Publications /

Opinion

WASHINGTON-The December 2020 U.S. Treasury Report (hereafter referred to as the TR) to Congress singled out Vietnam and Switzerland as currency manipulators. In Vietnam’s case, it is surprising that the U.S. Treasury openly expressed its concerns about a country that graduated from the group of low-income countries only a few years ago. Additionally, Vietnam’s GDP per capita and total GDP are a fraction of the U.S.’s, but the country is assessed in the same way as developed countries, including Switzerland and Germany, and/or as a large country, such as China and India.

This policy note assesses the merits of the U.S. Treasury report and the implications for Vietnam. It concludes that while the U.S. Treasury is correct that Vietnam has to adjust its policies, its emphasis on the exchange rate as a policy variable is misplaced. Vietnam needs to raise the productivity of its domestic economy through reform of state-owned enterprises and by leveling the playing field between domestic and foreign-owned companies. Exchange rate adjustments are not directly linked with these necessary reforms at this stage and may worsen the current distortions.

Unless the Biden administration reverses the Treasury approach, the decision to classify Vietnam as a currency manipulator has implications beyond any particular country. Hereafter, any developing country, rich or poor, whose macroeconomic management succeeds in achieving high economic growth through exports, could risk being treated the same way. If this classification entails higher U.S. tariffs on those countries, it would discourage many developing countries from following the virtuous development path international institutions have long advocated: higher exports leading to higher income and higher standard of living. Instead, higher exports would lead to higher tariffs, lower world trade and lower welfare.

Background. Under 1988 and 2015 legislation, the U.S. Treasury Secretary must report to Congress on certain aspects of international economic and exchange rate policies. The 1988 Act requires the Treasury Secretary to assess whether a country manipulates its bilateral exchange rate with the U.S. dollar to prevent effective balancing of payments adjustments or to gain unfair competitive advantage in international trade. The 2015 Act requires the Treasury Secretary to monitor its major trading partners’ macroeconomic and currency policies. The TR thus applies three criteria to trading partners with bilateral trade in goods with the U.S. of at least $40 billion:

- Those with at least a $20 billion trade surplus with the U.S. over a 12-month period;

- Those with a current account surplus of at least 2% over a 12-month period; and

- Those with persistent one-sided intervention in foreign currency purchases of at least 2% of GDP over a 12-month period, and whose intervention frequency is at least six months out of a 12-month period.

The TR observes:

Vietnam has tightly managed the value of the dong relative to the dollar at an undervalued level since 2016. Vietnam has applied this policy consistently in periods of both appreciation and depreciation pressure. Additionally, Vietnam entered 2019 with a relatively low level of reserves. Over the four quarters through June 2020, however, Vietnam conducted large-scale and protracted intervention, much more than in previous periods, to prevent appreciation of the dong, in the context of a larger current account surplus and a growing bilateral trade surplus with the United States. Intervention has also contributed to undervaluation of the dong on a real, trade-weighted basis, with the real effective exchange rate undervalued in 2019.

It therefore concludes:

Treasury therefore assesses based on a range of evidence and circumstances that at least part of Vietnam’s exchange rate management over the four quarters through June 2020, and particularly its intervention, was for purposes of preventing effective balance of payments adjustments and gaining unfair competitive advantage in international trade. Hence, Treasury has determined under the 1988 Act that Vietnam is a currency manipulator.

Is the TR factually correct? The TR decision is based on the following claims:

- Vietnam has kept its currency undervalued since 2016.

- Vietnam was found to have its currency undervalued by 8.3% in 2018 by the International Monetary Fund in its 2018 Article IV Report (IMF, 2018).

- Vietnam then entered 2019 with a low level of reserves, which it built up by buying dollars, in the process preventing the appreciation of the dong and keeping the dong/dollar real exchange rate low.

- Then, the TR determined that in the second half of 2019 and the first half of 2020, the Vietnam currency was kept undervalued.

