Publications /

Policy Brief

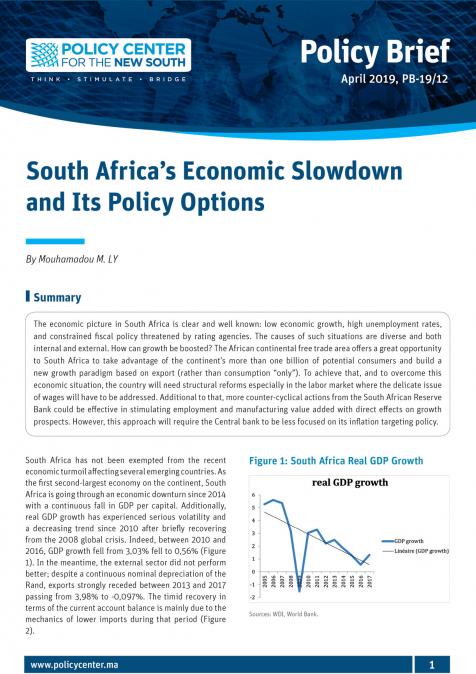

The economic picture in South Africa is clear and well known: low economic growth, high unemployment rates, and constrained fiscal policy threatened by rating agencies. The causes of such situations are diverse and both internal and external. How can growth be boosted? The African continental free trade area offers a great opportunity to South Africa to take advantage of the continent’s more than one billion of potential consumers and build a new growth paradigm based on export (rather than consumption “only”). To achieve that, and to overcome this economic situation, the country will need structural reforms especially in the labor market where the delicate issue of wages will have to be addressed. Additional to that, more counter-cyclical actions from the South African Reserve Bank could be effective in stimulating employment and manufacturing value added with direct effects on growth prospects. However, this approach will require the Central bank to be less focused on its inflation targeting policy.