Publications /

Policy Brief

Policy Brief

The roller-coaster ride of Chinese commodity markets

July 27, 2015

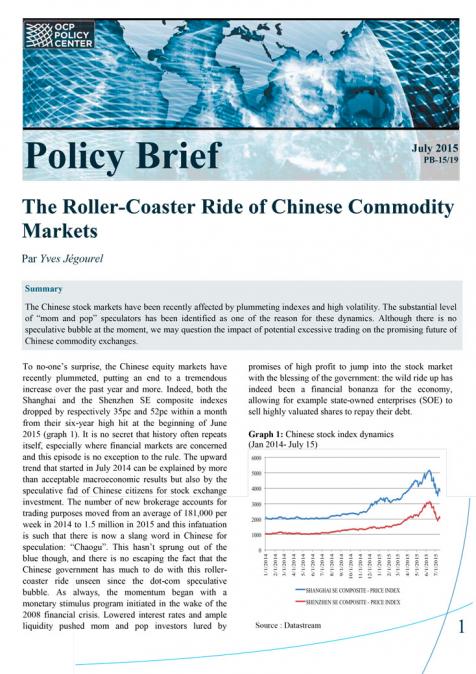

The Chinese stock markets have been recently affected by plummeting indexes and high volatility. The substantial level of “mom and pop” speculators has been identified as one of the reason for these dynamics. Although there is no speculative bubble at the moment, we may question the impact of potential excessive trading on the promising future of Chinese commodity exchanges.