Most of the TR analysis was based on information derived from the IMF 2018 and 2019 Article IV Reports.

Issues. There are a number of issues with the argument that Vietnam is a currency manipulator:

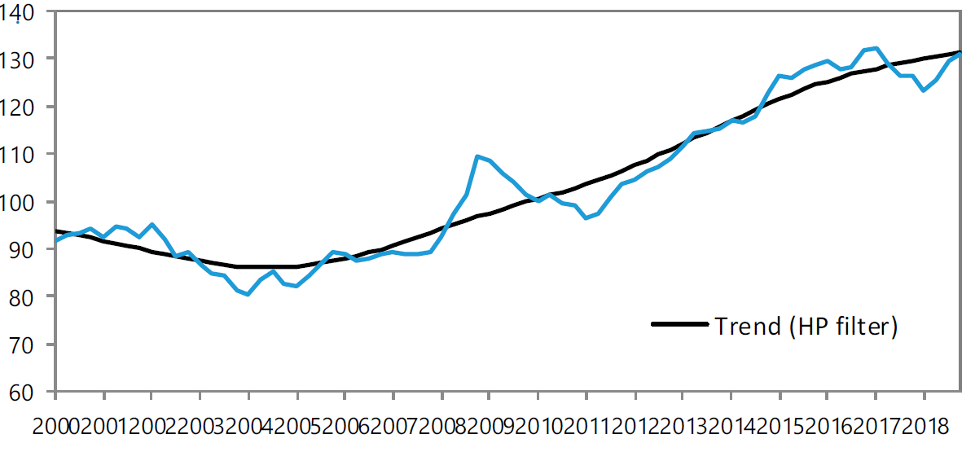

- Real effective exchange rate dynamics. In measuring the impact of exchange rate adjustments on the U.S.-Vietnam trade balance, it’s more accurate to use the real effective exchange rate (REER) since it takes into account the weighted average of Vietnam's dong in relation to an index or basket of other major currencies, among which the dollar carries a rather heavy weight. Figure 1, from the 2019 IMF Staff Report, shows the evolution of the REER since 2000. The figure clearly shows that the REER has been appreciating since 2005. The TR also noted that the REER appreciated by 22% in 2015 (TR, p. 52).

Figure 1: Vietnam: Real effective Exchange Rate, 2000Q1-2018Q4

(2010=100)

.png)

Source: IMF staff estimates. Note: An increase in the index shows an appreciation.

It is relevant to point out here that the IMF notes in its 2019 report (our emphasis):

“In 2017, the REER depreciated by 4.4 percent, as the Dong remained pegged to a weakening U.S. dollar. The trend reversed in 2018 and the REER appreciated by 3.5 percent through the year” (IMF, 2019, p. 36).

- Methodology. To assess overvaluation or undervaluation, the IMF uses two main methodologies: the REER-based model and the External Balance Assessment (EBA) model. These two models sometimes provide competing results and IMF staff uses their judgments to choose one over the other. Nonetheless:

“The EBA models provide numerical inputs for the identification of external imbalances but in some cases may not sufficiently capture all relevant country characteristics and potential policy distortions. In such cases, the individual economy assessments may need to be complemented by country-specific knowledge and insights” (IMF External Report, 2020, p.61).

In the case of Vietnam, if one uses the EBA approach, the dong was considered undervalued (by 8.4% in 2018 according to the IMF), but if one uses the traditional equilibrium real exchange rate approach, the dong would be considered “substantially” overvalued (IMF 2019, p. 36). IMF staff chose to use the former rather than the latter, based on their subjective judgment, a position that the TR also takes and mechanically applies to Vietnam.

