greatest concern centers on diesel—and, above all, on fertilizers.

Cassiana Fernandez, Mirella Mirandola Sampaio, and Vinicius Moreira. “Brazil: Economic Outlook after the Oil Shock”, JPMorgan, Global Economic Research, 19 March 2026.

Eurasia Group, EG Brazil Research, “Brazil - Prolonged Iran Conflict Could Trigger Diesel And Fertilizer Shortages”, 27 March 2026.