A question must also be raised over the External Balance Approach itself, which the IMF developed in 2013. Using it to measure the relationship between policies and Vietnam’s trade balance may be inaccurate. First, Vietnam was not among the 40 to 49 countries used to conduct the EBA model. Second, estimates from this model carry sizable standard errors. For example, the ranges of uncertainty for current account-based gaps are plus or minus 1 percent of GDP. Third, Vietnam’s foreign trade, including its structure, direction, and policy pattern from 2015–2020, was substantially different from that of the 1990–2000 period, which the model also relies on. Fourth, as the 2018 Report noted, the EBA-lite model does not account for the fact that the FDI sector in Vietnam has very few links to the domestic economy. Finally, as the IMF itself pointed out in its 2013 paper on the EBA methodology[1]:

“The underlying difficulty (of EBA) is that the positive empirical analysis still leaves one with an incomplete understanding of CA and REER levels and movements: there remains an unexplained, residual component, one that in many cases will be too large to completely ignore. In such a case, the challenge is to interpret that residual appropriately, since it can reflect policy distortions but also might reflect uncaptured fundamentals or other limitations of the empirical analysis (including measurement error, sampling error as well as possible misspecification)….In light of the above, as well as the element of uncertainty that comes with any econometric analysis, it is suggested that EBA be seen as a tool that provides useful—and multilaterally consistent—estimates to inform and guide assessments, rather than as a mechanical means of generating a final external assessment for each and every economy” (IMF, Phillips et al., 2013, p. 36).

- The year 2020. Because of the COVID-19 pandemic, 2020 was a special year in which many countries saw declining current account deficits or expanding current surpluses because of lower demand for imports resulting from restrictions on the economy. As an exceptional year, 2020 should not be included in the TR assessment, which has long-term consequences.

A new Article IV Report was prepared in November 2020, but only a press release has been published at time of writing. In this press release, nothing was said about Vietnam’s exchange rate policy, even though the Article IV Report’s primary purpose was to monitor Vietnam’s economic and financial policies and their impact.

- International reserves. The TR then states that Vietnam kept its currency undervalued to build up reserves. But reserve accumulation is necessary and consistent with IMF advice. Even after a substantial build-up, the current reserve level is considered below adequate (76% of the adequacy metric, according to the IMF). Note that the vast majority of countries considered in the U.S. TR are developed countries, so their currencies are convertible—they have much less need to accumulate reserves. In the context of a small, developing country, and indeed if the Treasury is correct in its assessment that Vietnam is following a fixed exchange rate regime, then there is clearly a need to have an ample buffer of reserves. In 2019, Vietnam’s international reserves amounted to about 2.5 months of imports, compared to 7.6 months for the Philippines.

What the TR should focus on. There are two important points that should form the basis of the discussion agenda between the U.S. and Vietnamese authorities on how to fix the large bilateral trade imbalance between them.

First, the Vietnamese economy is driven by two separate sectors: foreign-invested enterprises (FIEs) and the domestic economy. As the IMF has noted, the former drives the goods trade surplus, particularly in electronics and other manufacturing, while the latter runs a trade deficit and has very low productivity. For example, the IMF estimated that the former generated a trade surplus of 15.5% of GDP in 2018, while the latter ran a trade deficit of 8.7% of GDP. The productivity of the domestic sector is about 20% that of the FIE sector. Therefore, the best way to adjust the real exchange rate is to raise domestic sector productivity. But this may take some time because it involves structural reforms, particularly of public enterprises. The TR should focus more on the non-FDI domestic economy in Vietnam. Meanwhile, because of this dual economy, bilateral trade between the U.S. and Vietnam should take into account the profit outflows of the FIE sector. In fact, Vietnam has run consistent, modest deficits in services trade over the last two decades.

Second, while the size of its overall current account balance is not different from that of Korea or Taiwan, when these economies were at Vietnam’s current stage of economic development (in the early 1980s), Vietnam needs to balance its international trade by shifting bilateral imports from trade partners like China to the U.S. In this context, it should be noted that at present, Vietnamese exports are overstated compared to the value added because Vietnam mostly performs the final assembly stage in global value chains.

Macroeconomic management. Capital inflows also complicate management of the Vietnamese economy. Vietnam has been flooded with FDI (some of which actually follows from U.S. Treasury advice to move from China to countries such as Vietnam and India), and worker and other remittances. The dilemma facing the authorities is that while these flows tend to be regarded as a positive sign of investor confidence in the country, they impose a high cost on the domestic economy. If the authorities adopt a flexible exchange rate regime, the effect on exports will be devastating. If they adopt a fixed, or relatively fixed, regime, in an open capital account, the monetary authorities would need to either: a) sterilize inflows by issuing domestic denominated bonds or raising reserve requirements, in which case domestic interest rates would rise further and attract even more capital; or b) monetize the inflows (buying dollars from foreign investors) so that the money supply—and with it, inflationary pressures—will rise. The budget or financial sector or both will have to bear the sterilization cost, while consumers at large have to bear the cost of monetization. Monetization, therefore, is costly and has a major impact on monetary and exchange rate instability, especially in economies in the development stage.

This dilemma can only be solved by fiscal policies and productivity improvements. A temporary, large fiscal surplus is important to absorb the sterilization cost mentioned above, to counter the decline in private savings, and to contain domestic absorption. But when the budget faces pressures from a pandemic, as currently with COVID-19, management of foreign exchange inflows becomes much more difficult, and the trade-off between fiscal, monetary, and exchange rate policies becomes much clearer.

Conclusion. The TR could have pointed out that Vietnam has a lopsided imbalance with the U.S. and should monitor its bilateral trade balances carefully, reducing its surplus by buying more U.S. imports. More importantly, the TR is absolutely correct in having pointed out that Vietnam should focus on raising the productivity of the domestic economy by undertaking public enterprise reforms and providing the same level playing field to domestic private enterprises as to foreign-owned enterprises. But to classify Vietnam as a currency manipulator is neither correct nor helpful in policy dialogue with the country. Exchange rate adjustments would do nothing to these needed reforms at this stage, and may worsen the current distortions by creating more uncertainty and thereby penalizing domestic private enterprises. As the US-Vietnam trade imbalance may continue to grow in 2021 and beyond, it seems clear that the Biden Administration will have no alternative except to deal with the issue. As such, the current discussion between the two countries will continue and arguments in this article could provide inputs to the forthcoming dialogue.

References

IMF (2020). External Sector Report: Global Imbalances and the COVID-19 Crisis. Washington, DC, August. https://www.imf.org/en/Publications/ESR/Issues/2020/07/28/2020-external-sector-report.

IMF (2019). Vietnam : 2019 Article IV Consultation; Press Release; Staff Report; and Statement by the Executive Director for Vietnam. July. https://www.imf.org/en/Publications/CR/Issues/2019/07/16/Vietnam-2019-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-47124

IMF (2018). Vietnam : 2018 Article IV Consultation; Press Release; Staff Report; and Statement by the Executive Director for Vietnam. July. https://www.imf.org/en/Publications/CR/Issues/2018/07/10/Vietnam-2018-Article-IV-Consultation-Press-Release-and-Staff-Report-46064

Phillips, M. S., Catão, M. L., Ricci, M. L. A., Bems, M. R., Das, M. M., Di Giovanni, M. J., ... & Vargas, M. M. (2013). The external balance assessment (EBA) methodology. International Monetary Fund. https://www.imf.org/en/Publications/WP/Issues/2016/12/31/The-External-Balance-Assessment-EBA-Methodology-41200

Treasury, U. S. (2020). Macroeconomic and foreign exchange policies of major trading partners of the United States. December. https://home.treasury.gov/system/files/206/December-2020-FX-Report-FINAL.pdf

[1] We must point out here that as an econometric model, the EBA encounters other problems. The EBA model involves 20 variables, many of which are estimates. A number of variables are even non-financial, such as the “dependency ratio,” “the aging speed,” and the “safer institutional/political environment index.” One variable, the “own currency share in world reserves” is irrelevant to Vietnam since the dong is not a part of world reserves.